Is an Kentucky FHA loan right for you?

Here are some benefits of Kentucky FHA loans 🤩

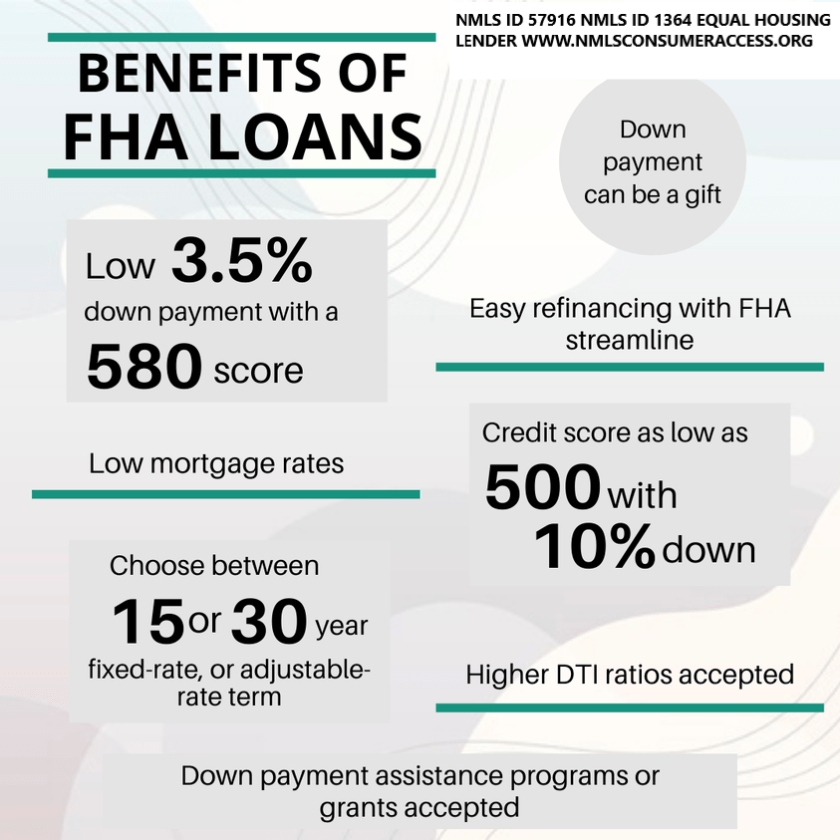

✅ Low down payment options

✅ Down payment assistance programs available

✅ Higher DTI ratios acceptedFHA requires you to establish that the income is in fact stable. I am covering Time on Job, Part Time Income, Seasonal Income and Job Gaps below.Time on JobThere is not a minimum length of time a borrower must have held a position for the income to be eligible. However, the application must identify the most recent 2 years of employment.If the borrower’s employment history indicates that they were in school or in the military, then the borrower must provide evidence supporting this such as college transcripts or discharge papers.The current type of employment has to be supported by the college transcripts or discharge papers showing that he borrower’s training enabled them to gain employment in their field of training.Part Time Income

Part-time and second job income can be used to qualify if documentation is obtained to prove that the borrower has worked the part-time job uninterrupted for the past two years, and plans to continue.For Qualifying purposed, “part-time” income refers to jobs taken to supplement the borrower’s main income from regular employment, such as a second job that is less than 40 hours per week.Income: Is averaged over the previous 2 years. If there was a pay rate increase and we can document the increase in pay, you can average the new pay rate over 12 months.Seasonal IncomeSeasonal income may be acceptable for qualifying. It is not unusual to have out-of-season income from unemployment income. If the borrower has a 2 year history and continuance is probable, this type of income may be allowed to qualify the borrower.The key here is history and continuance.Job GapsThe borrower must provide a signed explanation for gaps in employment as follows:Income can be considered effective if the following can be verified:1. Borrower has been employed in the current job for at least six months at the time of the case number assignment AND2. A two year work history prior to the absence from employment.What does FHA stand for?

FHA stands for Federal Housing Administration, and the FHA is a government agency that insures mortgages. It was created just after the Great Depression, at a time when homeownership was prohibitively expensive and difficult to achieve because so many Americans lacked the savings and credit history to qualify for a loan. The government stepped in and began backing mortgages with more accessible terms. Approved lenders began funding FHA loans, which offered more reasonable down payment and credit score standards.

Today, government-backed mortgages still offer a safety net to lenders—because a federal entity (in this case, the FHA) is guaranteeing the loans, there’s less financial risk if a borrower defaults on their payments. Lenders are then able to loosen their qualifying guidelines, making mortgages available to middle and low income borrowers who might not otherwise be approved under conventional standards.

What’s the difference between FHA and conventional loans?

Home loans fall into two broad categories: government and conventional. A conventional loan is any mortgage that is not insured by a federal entity. Because private lenders assume all the risk in funding conventional loans, the requirements to qualify for these loans are more strict. Generally speaking, FHA loans might be a good fit if you have less money set aside to fund your down payment and/or you have a below-average credit score. While low down payment minimums and competitive interest rates are still possible with a conventional loan, you’ll need to show a strong credit score to qualify for those advantages.

Each loan type has advantages and disadvantages—including different mortgage insurance requirements, loan limits, and property appraisal guidelines—so choosing the one that works best for you really depends on your financial profile and your homebuying priorities.

FHA loans pros and cons

FHA loans are meant to make homeownership more accessible to people with fewer savings set aside and lower credit scores. They can be a great fit for some borrowers, particularly first time homebuyers who often need lower down payment options, but you should weigh the costs and benefits of any mortgage before committing. Here’s a breakdown of the key pros and cons when it comes to FHA loans:

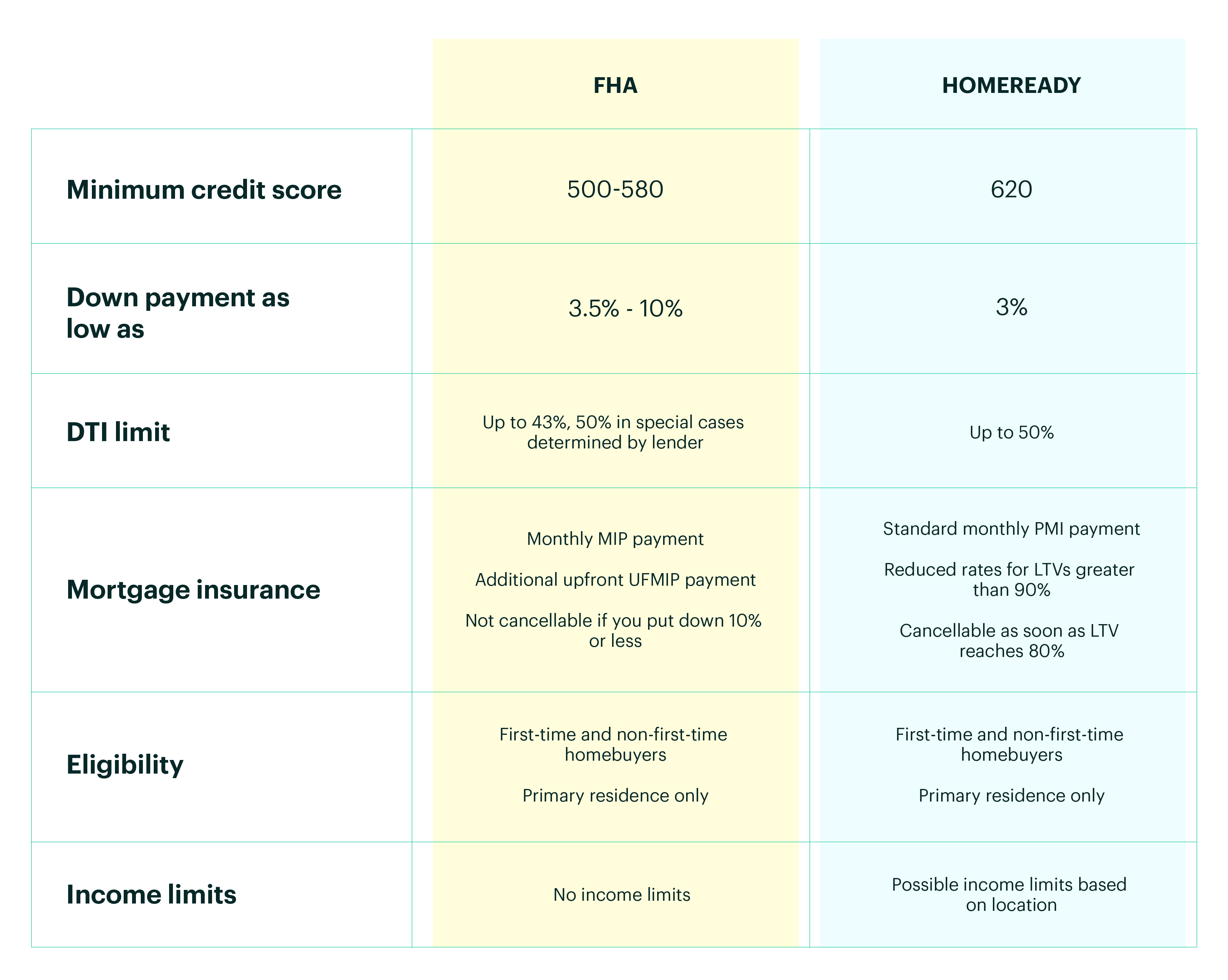

Pros Cons Low down payment. Down payments make up the majority of cash to close in any purchase loan, and saving up for one can be a significant barrier for some borrowers. FHA loans make it possible to put down as little as 3.5% upfront and still get competitive rates. Mandatory MIP payments. FHA loans are more lenient, but they also come with insurance costs to mitigate risk to the lender. You’ll have to pay Mortgage Insurance Premiums (MIP) no matter what—either for 11 years or for the life of your loan, depending on your down payment. Lower credit score. Credit scores can be a major hurdle when it comes to conventional loans, but borrowers with credit scores starting at 500 can qualify for FHA loans. Less competitive. Sometimes sellers can be more hesitant to accept FHA loans. In a competitive market, you might not win out against conventional loan bids. Higher DTI accepted. Your debt-to-income (DTI) ratio gives lenders an understanding of other major financial obligations in your life. This ratio is a key factor in any loan application because it indicates your ability to afford a mortgage based on current household income and existing debt. Again, FHA loans offer more leniency here and borrowers at or below 43% DTI can qualify. Stricter property standards. To offset risk and further protect lenders, FHA loans have strict criteria when it comes to assessing the condition of any property being purchased with an FHA loan. The downside? The house you want to buy might not qualify for an FHA loan. The upside? You’re less likely to be financially burdened by a home that requires expensive repairs or updates. No income limitations. It’s a common misconception that FHA loans are only available to first-time homebuyers or borrowers with limited income—but they’re not. There’s no maximum income limit that would disqualify you from this type of loan. Loan limits: FHA loan limits are typically lower than conventional loan limits, which means you might not be able to get funding for more expensive houses. This isn’t necessarily a bad thing, since it helps ensure that borrowers get loans they can afford to repay. How to qualify for an FHA loan

Qualifying for an FHA loan is generally easier than qualifying for a conventional loan, but you’ll still need to meet some basic minimum standards set by the FHA. While the government insures these loans, the funding itself comes through FHA-approved lenders each lending institution may have slightly different qualifying guidelines for its borrowers. Keep in mind that, while these FHA standards offer a basic framework, you’ll need to confirm the individual qualifying rules with your specific lender.

Credit score minimum 500. Your exact credit score will play a big role in determining your down payment minimum; typically, the higher your credit score, the lower your down payment and the more favorable your interest rate.

Debt-to-income ratio at or below 56.9%. DTI is a standard way of comparing the amount of money you earn to the amount you spend paying off other debts, and FHA loans are more lax on this number.

Steady income and proof of employment. Being able to provide at least 2 years of income and employment records is a standard requirement for all loans.

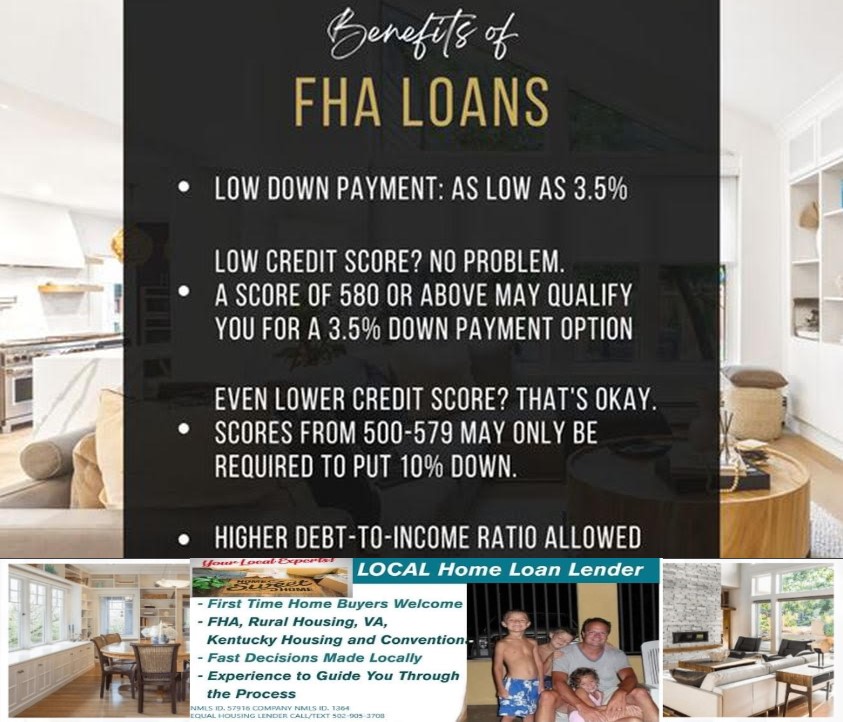

Down payment between 3.5%-10%. The down payment minimum for an FHA loan is typically lower than conventional loan, and can be as little as 3.5% depending on your credit score and lender.

Property standards apply. You won’t qualify for an FHA loan if the house you want to buy doesn’t pass the appraisal process, which is more strict with this type of loan than conventional mortgages.

Maximum FHA loan amount. The amount of money you borrow cannot exceed the FHA loan limits; this number changes based on your county and is determined by how expensive the local market is; the maximum FHA loan limit in 2021 is $420,000 (check HUD resources to confirm the latest limits.)

Joel Lobb

Senior Loan Officer

(NMLS#57916)American Mortgage Solutions, Inc.

10602 Timberwood Circle, Suite 3

Louisville, KY 40223text or call my phone: (502) 905-3708

email me at kentuckyloan@gmail.comThe view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency.

The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (http://www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.

Bank Statement Basics for A Kentucky Mortgage Loan Approval for USDA, KHC, FHA, VA, Fannie Mae and Rural Housing Mortgage Loans

-

Assets:

- Assets are not required; however, any assets disclosed must be supported with appropriate documentation

- Satisfactory explanation and documentation should be provided for large deposits or increases in liquid assets

- Cash on hand is not acceptable

- Bank accounts require Verification of Deposit with average 2 month balance, or 2 consecutive months statements dated within 45 days of loan application

- Earnest money deposit may be considered an asset if deposit is not already reflected in liquid assets

- Asset amount of retirement accounts is 60% of the vested account balance

- Gifts must be documented through gift donor letter and establish that gift does not have to be repaid

- For sale proceeds of real property, provide HUD-1 or equivalent closing statement to indicate the actual amount of cash proceeds realized by the borrower

- Stocks and bonds must be documented by a statement provide by stockbroker or financial institution managing the portfolio

- Households with net family assets of greater than $5,000 require that the actual income derived from all net family assets or a percentage of the value of such assets based on the current passbook savings rate be considered when calculating income.

- Government shutdown affects on USDA, FHA, VA, Rural Housing, KHC and Fannie Mae Mortgage loans in Kentucky (mylouisvillekentuckymortgage.com)

- Kentucky Housing Corporation (KHC) homeownership programs affected by the current federal government shutdown (mylouisvillekentuckymortgage.com)

- Louisville Ky Mortgage Lender FHA/VA KHC USDA Kentucky Mortgage: Kentuck… (mylouisvillekentuckymortgage.com)

Give us a try or let us compare your options on your next mortgage transaction. Call me locally at 502-905-3708. Free Mortgage Pre-Qualifications same day on most applications.

Email me at kentuckyloan@gmail.com with your questions

I specialize in Kentucky FHA, VA ,USDA, KHC, Conventional and Jumbo mortgage loans. I am based out of Louisville Kentucky. For the first time buyer with little money down, we offer Kentucky Housing or KHC loans with down payment assistance.

This website is not an government agency, and does

not officially represent the HUD, VA, USDA or FHA or any other government agency.

NMLS# 57916 http://www.nmlsconsumeraccess.org/

Joel Lobb Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

phone: (502) 905-3708

Fax: (502) 327-9119

kentuckyloan@gmail.com

Company ID #1364 | MB73346E

EQUAL HOUSING LENDER

Kentucky HUD Homes for Sale with the FHA $100 Down Program

KENTUCKY HUD HOMES SALES INCENTIVES

| For a limited time, FHA offers sales incentives on HUD homes that will make these homes more affordable for home buyers when purchasing a property using FHA-insured financing. The incentives VARY from State to State but may include low down payments; sales allowances that can be used to pay closing costs, make repairs, or pay down the mortgage amount; broker bonuses for owner-occupant sales. The benefits of FHA financing are low down payments; competitive interest rates; flexible credit qualifying. To find a HUD-Approved Lender, and for the latest sales incentives in your areas, visit HUDhomestore.com The program incentives are subject to change without prior notice. | |

|

Sales Incentives (subject to change without prior notice) |

Participating States |

|

$100 Down Payment! Available to Owner Occupant Homebuyers when purchasing a property using FHA-insured financing. |

Kentucky HUD Homes for Sale By FHA |

Search Results for HUD Homes in KY |

|

201-405318 409 Mildred Ave South Shore, KY 41175 Greenup County |

201-585835 2215 Sharon Rd Ashland, KY 41101 Boyd County |

_68633759.JPG) 201-648672 882 Whippoorwill Ro Paintsville, KY 41240 Johnson County |

201-443322 99 Falls Br Belfry, KY 41514 Pike County |

201-612315 2718 Cumberland Ave Ashland, KY 41102 Boyd County |

201-654741 801 E Broad Street Central City, KY 42330 Muhlenberg County |

201-492365 9655 Marshall Rd Ryland Hght, KY 41015 Kenton County |

201-619887 2878 1st Street Petersburg, KY 41080 Boone County |

201-662018 711 Aqua Shores Dr Shelbyville, KY 40065 Shelby County |

201-569915 1840 Holman St Covington, KY 41014 Kenton County |

201-631020 465 Kennedy Rd New Haven, KY 40051 Larue County |

201-663813 1501 Old Henderson Rd Providence, KY 42450 Webster County |

201-574687 2444 Bardstown Rd Lawrenceburg, KY 40342 Anderson County |

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

https://www.mylouisvillekentuckymortgage.com/

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Kentucky FHA Mortgage Insurance Requirements and Down Payments

FHA mortgage insurance, typically referred to as MIP, is the one closing cost that is unique to FHA mortgage programs.

**Every FHA mortgage must have mortgage insurance regardless

of the amount of the down payment.**

There are two types of mortgage insurance for FHA insured loans – Up-front Mortgage Insurance Premiums and Monthly Mortgage Insurance Premiums.

Up-front Mortgage Insurance Premium (UFMIP)

UFMIP is calculated at 1.75% of the base loan amount on all loans, regardless of the down payment amount. This insurance protects the lender against losses in the event that the borrower defaults on the loan.

**The entire amount of the UFMIP can be financed into the loan amount!**

For example:

- If the FHA loan amount is $100,000 (base loan amount)

- The mortgage insurance premium would be $1,750 ($100,000 x 1.75%)

- The mortgage amount including MIP would be $101,750 ($100,000 + $1,750)

What really happens during an FHA mortgage transaction is that the borrower owes FHA a lump sum mortgage insurance premium. The lender making the FHA loan will actually lend the money for the premium to the borrower and send the money to FHA so that the mortgage will be insured.

Monthly Mortgage Insurance Premium

In addition to the UFMIP, there may be a monthly premium due as well. The monthly premium is .80% of the base loan amount if the loan amount is less than or equal to 95% of the value of the home. If the loan amount is over 95% of the value of the home, the monthly premium is .85% of the base loan amount..

On a 30 year fixed loan, the monthly payment would be calculated as follows:

$100,000 x .80% = $800 / 12 months = $66.67 per month

FHA Minimum Down Payment

Effective January 1, 2009, the minimum down payment required on an FHA loan is 3.5% of the purchase price.

Any deposit (usually called earnest money) that you are required to give to your realtor at the time of an accepted purchase contract will count towards your 3.5% down payment. The appraisal fee collected at the time of inspection will also count towards your 3.5% down payment.

If, for example, you are purchasing a $100,000 house, your minimum down payment required would be $3,500. If your seller/realtor required you to put down $500 in earnest money on top of the $300 for your appraisal, your down payment would be lowered to $2,700 ($3,500 – $500 – $300 = $2,700).

Down Payment As A Gift

If a borrower does not have 3.5% of his or her own money to put down towards the home purchase, FHA allows that amount to be in the form of a gift to the borrower. The gift must be from a qualified source, such as a family member, employer or significant other. The source of the gift must be able to provide proof that they have the money in an account registered in their name prior to transfer to the borrower.

In some areas, this gift may also be grant money from a state or local municipality, if such funds are available.

What is an FHA Loan and Is It Right for You?

Source: What is an FHA Loan and Is It Right for You?

What Is An FHA Loan And Is It Right For You?

Sponsored by:

The Federal Housing Administration insures what are called FHA loans. These mortgage loans provide opportunities for buyers with less-than-perfect credit or limited down payments to purchase homes, but they aren’t without potential pitfalls.

FHA loans are available to borrowers with a credit score of at least 580, and you have to make a minimum 3.5% down payment. They’re a popular option for first-time home buyers.

Lenders such as banks and credit unions issue the mortgages, which are insured by the FHA. That protects the lender if the borrower defaults, which is why the terms are more favorable than a traditional mortgage.

Around eight million single-family homes have loans insured by the FHA.

What Can an FHA Loan be Used For?

You can use an FHA loan to refinance single-family houses, to buy a single-family home, to buy some multifamily homes and condos and certain mobile and manufactured homes. There are particular types of FHA loans that can be used to renovate an existing property or for new construction.

How is an FHA Loan Different from a Conventional Mortgage Loan?

The biggest differentiator between an FHA loan and a conventional mortgage is that it’s easier to qualify for an FHA loan. You may get a loan with a lower credit score than you would otherwise, and your mortgage insurance payments may be lower too.

There are also fewer restrictions as far as using gifts from family or donations for your down payment.

If you have a FICO score of at least 580, you have to make a 3.5% down payment. With a FICO score between 500 and 579, you’re required to make a 10% down payment, and mortgage insurance is required. Your debt-to-income ratio needs to be less than 43% whereas with a conventional loan it’s usually 36%. You do need to have proof of income and steady employment, as you would need with a conventional loan.

Are There FHA Loan Limits?

There are limits on the mortgage amount you can get with an FHA-guaranteed loan. The limits vary based on your county, and in 2020 these ranged from $331,760 to $765,600. The limit amounts are updated by the FHA each year based on fluctuations in home prices.

The Benefits of the FHA Loan

The primary benefits of an FHA loan are that buyers who wouldn’t otherwise qualify may be able to own a home and for a lower down payment. Sometimes the FHA will help facilitate coverage of closing costs. If you have problems making payments on an FHA loan you may be eligible for a forbearance period if you qualify.

What Are the Downsides of an FHA Loan?

You will have to pay an upfront mortgage insurance premium with an FHA loan to protect the lender. The fee is due when you close and it’s 1.75% of your loan. You will also have to pay an annual mortgage insurance premium for the life of your loan. The amount can range between 0.45% and 1.05%.

When you buy a home with an FHA loan, it has to meet strict standards in terms of health and safety.

Also, while there are set standards from the FHA, approved lenders can create their own requirements.

Applying for an FHA Loan

You’ll have to first find an FHA-approved lender to get one of these home loans. You’ll need some documents, including proof of U.S. citizenship, legal permanent residency, or eligibility to work in America. You’ll need bank statements for at least the past 30 days, and you’ll probably need to show pay stubs.

Some of the information your lender may be able to obtain on your behalf, such as your credit reports, tax returns and employment records.

There are advantages to an FHA loan because it expands homeownership to more people than conventional loans. It’s just important that if you’re considering this loan you understand the costs and that you’re not taking on more than you’re financially prepared for because of the less stringent approval requirements.

Written by Ashley Sutphin for http://www.RealtyTimes.com Copyright © 2020 Realty Times All Rights Reserved.

Kentucky FHA Mortgage Qualifying Guidelines

Kentucky FHA Loans

The FHA is actually not the lender. They insure the loans that are issued by FHA-approved lenders. FHA loans are gear more toward borrower’s with less than 20% down payment and credit issues in the past.

Qualifying for a FHA Loan Mortgage In Kentucky

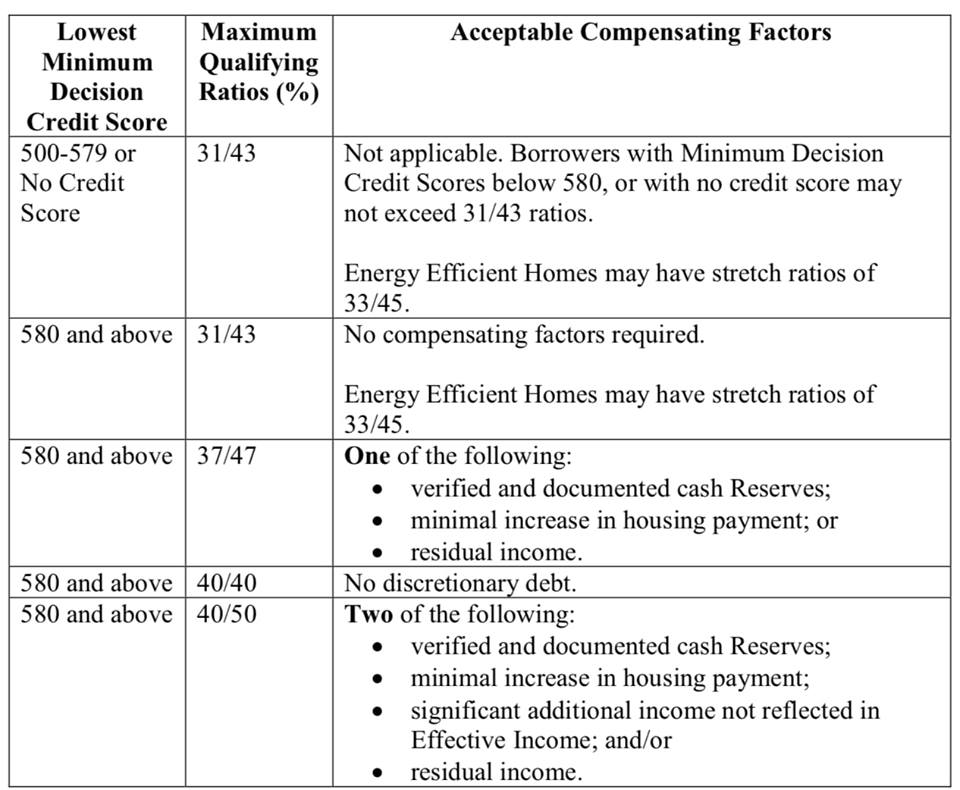

Credit Scores and Down Payment Percentages – Each year, the rules for qualifying for these loans changes. For 2020, applicants need a minimum credit score of 580 in order to get the low down payment, which is 3.5 percent.

For those whose credit score is less than 580, they will have to come up with 10 percent for their down payment. This does not guaranteed a mortgage loan approval if you have the certain credit scores, just a the minimum required.

Compensating Factors for FHA loan Approval

The credit score is just one part of the story. The FHA will also evaluate the borrower’s bankruptcies, foreclosures, prior payment history on other debts. They will also want information on difficulties that kept the borrower from making payments on other debts in the past.

Negative strikes against qualifying for the loan include not having any credit history or a bankruptcy.

Someone with a bankruptcy will have to wait for two or more years after their bankruptcy before applying for an FHA-insured loan.

If you have late payments on debt obligations, it is best to wait until you have had a full year of on-time payments before you apply for a FHA-insured loan.

If you have had a foreclosure in the past, you may still be able to get a FHA-insured loan three years after your foreclosure. The lender will be looking at the circumstances behind the foreclosure.

If you have had any civil judgement against you for money owed, collections actions or unpaid/unresolved federal debt, the FHA-approved lender will be required by the FHA to establish that all of these outstanding issues are resolved or paid before you can go through closing.

Watch out for student loans if they are delinquent because sometime this can cause a lien against you in the form of a CAVIRS Alert with HUD

As you can see, many types of borrowers who would not be eligible for a traditional mortgage, or who would face exorbitant interest rates, will be able to qualify for a FHA-insured loan at attractive interest rates.

Employment and Income for a Kentucky FHA Loan

You must have an employment history that is steady for the last two years. Does not have to be same employer.

Your income has to be verifiable in some way, whether that be through pay stubs, your income tax returns. No bank statements or cash deposits , or undocumented income can be used for income qualifying purposes.

Debt-to-Income Ratio Requirements –

Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.

Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.

If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

Property Requirements for a Kentucky FHA Loan

It must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.

It is really not too hard to pass FHA loans and the appraisal process.

Pros of FHA Loans –

-

New homebuyers and those who have lower credit scores or who have other blemishes on their credit history will often qualify for FHA-insured loans.

-

Even though these borrowers are considered “subprime” to a traditional lender, they will receive attractive interest rates through the FHA-insured mortgage programs.

-

The down payments required from borrowers are lower than those required by traditional mortgage lenders.

-

These loans can be combined with other forms of public assistance for lower income or new borrowers so that the borrower will not need to come up with a down payment of any kind.

Cons of FHA Loans –

-

Since the FHA is not actually the lender, and you have to go through FHA-approved lenders, you may not qualify due to stricter standards that the lender has for the loan.

-

Because you are not paying 20 percent as a down payment, the FHA requires two mortgage insurance premiums to be paid. One is an upfront premium that is 1.75 percent of the loan amount. Lenders often will allow you to make that mortgage insurance premium a part of your loan. The second is an annual mortgage insurance premium that is .45 percent or 1.05 percent. This premium is paid monthly.

FHA FINANCING

CREDIT REQUIREMENTS FOR KENTUCKY FHA FINANCING

What credit score do I need to qualify for a Kentucky FHA loan is one of the most common questions I hear from Kentucky homebuyers?

The short answer is you must have a minimum credit score of 500 to be eligible for an FHA loan in Kentucky. Anything lower than 500 disqualifies you from consideration for an FHA loan.

There are two sets of credit score requirements for a Kentucky FHA Loan

One important thing to understand is that the Federal Housing Administration (FHA) does not lend money directly to home buyers. You will fill out an application with a regular lender just as you would if you were applying for any other type of mortgage. What the FHA does is ensure your loan to help protect the lender in case you default.

You will be required not only to meet the FHA guidelines to qualify for a loan but also meet any additional qualifications required by the lender. This means there are two sets of requirements you have to meet with your credit score.

1. The first set of requirements comes from the Department of Housing and Urban Development (HUD). HUD oversees the FHA and determines what a borrower’s minimum eligibility requirements will be to obtain an FHA loan.

2. The second set of requirements comes from the mortgage lender. The mortgage lender has the right to add its requirements to those mandated by HUD.

What HUD requires of borrowers to be eligible for an FHA loan

The HUD Handbook 4000.1 includes the official guidelines when it comes to the FHA mortgage insurance program.

It states that in 2020 the Kentucky FHA borrowers with credit scores of 580 or higher are eligible for a 96.5% loan with 3.5% down.

Borrowers with credit scores from 500 to 579 are eligible for a 90% loan with 10% down.

Individuals with credit scores below 500 are not eligible for the FHA program.

What lenders may require of borrowers to be eligible for an Kentucky FHA loan

Lenders have the right to add requirements over and above the minimum requirements of HUD. These additional requirements are called overlays. Your lender may or may not require them.

This is not something that should come as a surprise to you, however. Requiring a credit score of 580 to 620 is not unusual. In addition to your credit score, you must have a manageable debt level that lenders are comfortable with and enough income to repay your loan.

What credit score do I need to qualify for FHA loan?

Each month Ellie Mae, the software company processing more than ⅓ of America’s mortgage loans, publishes an insight report for mortgage trends and standards. One of the things they track is average credit scores. The following is their report for November 2019 which shows what percentage of successful borrowers fall into what credit score ranges.

500 – 549 2.14%

550 – 599 5.20%

600 – 649 23.01%

650 – 699 34.74%

700 – 749 21.88%

750 – 799 10.87%

800+ 1.89%

These percentages show that the majority of borrowers who successfully qualify for FHA loans fall into the 600 to 799 range. While it is true that some successfully qualify in the low range of 500 to 599, you have a much better chance of being approved for a loan with good terms and a low down payment if you fall into the higher range.

For your free credit report and analysis call us today at 502-905-3708 or email us at kentuckyloan@gmail.com

Joel Lobb (NMLS#57916)

Senior Loan Officer

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

How does Kentucky FHA Mortgage Rates work?

Kentucky FHA mortgage loans are backed by the Federal Housing Administration under the umbrella of HUD. FHA loans were developed to help borrowers that don’t have a large down payment and a weaker credit profile to buy and refinance their home mortgage loan.

Kentucky FHA rates are backed by the government, so they are typically lower than other mortgage rates in the secondary market like Conventional loans and portfolio loans at banks, but fall in line compatible to other backed government loans in the secondary market likeUSDA, VA, mortgage loans. Most people seeking FHA mortgages will get a 30 year, 20 year of 15 year fixed rate loan with the security of the house payment not changing.

Lower Credit Standards and Credit Scores for FHA loans

FHA mortgages will go down to a 500 credit score with at least 10% down payment, and if your credit score is higher than 580, you can put the minimum of 3.5% down payment. Additionally, you need to be only 2 years removed from a Chapter 7 bankruptcy, or 1 year from a Chapter 13 bankruptcy.

Mortgage Insurance on FHA loans

Mortgage insurance is required on most FHA loans and is usually for life of loan with everyone paying the same. If you have a higher credit score and a larger down payment, it would make sense to look at doing a conventional mortgage loan because they are based on your credit score, money down, and debt to income ratio and not for life of loan.

You can get a lower FHA mortgage insurance premium and not have to finance the premiums for life of the loan if you put more than 10% down payment and finance on a 15 year term.

Why would you consider a FHA mortgage?

My best opinion is this. If you have a bankruptcy that is less than 4 years, have a credit score lower than 660, and very little money down, I would recommend at looking to do a FHA mortgage Loan. Your chances of getting approved with likely result in a loan approval as opposed to doing a conventional loan backed by Fannie Mae.

Why would you consider a Conventional Loan?

My best opinion is this. If you have a bankruptcy over 4 years or longer, at least 5% down payment, a credit score of 680 or higher, I would look doing a conventional mortgage loan.

I can help you understand what mortgage is correct for you. Please contact me below and I will be happy to answer any questions.

Joel Lobb (NMLS#57916)

Senior Loan Officer

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

How to qualify for a Kentucky FHA Home Loan ?

It’s important to understand the different types of loan programs available to you and what benefits and drawbacks there are to each type.

For example, if you’re looking to find a fixer upper this may not be the right loan program for you. But an FHA loan may be a better fit for you if you have little cash saved up for a down payment or if you don’t have a high credit score.

Kentucky FHA loan requirements:

- At least 18 years old to apply

- No age limit. just must be 18 years of age to apply.

- Must occupy the home as a primary residence, no rental homes or investment property

- An appraisal must be done by an FHA-approved appraiser.Typically FHA appraisal in Kentucky costs anywhere from low-end $325 to $525 with most FHA lenders in KY.

- Home inspection is not required

- Termite inspection not required

- 2 years removed from Chapter 7 bankruptcy, and 1 year in Chapter 13 bankruptcy is possible to get a loan while in bankruptcy

- Foreclosure or short sale on previous home mortgage requires 3 years removal from those dates.

- Mortgage insurance (MIP) is required

- Upfront Mortgage Insurance Premium is 1.75% and monthly mortgage insurance is .85% or .80% depending on loan term and loan to value.

- Mortgage insurance is for life of loan.

- No matter your credit scores, everyone pays the same mortgage insurance premiums.

- Must have 2 years of employment history proving a reliable source of income

- 500 FICO score requirement with at least 10% down payment

- 580 FICO score requirement with at least 3.5% down payment

- Gifts and down payment assistance programs are allowed to meet your down payment requirements. Cannot come from seller, but seller can contribute up to 6% of the sales price toward buyer’s closing costs and prepaids.

- Student loan payments are factored into the debt-to-income ratio when applying. Typically if loans are deferred, or in an income=based repayment plan, the FHA underwriters will use 1% of the outstanding balance, which sometimes can make it difficult to qualify.

- Your debt-to-income ratio must not be higher than 31% or total debt obligation cannot be higher than 43% of your current income. This is for a manual underwriter, meaning that if the AUS underwriting system by mortgage lenders will approve you for a higher debt to income ratio, that is fine.

Joel Lobb (NMLS#57916)

Senior Loan Officer

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

|

Student Loans In Collections, What Can I Do to get Approved For A Kentucky Mortgage ?

|

|

FHA eliminates two unnecessary and outdated lending roadblocks

The Federal Housing Administration has taken steps to reduce some of the regulatory burdens that belabor the lending process, releasing two mortgagee letters Tuesday with updated guidelines on home warranty and inspection requirements for single-family FHA loans. FHA Commissioner Brian Montgomery said the moves align with the administration’s goal streamline and update guidelines in an effort to reduce regulatory barriers.

Source: FHA eliminates two unnecessary and outdated lending roadblocks

How to get rid of Mortgage Insurance on a Kentucky Mortgage Loan.

Eliminate FHA Mortgage Insurance On Your Kentucky FHA Loan.

Mortgage insurance premium can add almost $200 to the payment on a $265,000 FHA mortgage. The decision to get an FHA loan may have been the lower down payment requirement or the lower credit score levels, but now that you have the loan, is it possible to eliminate it?

Mortgage Insurance Premium protects lenders in case of a borrower’s default and is required on FHA loans. The Up-Front MIP is currently 1.75% of the base loan amount and paid at the time of closing. Annual MIP for loans with greater than 95% loan-to-value is .85% per year.

For loans with FHA case numbers assigned before June 3, 2013, when the loan is paid down to 78% of the original loan amount, the MIP can be cancelled. The borrower may need to contact the current servicer.

However, for loans greater than 90% with FHA case numbers assigned on or after that date, the MIP is required for the term of the loan.

Most homeowners with FHA mortgages are not eligible to cancel the MIP because they either originated their loan after June 3, 2013, put less than 10% down payment and/or got a 30-year loan. If they have at least 20% equity in the home, they can refinance the home with an 80% conventional loan which in most cases, does not require mortgage insurance.

With normal amortization on a 30-year loan, it takes approximately 11-years to reduce the original loan to the 78-80% requirement based on normal amortization. There is another dynamic involved which is the appreciation on the home. As the home goes up in value and the unpaid balance goes down, the equity increases.

If the homeowners believe that they have enough equity that would eliminate the need for mortgage insurance, they can investigate refinancing with a conventional loan. Borrowers refinancing will incur expenses in starting a new mortgage and the interest rate may be higher than the existing rate. Analysis will determine how long it will take to recapture the cost of refinancing.

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3