Kentucky FHA Streamline Refinance: Lower Your FHA Payment With Less Hassle

If you already have an FHA mortgage in Kentucky and you’re searching online for a way to lower your house payment, an FHA Streamline Refinance may be the fastest path to a lower monthly payment. In many cases it requires less documentation than a standard refinance, and it often does not require a new appraisal.

This guide breaks down how an FHA Streamline Refinance works in Kentucky, what “mortgage insurance” (MI) changes mean for your payment, how streamline differs from a regular refinance, and what the closing costs typically look like. Then you’ll see a side-by-side payment example so you can quickly estimate how much you might save.

Call or text 502-905-3708 for a free FHA refinance review (Kentucky only).

Quick links

- What is an FHA Streamline Refinance?

- Streamline vs regular refinance (appraisal and documentation)

- Typical closing costs and “no-cost” options

- Payment example: interest rate vs mortgage insurance

- How to apply in Kentucky

- FAQs

What is an FHA Streamline Refinance?

An FHA Streamline Refinance is a refinance option for homeowners who already have an FHA-insured mortgage. It’s called “streamline” because the process can be simpler than a standard refinance.

In many cases, a streamline can be used to:

- Lower your interest rate and reduce your monthly principal-and-interest payment

- Move from an adjustable-rate to a fixed-rate mortgage (or vice versa)

- Shorten your term (for example, 30 years to 15 years) or adjust the term to fit your budget

- Potentially improve long-term cost if your current FHA mortgage insurance is high

Important: FHA streamline refinances generally require a “net tangible benefit,” meaning the refinance must clearly improve your situation (most commonly a lower payment or more stable terms).

External authority link (FHA basics): HUD.gov

Streamline vs regular refinance in Kentucky

People often ask, “Is streamline the same as a normal refinance?” It’s not. Here’s the practical difference for Kentucky homeowners.

| Category | FHA Streamline Refinance | Regular Refinance (full documentation) |

|---|---|---|

| Who it’s for | Only borrowers with an existing FHA mortgage | FHA, Conventional, VA, USDA refis (depending on eligibility) |

| Appraisal | Often not required (depends on lender/transaction type) | Typically required |

| Income/asset documentation | Often reduced compared to a full refinance (lender overlays may apply) | Full documentation is standard |

| Credit qualification | Can be simplified (lender overlays may require a minimum score) | Full credit underwriting is standard |

| Cash out | Not a cash-out program | Cash-out may be available (program rules apply) |

| Main goal | Lower payment and/or improve terms with fewer steps | Rate/term improvement, payoff liens, or cash-out depending on goals |

If you want to pull equity out, you’re usually looking at a different product (such as an FHA cash-out refinance or another cash-out option). A streamline is built for payment improvement, not cash-out.

Internal link suggestions (add your own URLs):

- Kentucky FHA loan guide (eligibility and rules)

- Kentucky refinance options overview

- FHA mortgage insurance explained

Closing costs for a streamline: what you’ll actually pay

Even when a streamline is “simpler,” there are still real costs. Here are the common categories you’ll see on a Loan Estimate:

- Lender fees (origination/underwriting/processing, if charged)

- Title work and settlement fees

- Recording and state/local charges

- Prepaid interest, escrow setup (taxes/insurance), if applicable

- Mortgage insurance items (depending on FHA rules for your specific case)

Many homeowners search for “no-cost FHA streamline.” What that usually means is the lender credit covers some or all closing costs. It does not mean the refinance is free. A lender credit typically comes with a slightly higher rate. The right choice depends on your break-even timeline and how long you plan to keep the home.

CTA: Call or text 502-905-3708 and I’ll run both options side-by-side: (1) lowest rate, (2) lowest out-of-pocket.

Payment example chart: interest rate vs mortgage insurance

Most borrowers focus only on interest rate. With FHA loans, mortgage insurance can also be a meaningful part of the monthly payment. Below is a simple example to help you compare.

Example assumptions (for illustration only):

- Base loan amount: $200,000

- 30-year term

- Principal and interest only (taxes and insurance not included)

- Mortgage insurance shown as an estimated monthly MI amount

| Scenario | Interest rate | Estimated monthly P&I | Estimated monthly FHA MI | Estimated total (P&I + MI) | Estimated monthly savings |

|---|---|---|---|---|---|

| Current FHA loan (example) | 7.00% | $1,330 | $170 | $1,500 | — |

| Streamline refinance (example) | 5.75% | $1,168 | $135 | $1,303 | $197 |

How to read this:

- The rate reduction lowers principal and interest.

- Mortgage insurance may also change based on FHA rules for your specific FHA case number/endorsement date and the new loan structure.

- Your real payment change depends on your current balance, remaining term, current MI factor, escrow, and pricing on the day you lock.

If you want, I can run your exact numbers and provide a clear “before vs after” worksheet.

How to apply for an FHA Streamline Refinance in Kentucky

Here’s the clean step-by-step path I use with Kentucky FHA homeowners:

- Quick review call (10 minutes): current FHA loan, payment, goals, occupancy, and timeframe.

- Case-specific eligibility check: confirm streamline eligibility and net tangible benefit.

- Pricing options: compare “lowest rate” vs “lender credit/no out-of-pocket” options.

- Disclosures and documentation: provide whatever your lender’s overlay requires (often reduced vs full refi).

- Title work and closing: finalize closing costs, escrows, and signing.

Primary CTA:

Call or text 502-905-3708 for a free Kentucky FHA Streamline Refinance review.

You’ll get a clear estimate of payment savings, costs, and break-even timeline.

External links for topical authority (add as needed):

FAQs: Kentucky FHA refinance questions

Will an FHA streamline refinance require an appraisal in Kentucky?

Often, no. Many streamline refinances are completed without a new appraisal, but lender overlays and transaction specifics can change the requirements.

Can I do an FHA Streamline if my home value is down?

Possibly. Since many streamlines do not require a new appraisal, value changes may not prevent approval. The final answer depends on the lender’s overlay and the exact streamline type.

Can I roll closing costs into the loan?

In many refinance structures, some costs may be financed or offset with lender credit. The right approach depends on your break-even timeline and monthly savings.

Is a streamline always the best refinance choice?

No. If you need cash-out, want to remove mortgage insurance via a different program, or need to restructure debt, a full refinance may be a better fit. The correct recommendation comes from a side-by-side comparison.

Free Kentucky FHA refinance review

Joel Lobb

Mortgage Broker

NMLS #57916

Licensed in Kentucky only

Company NMLS #1738461

Call or text: 502-905-3708

www.nmlsconsumeraccess.org

Not a commitment to lend. All loans subject to credit approval and underwriting. Program guidelines and lender overlays can change without notice. Not affiliated with any government agency, including FHA.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Email –

Email – Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome

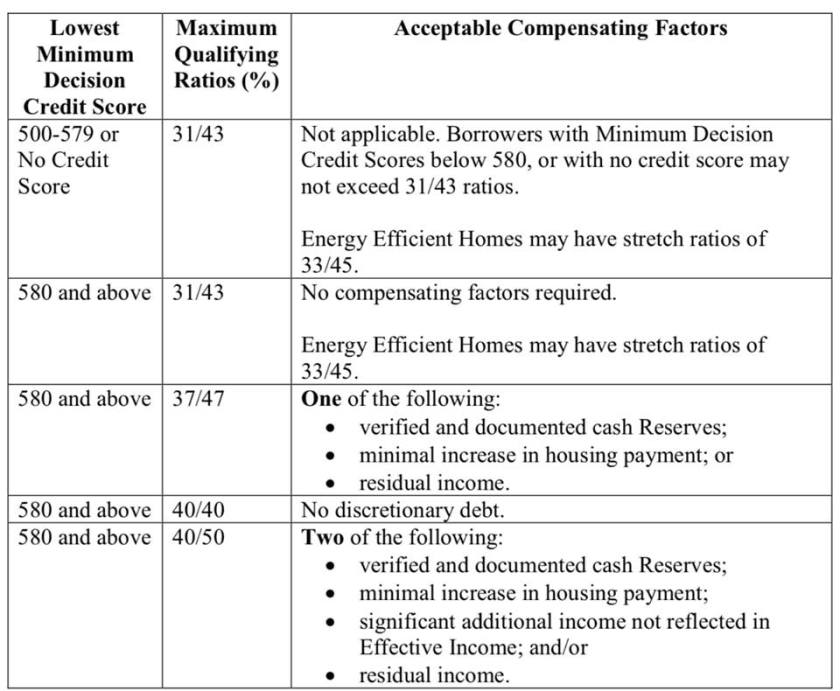

Debt-to-Income Ratio Requirements –Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

Debt-to-Income Ratio Requirements –Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family. Property Requirements for a Kentucky FHA LoanIt must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.It is really not too hard to pass FHA loans and the appraisal process.

Property Requirements for a Kentucky FHA LoanIt must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.It is really not too hard to pass FHA loans and the appraisal process. Pros of FHA Loans –

Pros of FHA Loans –