Kentucky FHA Loan Requirements 2026: Credit, Down Payment, Limits & Approval Guide

Everything Kentucky first-time homebuyers need to know — credit scores, down payment, debt-to-income, mortgage insurance, property rules, waiting periods, and the deal-killers many lenders do not explain upfront.

Get pre-approved in as little as 24 hours — even if your credit is not perfect.

On This Page

What Is an FHA Loan and Why Does It Matter in Kentucky?

An FHA loan is a mortgage insured by the Federal Housing Administration under HUD. The FHA does not lend money directly. Instead, it insures approved lenders against loss, which allows those lenders to offer more flexible approval guidelines than many conventional programs.

For Kentucky homebuyers, especially first-time buyers, FHA financing can be a practical path to homeownership because it may allow:

- Lower minimum credit scores than many conventional loans

- Down payment as low as 3.5%

- Gift funds for down payment and closing costs

- Higher debt-to-income ratios in many cases

- A way to buy after bankruptcy or foreclosure once waiting periods are met

1. Income & Employment Requirements

Two-Year Work History Is the Baseline

FHA generally looks for a two-year employment history. That does not always mean two years with the same employer. The bigger issue is consistency in the same line of work and the ability to document stable income.

- Two years of employment history is preferred

- Job changes are usually fine if they are in the same field or a logical advancement

- Recent graduates may be able to use education history to support the file

- Self-employed borrowers generally need two years of tax returns

- Part-time, overtime, bonus, and commission income usually need a history before counting

Kentucky tip: A job change for more pay in the same field is usually not the problem. Unexplained gaps, inconsistent hours, and unstable earnings are what create underwriting friction.

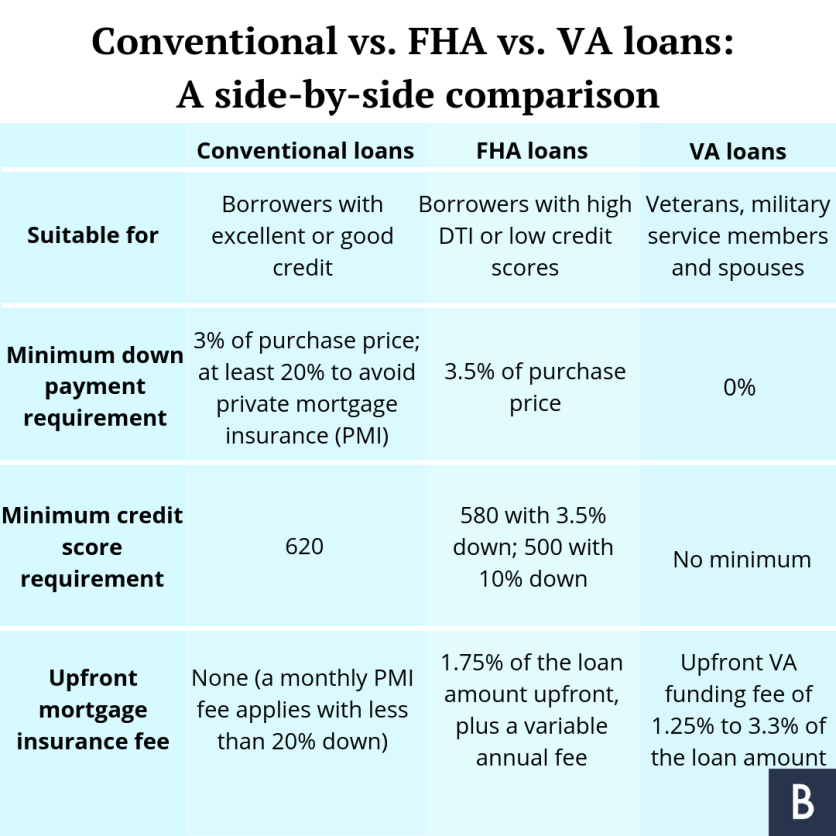

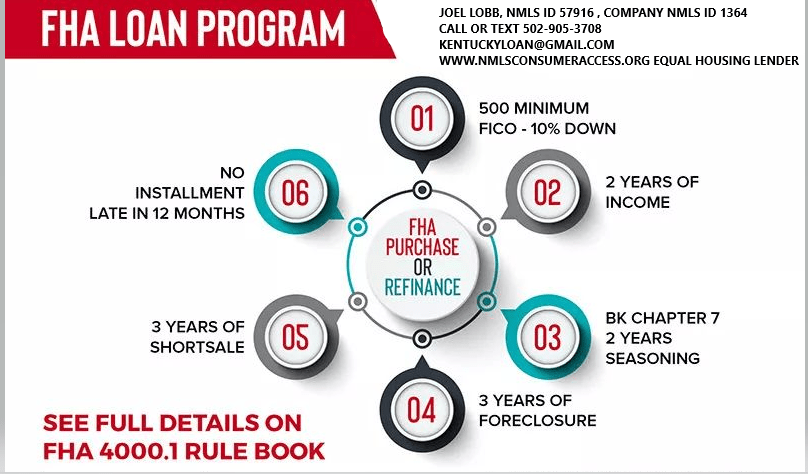

2. Credit Score & Down Payment

FHA Credit Score Tiers

| Credit Score Range | Minimum Down Payment | Real-World Status |

|---|---|---|

| 620 and above | 3.5% | Most lender-friendly |

| 580 to 619 | 3.5% | Usually workable |

| 500 to 579 | 10% | Limited lender options |

| Below 500 | Not eligible | Not FHA eligible |

Lender overlays matter. FHA may allow lower scores, but many lenders set stricter internal minimums. That is why borrowers often hear one thing online and something very different when they actually apply.

3. Debt-to-Income Limits

Front-End and Back-End DTI

Debt-to-income ratio measures how much of your gross monthly income goes toward monthly debt obligations. FHA reviews both housing-only and total debt ratios.

| DTI Type | What It Includes | Common Target |

|---|---|---|

| Front-End | Mortgage payment, taxes, insurance, and FHA mortgage insurance | About 31% |

| Back-End | Housing payment plus all monthly debts on credit | About 43% |

AUS flexibility: With a strong automated approval, debt ratios can often go above 43%. With manual underwriting, the file usually gets much tighter and compensating factors matter a lot more.

4. Acceptable Down Payment Sources

Funds Must Be Verified and Sourced

FHA is flexible about where funds come from, but not loose about documentation. Every dollar used for down payment and closing costs needs a clean paper trail.

Acceptable Sources

- Personal checking or savings

- Verified gift funds from family or eligible donors

- Retirement account withdrawals or loans when documented

- Sale of personal property with documentation

- Approved down payment assistance programs

Common Problems

- Cash deposits with no paper trail

- Borrowed funds from unapproved sources

- Undocumented transfers between accounts

- Large deposits that cannot be explained

- Gift funds without a gift letter and evidence of transfer

Bottom line: The money itself is often not the issue. Documentation is the issue. If the money cannot be sourced, it can derail the approval even when the borrower otherwise qualifies.

5. Property Requirements

The Home Has to Meet FHA Standards

FHA is not just approving the borrower. It is also approving the collateral. The property must be safe, sound, and marketable.

- The property must be owner-occupied as a primary residence

- The appraisal must support value and FHA minimum property standards

- Health and safety issues may need to be repaired before closing

- Utilities generally need to be on for proper appraisal review

- Manufactured homes have additional foundation and eligibility requirements

Important: FHA financing can be used on single-family homes, many condos, certain multi-unit owner-occupied properties, and some manufactured homes, but every category has its own eligibility rules.

6. Bankruptcy & Foreclosure Waiting Periods

Waiting Periods Do Exist, but FHA Is More Forgiving Than Many Programs

| Credit Event | Typical FHA Waiting Period | Notes |

|---|---|---|

| Chapter 7 Bankruptcy | 2 years | From discharge date in most cases |

| Chapter 13 Bankruptcy | 12 months | On-time trustee payments and court approval usually required |

| Foreclosure | 3 years | From completion date in most cases |

| Short Sale | Varies | May be sooner depending on how it reported and current credit profile |

7. Federal Debt & the CAIVRS Check

CAIVRS Is the Federal Database Many Buyers Never Hear About

Before FHA approval, borrowers are checked through CAIVRS, the federal database that flags certain unresolved government-related defaults or claims.

- Defaulted federally backed student loans

- Prior FHA or other government-backed loan claims

- Certain unresolved federal delinquencies or judgments

A CAIVRS hit can stop the deal cold. This is not something you finesse around. The underlying issue usually has to be resolved before the FHA loan can move forward.

8. FHA Mortgage Insurance Premium

Mortgage insurance is part of the FHA tradeoff. It is one reason FHA works for lower down payment and more flexible credit, but it also increases the payment.

On a $200,000 FHA loan, the upfront mortgage insurance premium adds about $3,500 to the loan amount if financed. Monthly mortgage insurance varies, but it can make a meaningful difference in payment planning.

Long-term strategy: Many FHA borrowers later refinance into a conventional loan once they build equity and improve credit, because FHA mortgage insurance does not work like conventional PMI in many cases.

The Top FHA Deal-Killers in Kentucky

After working through hundreds of FHA files, these are the issues that most often kill deals, delay closings, or force borrowers to regroup.

Credit overlays

The FHA guideline may say one thing, but the actual lender may require a higher score or cleaner profile.

Unsourced funds

Cash deposits, undocumented transfers, or gift money with no paper trail can stop the loan.

Appraisal issues

Safety, condition, value, or eligibility problems can delay or kill the transaction.

Federal debt problems

Defaulted student loans or other federal issues can cause a CAIVRS denial.

High debt ratios

If the automated system does not approve it, manual underwriting can get strict quickly.

Inconsistent income

Variable hours, weak earnings history, or recent instability can reduce qualifying income.

The Smart Long-Term FHA Strategy

FHA is often the best entry point, not always the best forever loan. For many Kentucky buyers, the real win is using FHA to get in the home now, then improving the credit profile and refinancing later when the numbers make sense.

Get pre-approved

Run the numbers honestly and determine what is actually workable today.

Use the right assistance

Layer in any available gift funds or down payment assistance that fits the file.

Buy with a plan

Get into the home, stabilize finances, build equity, and improve the credit profile.

Refinance later

Review conventional refinance options when rates, equity, and scores line up.

Frequently Asked Questions — Kentucky FHA Loans

Can I get an FHA loan with a 580 credit score in Kentucky?

Yes. FHA guidelines allow 580 with 3.5% down, but many lenders have overlays. Real-world approval depends on the full file, not just the score.

Is there down payment assistance available for Kentucky FHA loans?

Yes. Some Kentucky borrowers may qualify for Kentucky Housing Corporation down payment assistance, depending on income, credit, and program limits.

How long does FHA approval take in Kentucky?

A pre-approval can often be issued quickly with full documentation. From contract to closing, many FHA purchases land in the 30 to 45 day range, though every file is different.

Can I use an FHA loan to buy a duplex in Kentucky?

Yes, if you live in one unit as your primary residence and the property meets FHA rules. FHA is not for a pure non-owner-occupied investment purchase.

Does FHA mortgage insurance ever go away?

That depends on the loan structure, but many FHA borrowers eventually refinance into conventional financing once they have enough equity and improved credit.

What is the FHA loan limit for Kentucky in 2026?

Loan limits depend on property type and county rules in effect for the year. Always verify current limits for the specific property and loan structure before proceeding.

Ready to Apply for an FHA Loan in Kentucky?

Start your free mortgage review with Joel Lobb. Get straight answers on credit, income, down payment, and what you may qualify for now — without wasting time on the wrong program.

NMLS #57916 | Company NMLS #1738461 | Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval and program requirements. This website is not affiliated with or endorsed by FHA, VA, USDA, KHC, or any government agency. Licensed in Kentucky only. NMLS Consumer Access

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Email –

Email – Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome