Mobile Home Loans in Kentucky: FHA, VA, USDA, and Conventional Guidelines for 2026

Are you a Kentucky homebuyers looking for information on mobile home loans? Manufactured homes are an affordable option for many buyers. With flexible financing options like Kentucky FHA, VA, USDA, and Conventional loans, achieving homeownership in Kentucky is easier than ever. This guide provides the guidelines for each loan program. It also explains how you can qualify for a free mortgage loan approval for your mobile home in Kentucky.

Mobile Home Loan Options in Kentucky

Manufactured homes offer affordable housing solutions, but the financing process requires specific guidelines. Here’s a breakdown of the major loan programs for mobile home loans in Kentucky, their qualifications, and how they work.

FHA Mobile Home Loans in Kentucky

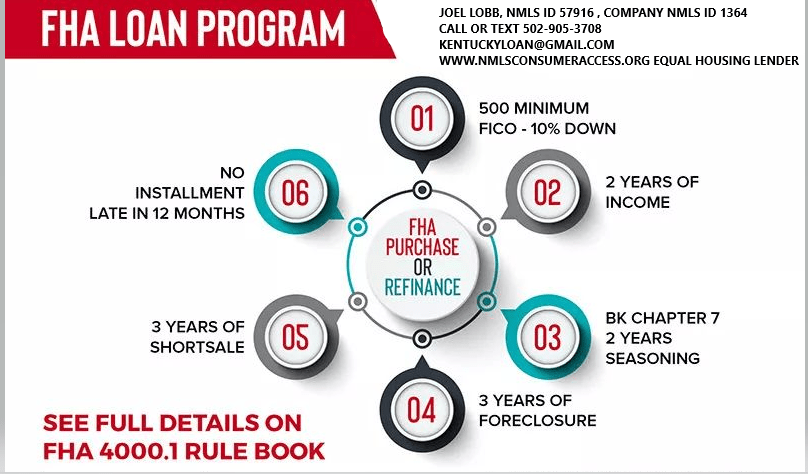

The FHA Loan Program is one of the most popular options for manufactured homes in Kentucky. This program requires a low credit score and offers competitive terms. It is ideal for first-time buyers or those with less-than-perfect credit.

- Minimum Credit Score: 500 qualifying FICO score.

- Property Types: Singlewide, Doublewide, and Triplewide manufactured homes.

- Loan-to-Value (LTV): Up to 96.5% LTV for purchase and 80% for cash-out refinancing.

- Underwriting: Manual underwrites are allowed.

- Key Guidelines:

- Homes must have been constructed after June 15, 1976.

- The home cannot have been previously installed or occupied at another site.

- Real property conversion is required at closing.

- Primary residence only.

- Advantages: No pricing adjuster for manufactured homes.

VA Mobile Home Loans in Kentucky

If you are a veteran or active-duty service member, consider the VA Loan Program. It is an excellent option for financing a mobile home. This program offers 100% financing with no down payment required.

- Minimum Credit Score: 500 qualifying FICO score.

- Property Types: Singlewide, Doublewide, and Triplewide units.

- Loan-to-Value (LTV): Up to 100% for purchases and 90% for cash-out refinancing.

- Underwriting: Manual underwrites are allowed.

- Key Guidelines:

- Homes must have been constructed after June 15, 1976.

- The home cannot have been previously installed or occupied at another site.

- Real property conversion is required at closing.

- Primary residence only.

USDA Mobile Home Loans in Kentucky

The USDA Loan Program provides 100% financing for manufactured homes in eligible rural areas of Kentucky. This loan is ideal for homebuyers looking for affordable financing with no down payment.

- Minimum Credit Score: 581 qualifying FICO score.

- Property Types: Singlewide, Doublewide, and Triplewide units.

- Loan-to-Value (LTV): Up to 100% for purchases.

- Home Requirements:

- Must be a 2006 model or newer.

- Located in a USDA-eligible rural area.

- Underwriting: Manual underwriting is required (Max DTI: 29/41).

- Key Guidelines:

- The home cannot have been previously installed or occupied at another site.

- Real property conversion is required at closing.

- Primary residence only.

- Eligible States: RD Program available in KY and select other states.

Conventional Mobile Home Loans in Kentucky

The Conventional Loan Program is another option for financing manufactured homes in Kentucky. It offers competitive terms for buyers with stronger credit profiles.

- Minimum Credit Score: 620 qualifying FICO score.

- Property Types: Singlewide, Doublewide, and Triplewide units.

- Loan-to-Value (LTV): Up to 95% for purchases and 65% for cash-out refinancing.

- Cash-out refinancing is not allowed on singlewide homes.

- Key Guidelines:

- Homes must have been constructed after June 15, 1976.

- The home cannot have been previously installed or occupied at another site.

- Real property conversion is required at closing.

- Both primary residences and second homes are allowed.

- Small pricing adjuster applies for manufactured homes.

Mobile Home Loans in Kentucky: FHA, VA, USDA, and Conventional Guidelines

If you’re a Kentucky homebuyer looking to finance a mobile home, understanding the different loan options and guidelines is essential. Below, we break down the requirements for FHA loans. We also cover the requirements for VA, USDA, and Conventional loans. This information will help you secure a mobile home loan in Kentucky. Learn how you can qualify for a free mortgage loan pre-approval today!

| Loan Program | Credit Score Requirement | Eligible Property Types | Loan-to-Value (LTV) | Key Guidelines | Additional Notes |

|---|---|---|---|---|---|

| FHA Loan | 500 minimum FICO score | Singlewide, Doublewide, Triplewide homes | Purchase/Rate-Term up to 96.5% LTV Cash-Out up to 80% LTV | – Manual underwriting allowed – Real Property Conversion allowed at closing – Primary residence only – Exempt from ATR Points/Fees Test | – No prior installation/occupancy at another site – No pricing adjuster for mobile homes – Home must be constructed after June 15, 1976 |

| VA Loan | 500 minimum FICO score | Singlewide, Doublewide, Triplewide homes | Purchase/Rate-Term up to 100% LTV Cash-Out up to 90% LTV | – Manual underwriting allowed – Real Property Conversion allowed at closing – Primary residence only – Exempt from ATR Points/Fees Test | – No prior installation/occupancy at another site – No pricing adjuster for mobile homes – Home must be constructed after June 15, 1976 |

| USDA Loan | 581 minimum FICO score | Singlewide, Doublewide, Triplewide homes | Purchase up to 100% LTV | – Manual underwriting required (Max DTI: 29/41) – Home must be a 2006 model or newer – Located in USDA-eligible rural areas – Primary residence only | – No prior installation/occupancy at another site – No pricing adjuster for mobile homes – RD Program available in specific states, including Kentucky |

| Conventional Loan | 620 minimum FICO score | Singlewide, Doublewide, Triplewide homes | Purchase/Rate-Term up to 95% LTV Cash-Out up to 65% LTV | – Real Property Conversion allowed at closing – Primary and second homes allowed – Cash-Out not allowed on Singlewide homes | – No prior installation/occupancy at another site – Small 50 pricing adjuster for mobile homes – Home must be constructed after June 15, 1976 |

Why Choose a Mobile Home Loan in Kentucky?

Mobile homes, also known as manufactured homes, offer an affordable housing solution for Kentucky residents. Whether you’re a first-time homebuyer or looking to refinance your property, government-backed loans can help. Conventional options also provide flexible terms. These options make homeownership a reality.

How to Qualify for a Mobile Home Loan in Kentucky

- Step 1: Check your credit score against the loan program requirements. The minimum FICO score is 500 for FHA and VA loans. For USDA loans, it is 550. Conventional loans require a score of 620.

- Step 2: Ensure the mobile home meets eligibility guidelines (e.g., it must be a 2006 model or newer for USDA loans or constructed after June 15, 1976, for FHA, VA, and Conventional loans).

- Step 3: Verify the home is not previously installed or occupied at another site.

- Step 4: Contact a trusted Kentucky mortgage lender to get a free pre-approval for your mobile home loan.

Free Pre-Approval for Mobile Home Loans in Kentucky

Ready to take the next step? As a Kentucky homebuyer, you can benefit from free mortgage loan pre-approval for your mobile home loan. You might be interested in an FHA, VA, USDA, or Conventional loan. Our experts will guide you through the process. They will find the best option for your needs.

Why Choose a Mobile Home Loan in Kentucky?

Manufactured homes in Kentucky offer affordability, flexibility, and modern designs. Whether you’re a first-time homebuyer or someone looking to refinance your current mobile home, these loan programs provide tailored solutions. They meet your needs. With low credit score requirements and flexible terms, financing your manufactured home is within reach.

Get Pre-Approved for a Mobile Home Loan in Kentucky Today!

Ready to take the next step? Get a free mortgage pre-approval for your mobile home loan in Kentucky today. We offer expert guidance on FHA, VA, USDA, and Conventional loan programs. We’ll help you find the best financing option for your needs.

Contact us now to get started on your journey to owning a manufactured home in Kentucky. Call or apply online for your free pre-qualification and same-day approval!

Email – kentuckyloan@gmail.com

Call/Text – 502-905-3708

Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com

Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Email –

Email – Call/Text –

Call/Text –  Website:

Website:  Address:

Address:  First-Time Home Buyers Welcome

First-Time Home Buyers Welcome

Email:

Email:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204