FHA vs. Conventional Loans: Which Is Better for Kentucky Homebuyers?

Compare FHA and conventional loans for Kentucky homebuyers. Learn credit requirements, down payments, mortgage insurance, and which loan fits your situation.

When comparing FHA loans vs conventional loans in Kentucky, the decision comes down to four core factors: credit score, down payment, debt-to-income ratio, and mortgage insurance. Both loan programs are widely used across Louisville, Lexington, Northern Kentucky, and rural areas, but they serve very different borrower profiles.

FHA Loans: Built for Flexibility

Kentucky FHA loans are designed for buyers who need more flexibility. FHA financing is often a strong option for borrowers with credit scores under 680, limited savings, or little to no cash reserves after closing. FHA also allows buyers to qualify sooner after major credit events, including foreclosures that are three to seven years old and short sales that occurred two to four years ago.

Another major advantage of FHA loans in Kentucky is gifting. The entire down payment and most closing costs can be covered with gift funds from approved sources. This makes FHA especially popular with first-time homebuyers and buyers using down payment assistance programs.

FHA Mortgage Insurance (MIP) Breakdown:

Upfront mortgage insurance premium: 1.75% of loan amount (rolled into the loan)

30-year loans with less than 5% down: 0.85% annually

30-year loans with 5%+ down: 0.80% annually

15-year loans: 0.45% to 0.70% annually (depending on down payment)

Conventional Loans: For Stronger Credit

Kentucky conventional loans are best suited for borrowers with stronger credit and more money saved. Conventional financing generally favors buyers with credit scores above 680, at least five percent down, and reserves remaining after closing. Borrowers with foreclosures over seven years old or short sales that occurred five to seven years ago typically fit conventional guidelines more easily.

One of the biggest advantages of conventional loans is mortgage insurance flexibility. Unlike FHA, there is no upfront mortgage insurance premium. Monthly private mortgage insurance can be lower for borrowers with strong credit, and PMI automatically drops off once the loan reaches roughly 80 percent loan-to-value. FHA mortgage insurance, by contrast, usually lasts for the life of the loan when the down payment is less than ten percent.

Quick Comparison Table

Factor

FHA Loans

Conventional Loans

Credit Score Required

580+ 3.5% down payment (some lenders 500+ 10% down payment)

720+ typically

Down Payment

3.5% (with 580+ score)

3-5% minimum, typically 5%

Mortgage Insurance

Required on all loans (lifetime with <10% down)

Only if less than 20% down; drops at 80% LTV

Upfront Insurance Premium

1.75%

None

Gift Funds

100% of down payment allowed

Limited or restricted

Max Debt-to-Income

Up to 56.99% (with compensating factors)

Typically 45%

Property Types

Owner-occupied only

Owner-occupied and investment

Appraisal Standards

Stricter

More flexible

The Bottom Line

FHA loans are ideal for Kentucky buyers rebuilding credit, using gift funds, or purchasing with limited savings. Conventional loans reward borrowers with stronger credit, larger down payments, and long-term equity goals.

Most homeowners do not keep a mortgage for 30 years. Because many refinance or sell within five to seven years, FHA’s lifetime mortgage insurance is often less of a concern than it appears on paper. In many cases, the lower interest rate and easier approval standards outweigh the insurance cost.

Joel Lobb

Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae

EVO Mortgage • Helping Kentucky Homebuyers Since 2001

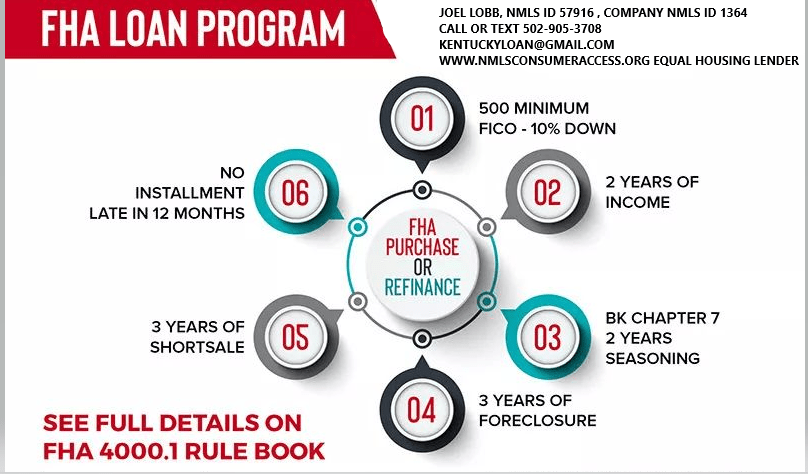

FHA loans are a popular choice for many first-time homebuyers in Kentucky. This is due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

Credit Score Requirements:

FHA loans are known for accommodating borrowers with lower credit scores. The minimum required credit score can vary. Typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. Borrowers with credit scores between 500 and 579 might still qualify. They will need a higher down payment, usually around 10%.

Down Payment:

The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

Work History:

Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history is beneficial. It is preferable to have worked with the same employer or within the same field. This helps demonstrate financial stability and the ability to repay the loan.

Debt-to-Income Ratio (DTI):

The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income. It can go higher up to 56% with good credit scores, a large down payment, or a shorter-term loan. Lenders may also consider higher ratios in certain cases if compensating factors are present.

Bankruptcy and Foreclosure:

FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years. This is possible if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

Mortgage Term:

FHA loans offer various mortgage term options, including 15-year, 20 year, 25 year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

Occupancy: Primary residences with 1-4 units. Not for investment properties or second homes.

Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

can be used for refinances, not only for purchases.

No income limits nor property restrictions on where home is located

Can close within 30 days typically with good appraisal and title work

FHA Loan Requirements in Kentucky for Credit scores, Down payment, Debt Ratio and work history below

Requirement

Details

Credit Score

– 580+: Eligible for a 3.5% down payment. – 500-579: Requires a 10% down payment.

Down Payment

Minimum of 3.5% for qualified buyers; 10% for lower credit scores below 580 to 500 score range

Debt-to-Income Ratio (DTI)

– Ideal: 45% or lower on front end ratio or housing ratio. – Acceptable: Up to 57% with compensating factors. There are two ratios. Front end and back end with front end being maxed at 45% and the backed end ratio being 56.99% with an AUS approval. If manually underwritten, see guidelines here

Employment History

Must provide at least **2 years of consistent employment—College transcripts can supplement with a less than 2 year work history

Key Benefits of FHA Loans in Kentucky

Low Credit Score Requirements

FHA loans accept borrowers with credit scores as low as 500. However, a score of 580+ qualifies you for the lowest down payment option.

Low Down Payment Options

You can purchase a home with as little as 3.5% down if you meet credit requirements, making FHA loans more accessible than conventional loans.

Competitive Interest Rates

FHA loans typically offer rates comparable to conventional mortgages. They may even offer lower rates. This could save you money over the life of the loan.

Flexible Loan Uses

With an FHA 203(k) loan, you can bundle home purchase and renovation costs into a single mortgage.

Assumable Loans

FHA loans can be transferred to a new buyer. This feature is especially valuable if you sell your home when interest rates are higher.

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can provide valuable guidance. They offer assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

Any questions, please don’t hesitate to reach out via, text, email, or call. Advice is always free.

One of Kentucky’s highest rated mortgage loan officers for FHA, VA, USDA, Kentucky Housing KHC and conventional mortgage loans.

Evo Mortgage Company NMLS# 1738461 Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. (www.nmlsconsumeraccess.org).

Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans

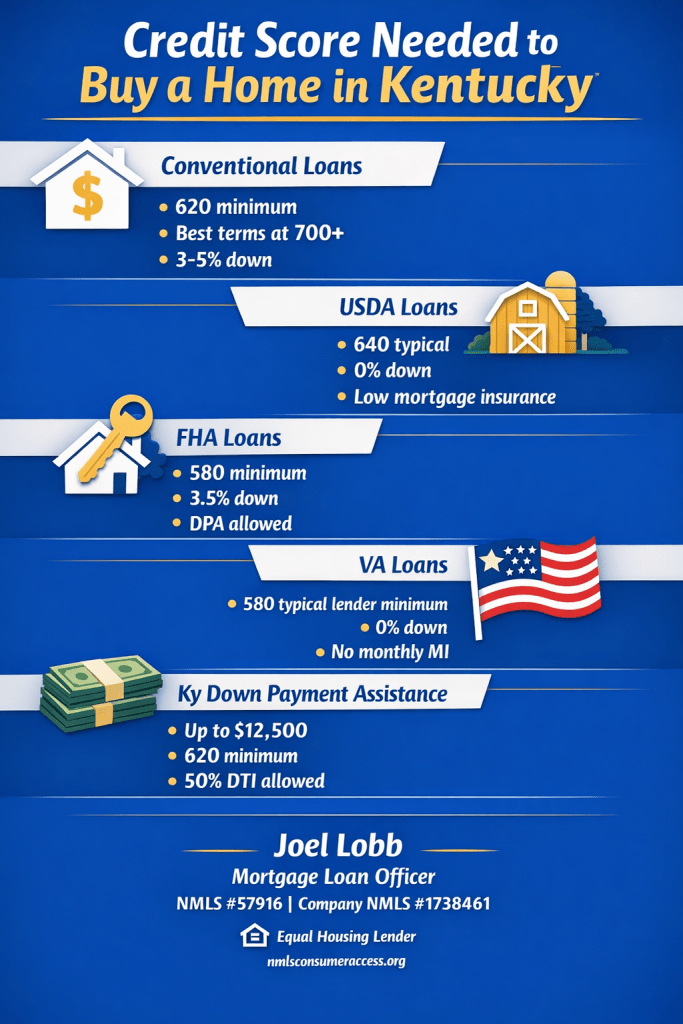

What Credit Score Do You Need to Buy a House in Kentucky?

There is no single “magic number.” The credit score needed depends on the loan program (Conventional, USDA, FHA, VA, or Kentucky Housing Corporation down payment assistance). Here’s how it works in the real world for Kentucky buyers.

Quick guide: typical credit score ranges and key highlights by Kentucky mortgage program.

Conventional Loans in Kentucky

Minimum credit score generally starts at 620.

Most lenders prefer higher scores for 3%–5% down options.

Best pricing and easier approvals are typically with strong credit (often 700+).

Mortgage insurance (PMI) usually improves as scores increase.

USDA Rural Housing Loans in Kentucky

Many lenders target around 640 for automated approval through GUS (Guaranteed Underwriting System).

Manual underwriting may be possible when automated approval is not available.

0% down payment required (eligible rural/suburban areas).

Typical fees include a 1% upfront guarantee fee and 0.35% annual fee (paid monthly).

USDA can be one of the best value options for Kentucky buyers with limited cash, provided the property is in an eligible area and the file meets income and underwriting requirements.

Kentucky FHA Loans

As low as 580 credit score with 3.5% down (typical baseline).

Gift funds, grants, and down payment assistance may be allowed.

Mortgage insurance is generally higher than USDA or VA, but rates can still be competitive.

Common waiting periods: 2 years after bankruptcy and 3 years after foreclosure (standard guideline).

Kentucky VA Loans

VA does not set a minimum credit score in its guidelines, but most lenders do.

Many VA lenders target around 580+ (lender overlay varies).

0% down and no monthly mortgage insurance.

Clear CAIVRS is required (for federal delinquency screening).

Kentucky Down Payment Assistance (KHC)

Kentucky Housing Corporation (KHC) often offers up to $12,500 down payment assistance (program terms and funding can change).

Typically structured as a second mortgage paid back over 15 years.

Minimum credit score is commonly 620 across many KHC options; KHC conventional often requires 660.

Maximum debt-to-income ratios are commonly around 50/50 (program and investor rules apply).

Next step: get a clear pre-approval target

If you share your approximate credit score range, income type, and whether you’re looking in Louisville, Lexington, or rural Kentucky, I can point you to the most realistic program and the exact score threshold that will matter for approval.

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “What credit score do I need to buy a house in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “It depends on the loan program. Conventional financing often starts around 620, USDA lenders commonly target about 640 for automated approval, FHA can allow down to 580 with 3.5% down, and many VA lenders look for around 580 even though VA does not publish a minimum score. Kentucky Housing Corporation down payment assistance commonly requires around 620 (and KHC conventional often around 660). Final approval also depends on income, debt-to-income ratio, and underwriting findings.”

}

},

{

“@type”: “Question”,

“name”: “Can I buy a home in Kentucky with a 580 credit score?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Often yes, depending on the full file. FHA commonly allows 580 with 3.5% down and can work well when you have limited savings or are using gift funds or down payment assistance. Lender overlays and underwriting results still apply.”

}

},

{

“@type”: “Question”,

“name”: “Is 640 a good credit score for a Kentucky mortgage?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “A 640 score can be workable for several programs. USDA lenders often target around 640 for automated approvals, and conventional approvals may be possible starting at 620, though terms improve as scores rise. Your debt-to-income ratio, income stability, and cash to close will strongly influence results.”

}

},

{

“@type”: “Question”,

“name”: “What credit score do I need for a USDA loan in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Many lenders prefer around 640 to obtain an automated approval through the USDA Guaranteed Underwriting System (GUS). Manual underwriting may be possible in some cases, but it is typically more restrictive on ratios and documentation.”

}

},

{

“@type”: “Question”,

“name”: “Does the VA require a minimum credit score in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “VA guidelines do not publish a minimum credit score, but lenders usually do. Many VA lenders commonly target around 580 or higher, depending on the overall file and lender overlays.”

}

},

{

“@type”: “Question”,

“name”: “What credit score is needed for Kentucky Housing Corporation (KHC) down payment assistance?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “KHC program requirements vary, but a common minimum is around 620 for many options. KHC conventional commonly requires around 660. Eligibility also depends on income limits, purchase price limits, and underwriting findings.”

}

}

]

}

What Credit Score Do You Need to Buy a House in Kentucky?

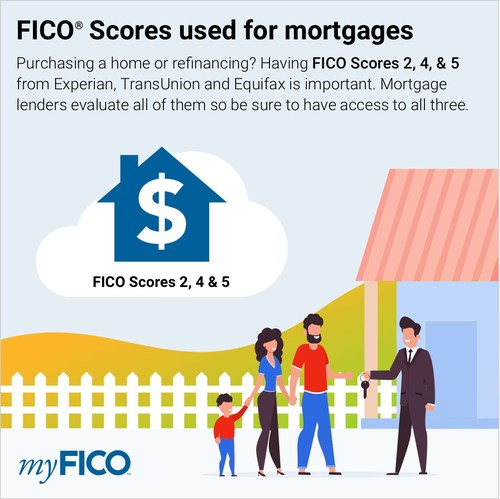

FICO is used by 90% of lenders, according to myFICO, and has been around

since 1989. (VantageScore only hit the scene in 2006.)

If you’re not sure which scoring model a lender will use, just ask!

FICO Scores used for mortgages

USDA loan:

Most lenders prefer at least a 620

The U.S. Department of Agriculture insures for low- to moderate-income homebuyers. The USDA does not set a minimum credit score requirement and does not require a down payment.

Conventional loan:

620 is the minimum but in reality most will need a 720 or higher for a pre-approval if you are putting down less than 20%

Conventional loans aren’t insured by a government agency either, but they are covered by mortgage loan companies Fannie Mae and Freddie Mac. The down payment amount varies.

VA loan:

Most lenders prefer at least a 580

A Veterans Affairs loan is backed by the U.S. Department of Veterans Affairs and meant for military members and their spouses. These loans don’t require a minimum score or money down.

FHA loan:

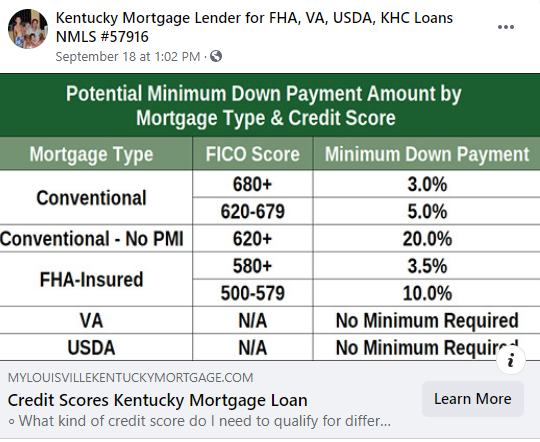

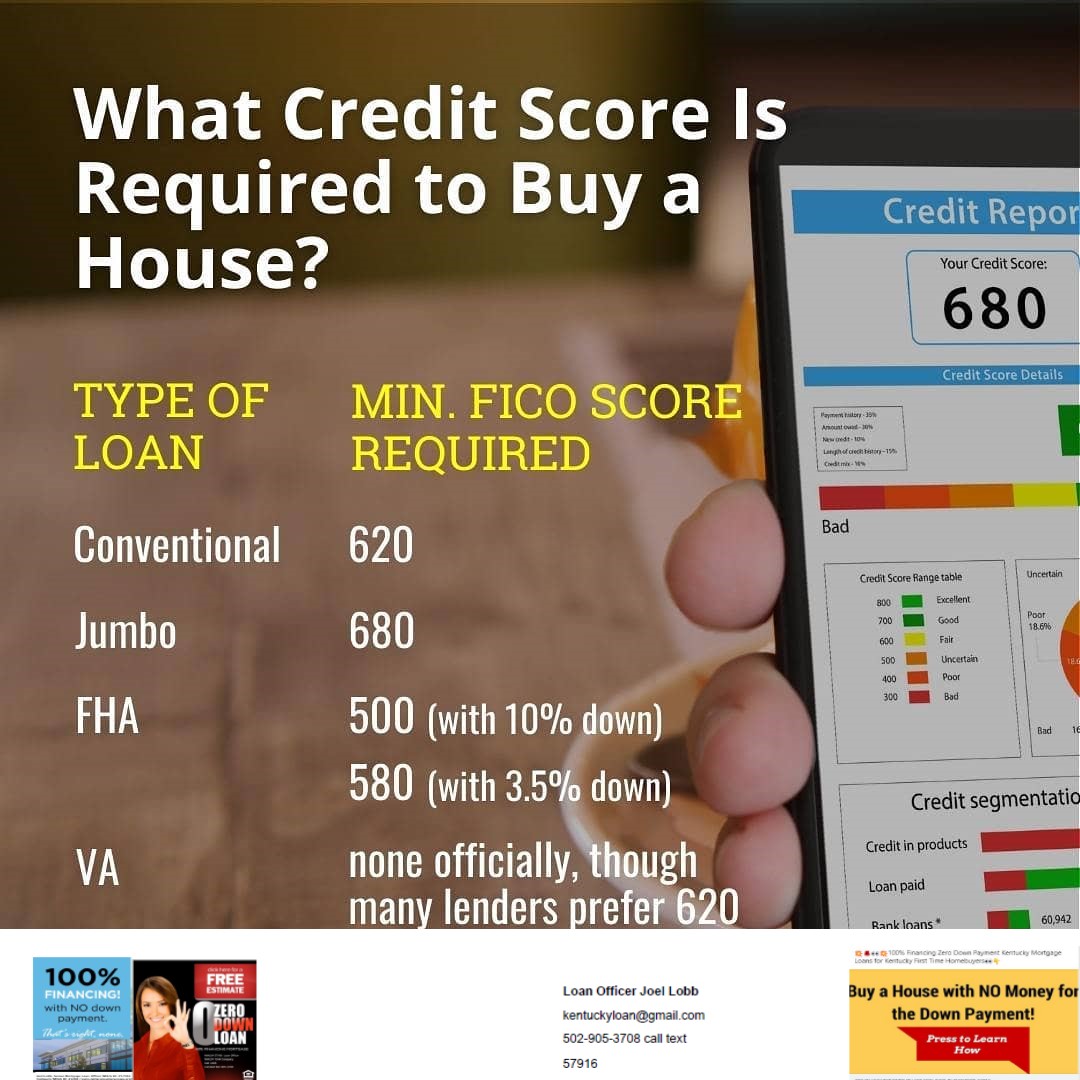

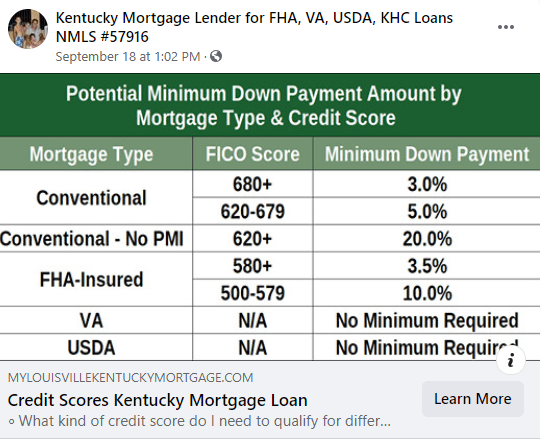

500 (with 10% down payment) or 580 (with 3.5% down payment)

FHA loans, those guaranteed by the Federal Housing Administration, are for higher-risk borrowers who have poor credit and little money saved for a down payment. The credit requirements can fluctuate based on how much of a down payment you can afford.Most lenders have overlays now wanting a minimum 620 credit score even for FHA loans.

Are you interested in seeing how your current credit score might affect a new mortgage?

Let’s take a look together.

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

What Will My Lender Use? FICO is used by 90% of lenders, according to myFICO, and has been around since 1989. (VantageScore only hit the scene in 2006.) If you’re not sure which scoring model a lender will use, just ask! USDA loan: Most lenders prefer at least a 620 The U.S. Department of Agriculture … Continue reading Credit Score Information For Kentucky Home buyers

What credit score is needed to buy a house in Kentucky?

Ultimately, there is no singular credit score that can guarantee you a mortgage approval. Each lender is free to set their own credit score requirements.

But many loan types are insured by government organizations. And lenders cannot accept borrowers with credit scores below the minimum these organizations set. The four most popular home loan types are:

Conventional: Not backed by any government agency, but must meet the Fannie Mae and Freddie Mac underwriting guidelines

FHA: Loans backed by the Federal Housing Administration

VA: Loans backed by the US Department of Veterans Affairs (for military members)

USDA: Loans backed by the US Department of Agriculture (for low- to moderate-income families who buy homes in rural areas)

And here are the minimum credit score requirements for each of these loan types:

Conventional:

620 SCORE NEEDED. BUT TO GET APPROVED FOR A FANNIE MAE LOAN MOSTLY LIKE YOU WILL NEED A 720 SCORE OR HIGHER IF YOU HAVE LESS THAN 20% EQUITY POSITION OR LESS THAN 20% DOWN PAYMENT DUE TO PRIVATE MORTGAGE INSURANCE

FHA:

580 for a 3.5% down payment

500 for down payments of at least 10%

**MOST FHA LENDERS WILL WANT A 580 to 620 CREDIT SCORE NOWADAYS

VA:

No minimum BUT MOST VA LENDERS WILL WANT A 580 to 620 CREDIT SCORE

USDA:

No minimum, but with a credit score of at least 620 to 640 you could qualify for streamlined credit analysis and chances of approval goes way down if score is below 640…

When you think credit score, you probably think FICO Since the Fair Isaac Corporation introduced its FICO scoring system in 1989, “What is my FICO score?” has become a common question. FICO scores have burrowed their way into all kinds of lending decisions, most notably mortgages, credit cards, and rentals.

But over the last decade or so, FICO’s market dominance has been challenged by a newcomer called VantageScore. As the result of a collaboration between the three major credit reporting agencies (CRAs) — Experian, Equifax, and TransUnion — VantageScore uses similar scoring methods to FICO but with slightly different results.

So what are the differences, and more importantly, do they really matter to you, the consumer? The short answer: usually no. But you might want to look at different scores for different needs or goals.In this article, we’ll cover the five main differences between FICO and VantageScore and tell you which one to watch.

What credit score is needed to buy a house?

1. Difference in scoring models

FICO and VantageScore aren’t the only scoring models on the market. Lenders use a multitude of scoring methods to determine your creditworthiness and make financial decisions. But despite the numerous options, FICO and VantageScore are likely the only scores you’ll ever personally see.How do FICO and VantageScore rate you? Both use the same basic criteria:

Payment history

Length of credit

Types of credit

Credit usage

Recent inquiries

Although both FICO and VantageScore consider much of the same information, they gather their data in different ways.

FICO bases its scoring model on credit reports from millions of consumers at once. They gather these reports from the three major credit bureaus and analyze the reports’ anonymous consumer data to generate an accurate scoring model.Alternatively, VantageScore uses a combined set of consumer credit files, also obtained from those same three credit bureaus, to come up with a single formula.

Both FICO and VantageScore issue scores ranging from 300 to 850. In the past, VantageScore has used a range of 501 to 990, but the range was adjusted when VantageScore 3.0 was issued in 2013. VantageScore’s numerical rankings now match FICO’s, which makes it easier for consumers and lenders to implement the VantageScore model — plus, it’s less confusing for consumers who check both their FICO score and VantageScore.

2. Variance in scoring requirements

If you don’t have a long history of credit, VantageScore is the score you want to monitor. Before it’s able to establish your credit score, FICO requires at least six months of credit history and at least one account reported to a CRA within the last six months. VantageScore only requires one month of history and one account reported within the past two years.

Because VantageScore allows a shorter credit history and a long period for reported accounts, it’s able to issue credit ratings to millions of consumers who wouldn’t qualify for FICO scores. Considering how everyone from employers to landlords wants to see your credit score these days, if you’re new to credit or haven’t been using it recently, VantageScore might be able to prove your trustworthiness before FICO has enough data to issue a rating.

3. Significance of late payments

A history of late payments will impact both your FICO score and your VantageScore. Both models consider these factors:

How recently the last late payment occurred

How many of your accounts have had late payments

How many payments you’ve missed on an account

However, while FICO treats all late payments the same, VantageScore judges them differently — it penalizes late mortgage payments more harshly than other types of credit.If you’ve had late payments on your credit cards, they will have about the same impact on both your FICO and your VantageScore. But if you’ve had late payments on your mortgage, you might find you have a higher FICO score than VantageScore.

4. Impact of credit inquiries

You’ve probably heard you shouldn’t open too many credit cards in a short period of time. One reason for this is every time you apply for a credit card, the lender does a “hard inquiry” to check your creditworthiness.

VantageScore and FICO both penalize consumers who have multiple hard inquiries in a short period of time, and they both do “deduplication.” Deduplication is important for things like auto loans, where your application may be sent to multiple lenders, thereby resulting in multiple inquiries. Both FICO and VantageScore don’t count each of these inquiries separately — they deduplicate them, or consider them one inquiry. However, the timespan they use for deduplication differs.

FICO uses a 45-day span to deduplicate your credit inquiries. VantageScore limits its focus to only a 14-day range. VantageScore also looks at multiple hard inquiries for all types of credit, including credit cards. FICO considers only mortgages, auto loans, and student loans.

Inquiries aren’t your biggest concern when it comes to your credit score, but they do have an impact. If you want to buy a house or a car, restrict hard inquiries as much as possible to avoid lowering your credit score.

5. Influence of low-balance collections

VantageScore and FICO both have penalties for accounts sent to collection agencies. However, FICO might give you a bit more of a break when it comes to low-amount collection accounts.

FICO ignores all collections where the original balance was under $100. It also doesn’t count collection accounts you’ve paid off. VantageScore, on the other hand, ignores only paid collection accounts, regardless of the original balance amount.

Keep your credit high

Regardless of the differences between FICO and VantageScore, the essential advice for keeping your credit score high remains the same:

Avoid late payments. Pay your bills, and pay them on time.

Keep your credit balances low. Don’t max out your credit cards, and try to keep your cumulative balance to less than 30% — the lower the better.

Apply for new credit only when you have to. Don’t open a bunch of new cards in a short period of time, and don’t close old accounts without good reason.

Which credit scores do mortgage lenders use to qualify people for a mortgage?

While it’s common knowledge that mortgage lenders use FICO scores, most people with a credit history have three FICO scores, one from each of the three national credit bureaus (Experian, Equifax, and TransUnion).

Which FICO Score is Used for Mortgages

Most lenders determine a borrower’s creditworthiness based on FICO® scores, a Credit Score developed by Fair Isaac Corporation (FICO™). This score tells the lender what type of credit risk you are and what your interest rate should be to reflect that risk. FICO scores have different names at each of the three major United States credit reporting companies. And there are different versions of the FICO formula. Here are the specific versions of the FICO formula used by mortgage lenders:

Equifax Beacon 5.0

Experian/Fair Isaac Risk Model v2

TransUnion FICO Risk Score 04

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

Which Score Gets Used?

Since most people have three FICO scores, one from each credit bureau, how do lenders choose which one to use?

For a FICO score to be considered “usable”, it must be based on adequate, concrete information. If there is too little information, or if the information is inaccurate, the FICO score may be deemed unusable for the mortgage underwriting process. Once the underwriter has determined if a score is usable or not, here’s how they decide which score(s) to use for an individual borrower:

If all three scores are different, they use the middle score

If two of the scores are the same, they use that score, regardless of whether the two repeated scores are higher or lower than the third score

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

If it helps to visualize this information:

Identifying the Underwriting Score

Example

Score 1

Score 2

Score 3

Underwriting Score

Borrower 1

680

700

720

700

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc. 10602 Timberwood Circle Suite 3 Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

Joel Lobb, American Mortgage Solutions (Statewide)

Joel has worked with KHC for 12 of his 20 years in the mortgage lending business. Joel said, “A lot of my clients would not have been able to purchase a home of their own or possibly delayed their purchase due to lack of down payment but with the $6,000 DAP loan program, this gets them into a house sooner and starts their path to homeownership while building equity instead of throwing their money away.”

Call/Text: 502-905-3708

Call/Text: 502-905-3708 Email: kentuckyloan@gmail.com

Email: kentuckyloan@gmail.com Website: www.mylouisvillekentuckymortgage.com

Website: www.mylouisvillekentuckymortgage.com

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Email –

Email – Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome