<!– WordPress.com-friendly page content (no , no , no ) –>

Kentucky FHA Loans (2026): Requirements, Down Payment, Credit Scores, and How to Get Approved

If you are buying a home in Kentucky and want a low down payment option with more flexible credit guidelines, an FHA loan is often the most practical path. This guide covers the FHA rules that matter in 2026, the common underwriting issues that slow people down, and the fastest way to get a clean pre-approval.

Want a same-day pre-approval review? Call or text 502-905-3708 or email kentuckyloan@gmail.com.

Helpful links (official + Kentucky-specific):

• FHA loan limits lookup (by Kentucky county):

HUD FHA Mortgage Limits

• FHA underwriting rules source document:

HUD Handbook 4000.1

• Kentucky Housing down payment assistance overview:

KHC Down Payment Assistance

Quick FHA Requirements Snapshot (Kentucky)

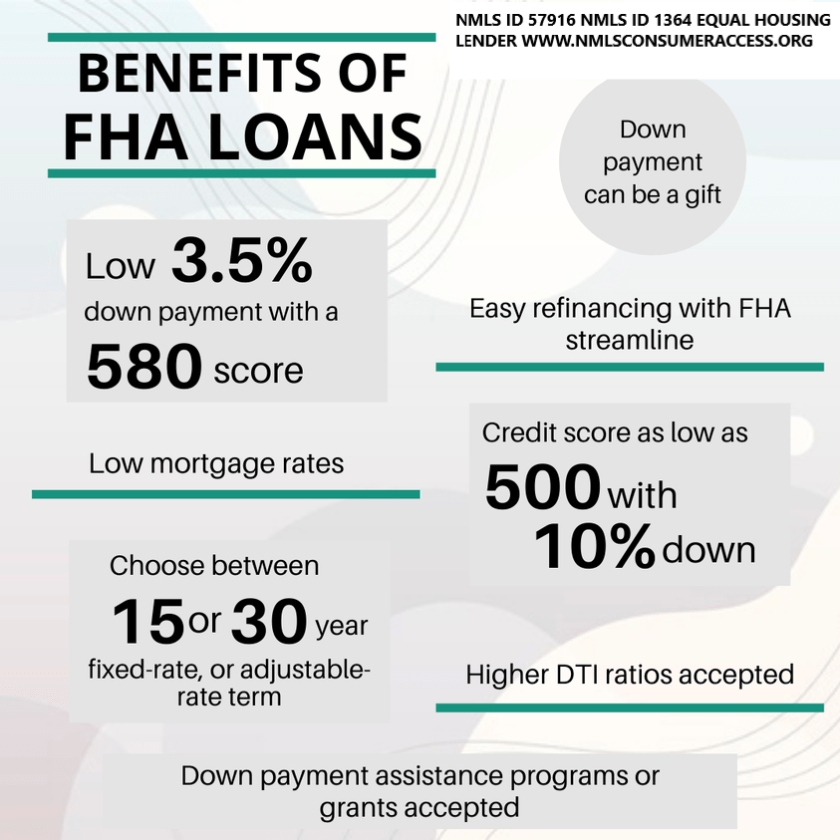

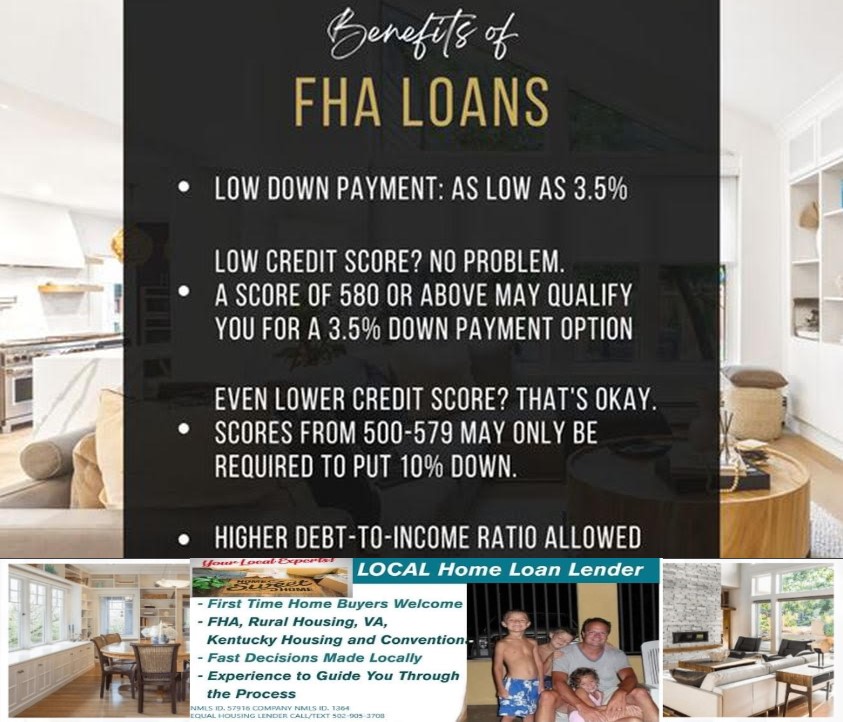

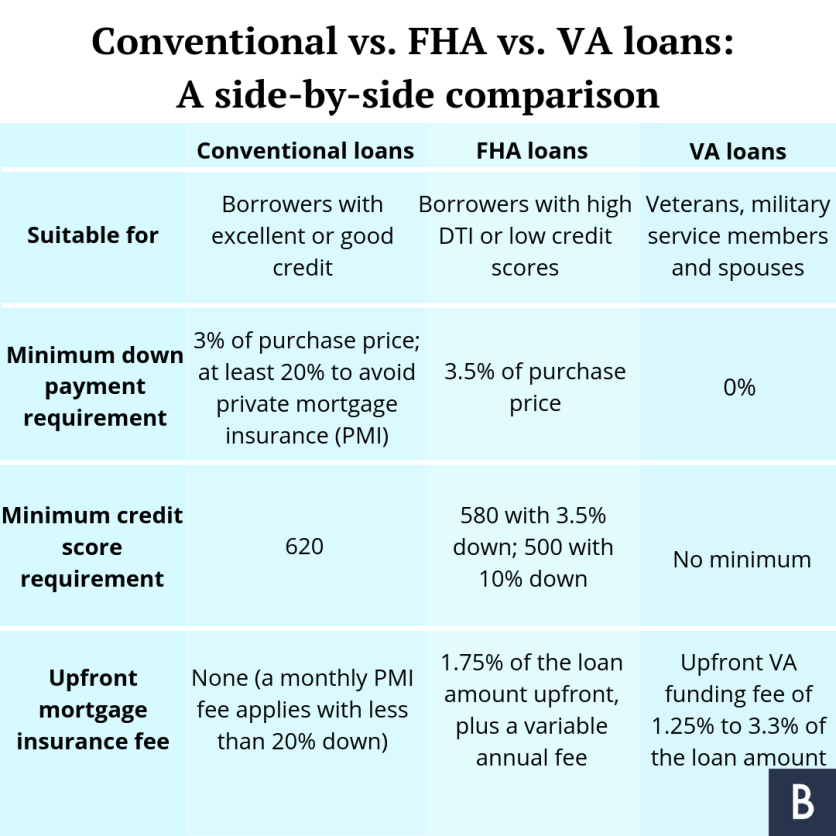

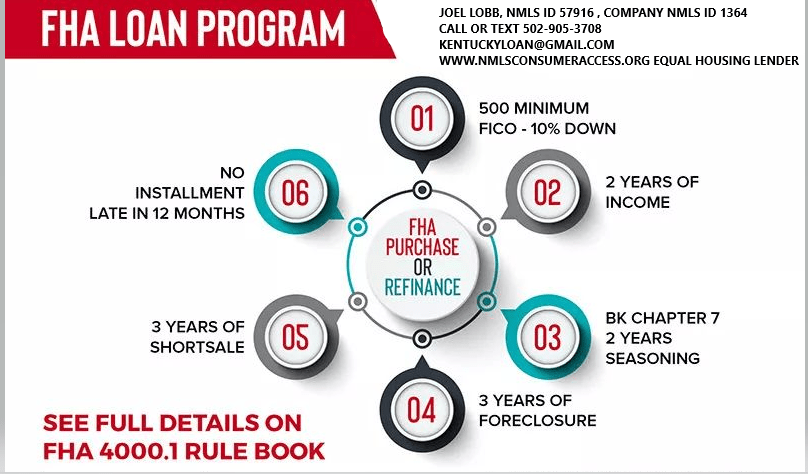

- Minimum down payment: 3.5% with 580+ credit score; 10% with 500–579 (case-by-case).

- Primary residence only (no investment property).

- FHA appraisal required and the home must meet FHA property standards.

- Seller concessions allowed up to 6% of the sales price toward certain closing costs and fees.

- Mortgage insurance is required (upfront + monthly/annual).

Want me to price your payment and cash-to-close fast? Text “FHA” to 502-905-3708 and I will reply with a document checklist.

Credit Score Guidelines for Kentucky FHA Loans

FHA guidelines allow:

- 580+ credit score: eligible for the 3.5% minimum down payment option.

- 500–579 credit score: may be eligible with 10% down (approval depends on the full file).

- Below 500: generally not eligible for FHA financing.

Important: lenders can add “overlays” (stricter requirements than FHA). That is why two lenders can give two different answers on the same borrower. If you want a straight answer, I will review your scenario and tell you what is realistically approvable.

Next step: Call or text 502-905-3708 for a quick credit-and-income review.

Down Payment and Closing Costs (What Kentucky Buyers Actually Pay)

FHA requires a minimum down payment based on credit score. Closing costs are separate and typically include lender fees, title, escrow, and prepaid items like taxes and homeowners insurance.

3 ways Kentucky FHA buyers reduce cash-to-close

- Seller concessions (up to 6% of the sales price, when allowed and properly structured).

- KHC Down Payment Assistance (for eligible borrowers using a KHC first mortgage).

- Lender credits (higher rate trade-off to reduce upfront costs, when it makes sense).

External reference on seller concessions: HUD guidance on interested party contributions

Kentucky FHA Loan Limits (2026)

FHA loan limits change by county and are updated periodically. The cleanest way to avoid outdated numbers is to pull your county limit directly from HUD.

Use this official lookup tool: HUD FHA Mortgage Limits by County

If you text me your county (or the property address), I will confirm the current FHA limit and your max purchase price: 502-905-3708.

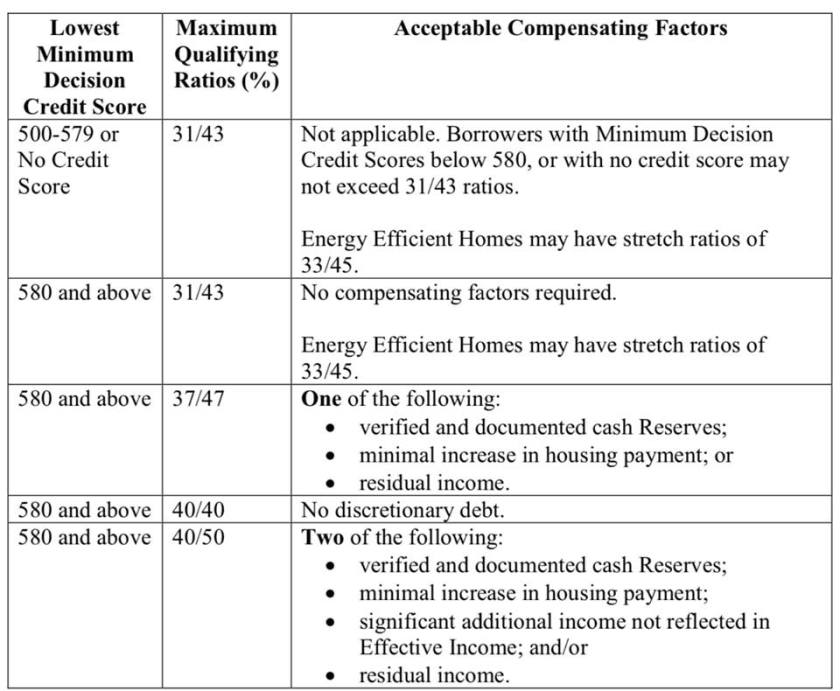

Debt-to-Income Ratio (DTI): What FHA Looks At

FHA underwriting looks at housing expense compared to income and total monthly debts compared to income. A common baseline guideline you will see referenced is 31% for housing and 43% for total debt, with exceptions possible depending on automated underwriting results and compensating factors.

- Housing ratio (front-end): proposed house payment compared to gross monthly income.

- Total DTI (back-end): house payment plus monthly debts compared to gross monthly income.

If your DTI is tight, the fix is usually one of these: adjust purchase price, restructure debt, improve credit, or document additional qualifying income correctly.

Types of FHA Loans Kentucky Buyers Use Most

FHA 203(b) Standard Purchase

The most common FHA loan for buying a primary residence in Kentucky.

FHA 203(k) Renovation Loan

Combines purchase plus renovation costs into one loan for qualifying homes that need repairs or updates.

FHA Streamline Refinance

For existing FHA borrowers looking to reduce payment with simplified documentation (when eligible).

FHA Cash-Out Refinance

For homeowners who want to access equity (subject to FHA rules and underwriting).

Internal links (recommended):

• VA Loans: Kentucky VA Home Loans

• USDA Loans: Kentucky USDA Zero Down Loans

• KHC Programs: Kentucky Housing (KHC) Loan Programs

KHC Down Payment Assistance (Pairs Well with FHA)

Kentucky Housing Corporation (KHC) offers down payment assistance for eligible borrowers using a KHC first mortgage. KHC’s Regular DAP has been listed as assistance up to $12,500, repayable over 15 years at 4.75% (subject to program terms, eligibility, and availability). Confirm current options here: KHC Down Payment Assistance.

If you want a straight answer on eligibility (income limits, purchase price limits, and which first mortgage fits), call or text me: 502-905-3708.

How to Apply for an FHA Loan in Kentucky (Simple Process)

- Quick consult (10 minutes): goals, county, price range, and down payment plan.

- Document review: paystubs, W-2s, bank statements, and ID.

- Run automated underwriting and issue a clean pre-approval.

- Home shopping + contract.

- Appraisal, underwriting, and final approval.

- Closing and keys.

Primary CTA:

Call or Text 502-905-3708 for FHA Pre-Approval

Email: kentuckyloan@gmail.com

Secondary CTA (site):

Start here: mylouisvillekentuckymortgage.com

FHA FAQ (Kentucky)

Do FHA loans have income limits?

FHA itself does not set income limits. However, down payment assistance programs (like KHC) typically do.

How long does an FHA loan take to close?

Many FHA purchases close in the 30–45 day range, depending on appraisal timing, documentation, and underwriting conditions.

Can the seller pay my closing costs on FHA?

Seller concessions are allowed up to 6% of the sales price toward certain costs when structured correctly. Reference: HUD guidance.

Where can I verify FHA loan limits for my Kentucky county?

Use HUD’s official lookup tool: FHA Mortgage Limits.

About

Joel Lobb — Kentucky Mortgage Loan Officer

NMLS Personal ID: 57916 | Company NMLS: 1738461

Call/Text: 502-905-3708 |

Email: kentuckyloan@gmail.com

NMLS Consumer Access: nmlsconsumeraccess.org

Email –

Email – Call/Text –

Call/Text –  Website:

Website:  Address:

Address:  First-Time Home Buyers Welcome

First-Time Home Buyers Welcome

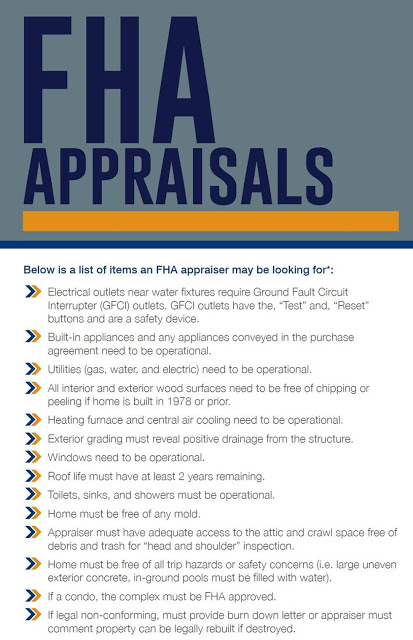

Debt-to-Income Ratio Requirements –Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

Debt-to-Income Ratio Requirements –Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family. Property Requirements for a Kentucky FHA LoanIt must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.It is really not too hard to pass FHA loans and the appraisal process.

Property Requirements for a Kentucky FHA LoanIt must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.It is really not too hard to pass FHA loans and the appraisal process. Pros of FHA Loans –

Pros of FHA Loans –