Best Mortgage Lenders in Kentucky with Joel Lobb

Are you a prospective homebuyer in Kentucky searching for the best mortgage lenders? Joel Lobb is a trusted mortgage broker. He has a proven track record of helping clients secure competitive mortgage rates. He also helps clients with financing options. With Joel Lobb by your side, you can access top-notch mortgage lenders in Kentucky. He will help you make your dream of homeownership a reality.

Joel Lobb has established strong relationships with a network of reputable mortgage lenders in Kentucky. These lenders offer a wide range of loan programs. These programs can suit your unique needs and financial goals. Whether you’re a first-time homebuyer, a seasoned investor, or looking to refinance your existing mortgage, Joel Lobb can connect you with the best mortgage lenders that offer:

- Competitive Interest Rates: Access mortgage loans with competitive interest rates. These rates can save you money over the life of your loan.

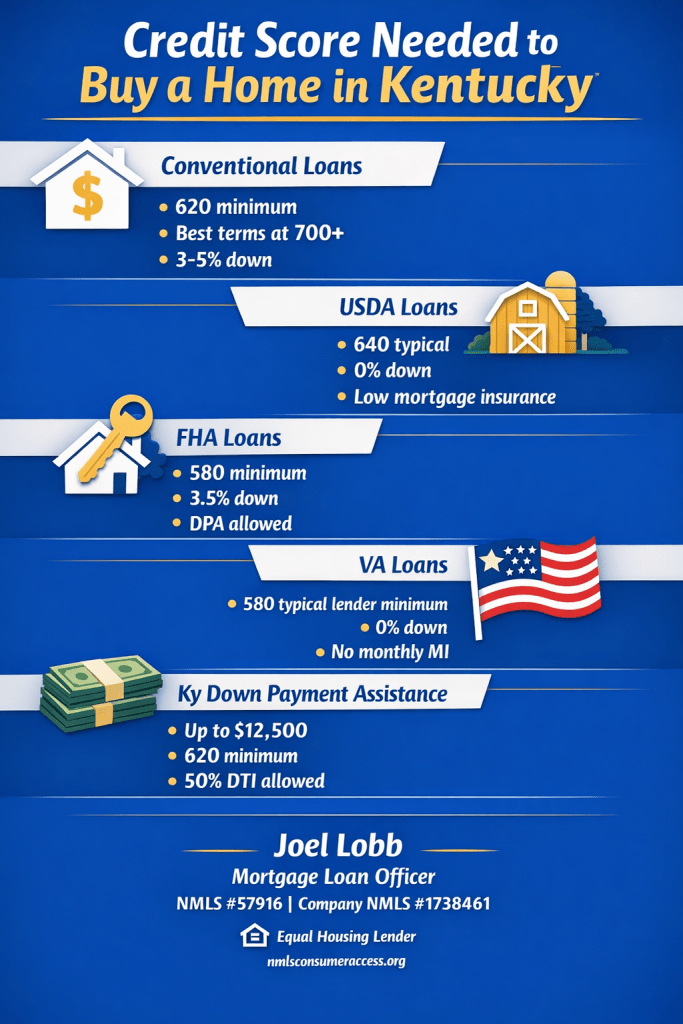

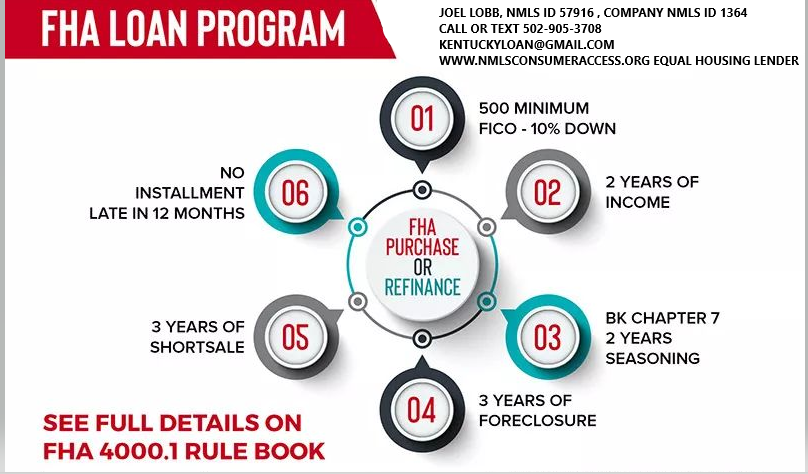

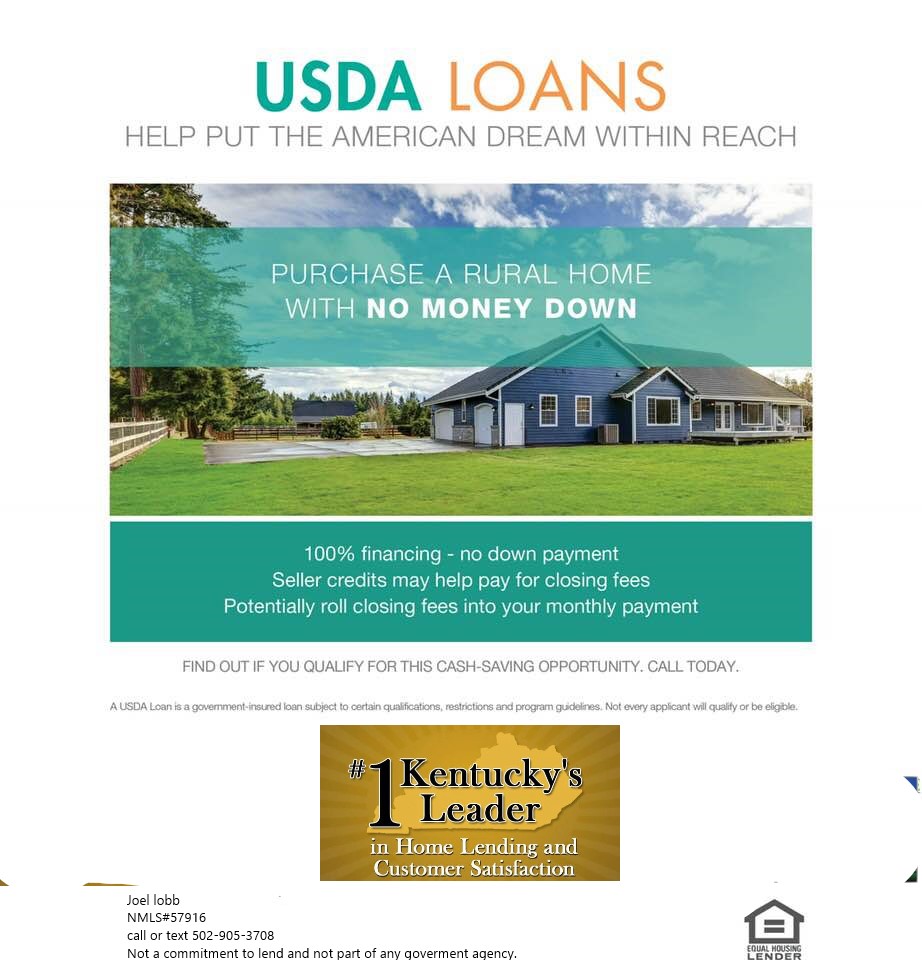

- Flexible Loan Programs: Choose from a variety of loan programs. These include FHA, VA, USDA, conventional, jumbo loans, and more. They are tailored to your specific requirements.

- Personalized Guidance: Receive personalized guidance and support throughout the mortgage process. This includes steps from pre-qualification to closing. These efforts ensure a smooth and stress-free experience.

- Quick and Efficient Approval: Benefit from efficient loan processing. Experience quick approval times, allowing you to close on your new home faster.

- Transparent and Honest Service: Experience transparent and honest communication throughout your mortgage journey. We provide full transparency on loan terms, fees, and requirements.

When you are looking for the best mortgage lenders in Kentucky, Joel Lobb stands out. He is a trusted advisor and advocate for his clients’ best interests. With Joel Lobb’s expertise and industry knowledge, you can navigate the complex world of mortgage lending with confidence. You can achieve your homeownership goals.

Contact Joel Lobb today. Learn more about the best mortgage lenders in Kentucky. Start your journey towards owning the perfect home for you and your family.

Joel Lobb Mortgage Loan Officer

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

Call/Text: 502-905-3708 Call/Text: 502-905-3708 Email: kentuckyloan@gmail.com Email: kentuckyloan@gmail.com Website: www.mylouisvillekentuckymortgage.com Website: www.mylouisvillekentuckymortgage.com  Address: 911 Barret Ave, Louisville, KY 40204 Address: 911 Barret Ave, Louisville, KY 40204NMLS #57916 | Company NMLS #1738461 |

Click here to apply for Free Info & Homebuyer Advice → Click here to apply for Free Info & Homebuyer Advice → |

|

Kentucky Mortgage Loan Expert

FHA | VA | USDA | KHC Down Payment Assistance | Fannie Mae

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval and program requirements.

|

Email –

Email – Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome