FHA vs. Conventional Loans: Which Is Better for Kentucky Homebuyers?

Compare FHA and conventional loans for Kentucky homebuyers. Learn credit requirements, down payments, mortgage insurance, and which loan fits your situation.

When comparing FHA loans vs conventional loans in Kentucky, the decision comes down to four core factors: credit score, down payment, debt-to-income ratio, and mortgage insurance. Both loan programs are widely used across Louisville, Lexington, Northern Kentucky, and rural areas, but they serve very different borrower profiles.

FHA Loans: Built for Flexibility

Kentucky FHA loans are designed for buyers who need more flexibility. FHA financing is often a strong option for borrowers with credit scores under 680, limited savings, or little to no cash reserves after closing. FHA also allows buyers to qualify sooner after major credit events, including foreclosures that are three to seven years old and short sales that occurred two to four years ago.

Another major advantage of FHA loans in Kentucky is gifting. The entire down payment and most closing costs can be covered with gift funds from approved sources. This makes FHA especially popular with first-time homebuyers and buyers using down payment assistance programs.

FHA Mortgage Insurance (MIP) Breakdown:

- Upfront mortgage insurance premium: 1.75% of loan amount (rolled into the loan)

- 30-year loans with less than 5% down: 0.85% annually

- 30-year loans with 5%+ down: 0.80% annually

- 15-year loans: 0.45% to 0.70% annually (depending on down payment)

Conventional Loans: For Stronger Credit

Kentucky conventional loans are best suited for borrowers with stronger credit and more money saved. Conventional financing generally favors buyers with credit scores above 680, at least five percent down, and reserves remaining after closing. Borrowers with foreclosures over seven years old or short sales that occurred five to seven years ago typically fit conventional guidelines more easily.

One of the biggest advantages of conventional loans is mortgage insurance flexibility. Unlike FHA, there is no upfront mortgage insurance premium. Monthly private mortgage insurance can be lower for borrowers with strong credit, and PMI automatically drops off once the loan reaches roughly 80 percent loan-to-value. FHA mortgage insurance, by contrast, usually lasts for the life of the loan when the down payment is less than ten percent.

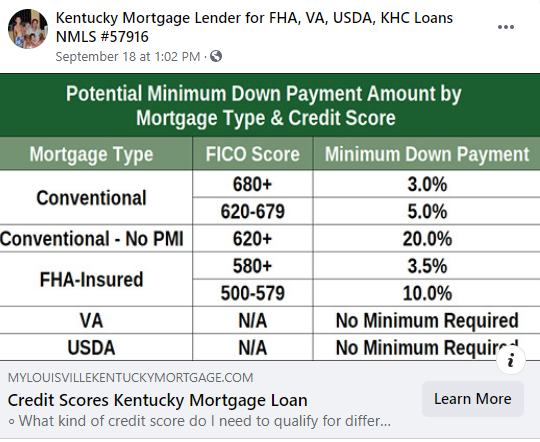

Quick Comparison Table

| Factor | FHA Loans | Conventional Loans |

|---|---|---|

| Credit Score Required | 580+ 3.5% down payment (some lenders 500+ 10% down payment) | 720+ typically |

| Down Payment | 3.5% (with 580+ score) | 3-5% minimum, typically 5% |

| Mortgage Insurance | Required on all loans (lifetime with <10% down) | Only if less than 20% down; drops at 80% LTV |

| Upfront Insurance Premium | 1.75% | None |

| Gift Funds | 100% of down payment allowed | Limited or restricted |

| Max Debt-to-Income | Up to 56.99% (with compensating factors) | Typically 45% |

| Property Types | Owner-occupied only | Owner-occupied and investment |

| Appraisal Standards | Stricter | More flexible |

The Bottom Line

FHA loans are ideal for Kentucky buyers rebuilding credit, using gift funds, or purchasing with limited savings. Conventional loans reward borrowers with stronger credit, larger down payments, and long-term equity goals.

Most homeowners do not keep a mortgage for 30 years. Because many refinance or sell within five to seven years, FHA’s lifetime mortgage insurance is often less of a concern than it appears on paper. In many cases, the lower interest rate and easier approval standards outweigh the insurance cost.

|

Joel Lobb

Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae

EVO Mortgage • Helping Kentucky Homebuyers Since 2001

|

Call/Text: 502-905-3708 Call/Text: 502-905-3708 Email: kentuckyloan@gmail.com Email: kentuckyloan@gmail.com Website: www.mylouisvillekentuckymortgage.com Website: www.mylouisvillekentuckymortgage.com  Address: 911 Barret Ave, Louisville, KY 40204 Address: 911 Barret Ave, Louisville, KY 40204NMLS #57916 | Company NMLS #1738461 |

| Free Info & Homebuyer Advice → |

|

Kentucky Mortgage Loan Expert

FHA | VA | USDA | KHC Down Payment Assistance | Fannie Mae

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval and program requirements.

|