Kentucky FHA Loans

The FHA is actually not the lender. They insure the loans that are issued by FHA-approved lenders. FHA loans are gear more toward borrower’s with less than 20% down payment and credit issues in the past.

Qualifying for a FHA Loan Mortgage In Kentucky

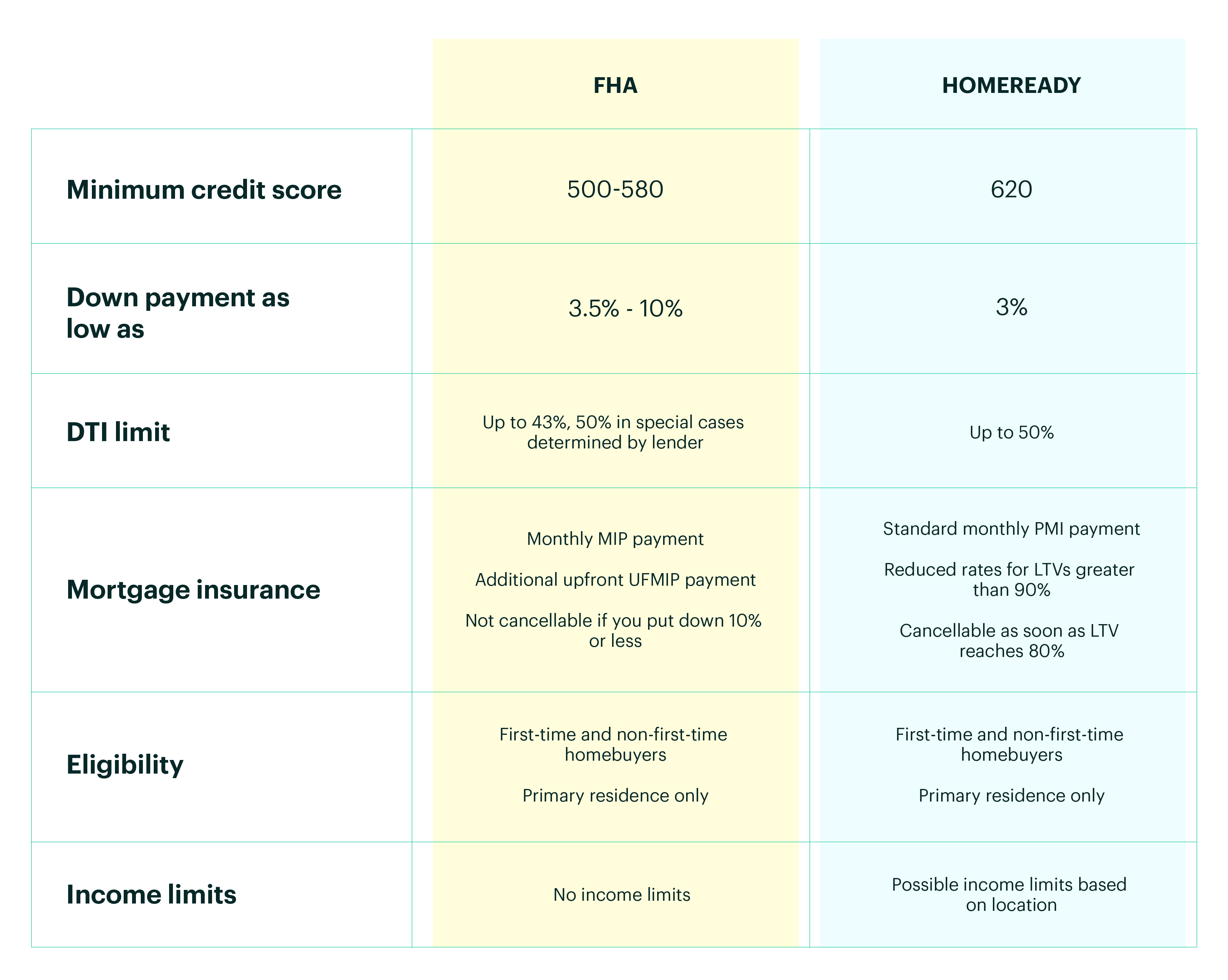

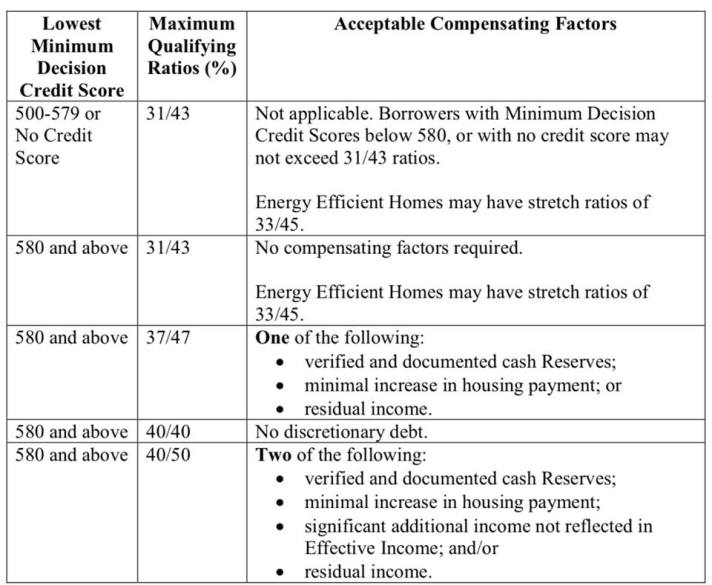

Credit Scores and Down Payment Percentages – Each year, the rules for qualifying for these loans changes. For 2020, applicants need a minimum credit score of 580 in order to get the low down payment, which is 3.5 percent.

For those whose credit score is less than 580, they will have to come up with 10 percent for their down payment. This does not guaranteed a mortgage loan approval if you have the certain credit scores, just a the minimum required.

Compensating Factors for FHA loan Approval

The credit score is just one part of the story. The FHA will also evaluate the borrower’s bankruptcies, foreclosures, prior payment history on other debts. They will also want information on difficulties that kept the borrower from making payments on other debts in the past.

Negative strikes against qualifying for the loan include not having any credit history or a bankruptcy.

Someone with a bankruptcy will have to wait for two or more years after their bankruptcy before applying for an FHA-insured loan.

If you have late payments on debt obligations, it is best to wait until you have had a full year of on-time payments before you apply for a FHA-insured loan.

If you have had a foreclosure in the past, you may still be able to get a FHA-insured loan three years after your foreclosure. The lender will be looking at the circumstances behind the foreclosure.

If you have had any civil judgement against you for money owed, collections actions or unpaid/unresolved federal debt, the FHA-approved lender will be required by the FHA to establish that all of these outstanding issues are resolved or paid before you can go through closing.

Watch out for student loans if they are delinquent because sometime this can cause a lien against you in the form of a CAVIRS Alert with HUD

As you can see, many types of borrowers who would not be eligible for a traditional mortgage, or who would face exorbitant interest rates, will be able to qualify for a FHA-insured loan at attractive interest rates.

Employment and Income for a Kentucky FHA Loan

You must have an employment history that is steady for the last two years. Does not have to be same employer.

Your income has to be verifiable in some way, whether that be through pay stubs, your income tax returns. No bank statements or cash deposits , or undocumented income can be used for income qualifying purposes.

Debt-to-Income Ratio Requirements –

Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.

Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.

If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

Property Requirements for a Kentucky FHA Loan

It must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.

It is really not too hard to pass FHA loans and the appraisal process.

Pros of FHA Loans –

-

New homebuyers and those who have lower credit scores or who have other blemishes on their credit history will often qualify for FHA-insured loans.

-

Even though these borrowers are considered “subprime” to a traditional lender, they will receive attractive interest rates through the FHA-insured mortgage programs.

-

The down payments required from borrowers are lower than those required by traditional mortgage lenders.

-

These loans can be combined with other forms of public assistance for lower income or new borrowers so that the borrower will not need to come up with a down payment of any kind.

Cons of FHA Loans –

-

Since the FHA is not actually the lender, and you have to go through FHA-approved lenders, you may not qualify due to stricter standards that the lender has for the loan.

-

Because you are not paying 20 percent as a down payment, the FHA requires two mortgage insurance premiums to be paid. One is an upfront premium that is 1.75 percent of the loan amount. Lenders often will allow you to make that mortgage insurance premium a part of your loan. The second is an annual mortgage insurance premium that is .45 percent or 1.05 percent. This premium is paid monthly.

FHA FINANCING

CREDIT REQUIREMENTS FOR KENTUCKY FHA FINANCING

What credit score do I need to qualify for a Kentucky FHA loan is one of the most common questions I hear from Kentucky homebuyers?

The short answer is you must have a minimum credit score of 500 to be eligible for an FHA loan in Kentucky. Anything lower than 500 disqualifies you from consideration for an FHA loan.

There are two sets of credit score requirements for a Kentucky FHA Loan

One important thing to understand is that the Federal Housing Administration (FHA) does not lend money directly to home buyers. You will fill out an application with a regular lender just as you would if you were applying for any other type of mortgage. What the FHA does is ensure your loan to help protect the lender in case you default.

You will be required not only to meet the FHA guidelines to qualify for a loan but also meet any additional qualifications required by the lender. This means there are two sets of requirements you have to meet with your credit score.

1. The first set of requirements comes from the Department of Housing and Urban Development (HUD). HUD oversees the FHA and determines what a borrower’s minimum eligibility requirements will be to obtain an FHA loan.

2. The second set of requirements comes from the mortgage lender. The mortgage lender has the right to add its requirements to those mandated by HUD.

What HUD requires of borrowers to be eligible for an FHA loan

The HUD Handbook 4000.1 includes the official guidelines when it comes to the FHA mortgage insurance program.

It states that in 2020 the Kentucky FHA borrowers with credit scores of 580 or higher are eligible for a 96.5% loan with 3.5% down.

Borrowers with credit scores from 500 to 579 are eligible for a 90% loan with 10% down.

Individuals with credit scores below 500 are not eligible for the FHA program.

What lenders may require of borrowers to be eligible for an Kentucky FHA loan

Lenders have the right to add requirements over and above the minimum requirements of HUD. These additional requirements are called overlays. Your lender may or may not require them.

This is not something that should come as a surprise to you, however. Requiring a credit score of 580 to 620 is not unusual. In addition to your credit score, you must have a manageable debt level that lenders are comfortable with and enough income to repay your loan.

What credit score do I need to qualify for FHA loan?

Each month Ellie Mae, the software company processing more than ⅓ of America’s mortgage loans, publishes an insight report for mortgage trends and standards. One of the things they track is average credit scores. The following is their report for November 2019 which shows what percentage of successful borrowers fall into what credit score ranges.

500 – 549 2.14%

550 – 599 5.20%

600 – 649 23.01%

650 – 699 34.74%

700 – 749 21.88%

750 – 799 10.87%

800+ 1.89%

These percentages show that the majority of borrowers who successfully qualify for FHA loans fall into the 600 to 799 range. While it is true that some successfully qualify in the low range of 500 to 599, you have a much better chance of being approved for a loan with good terms and a low down payment if you fall into the higher range.

For your free credit report and analysis call us today at 502-905-3708 or email us at kentuckyloan@gmail.com

Senior Loan Officer

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/