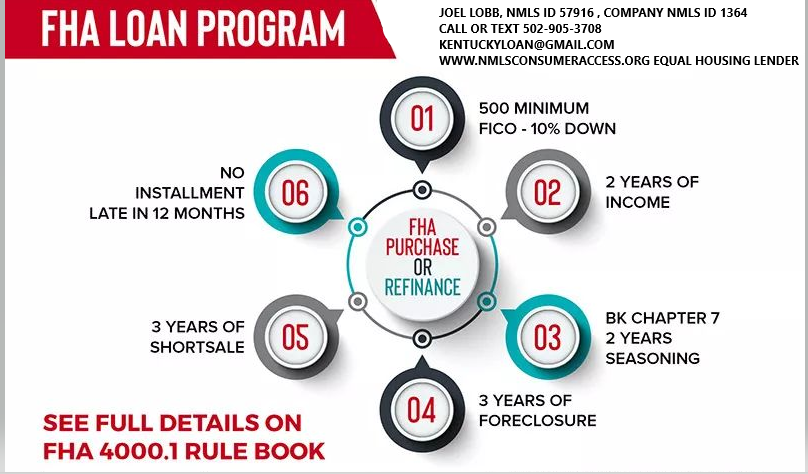

- FHA – 620+ Min Fico Approve Eligible / NO OVERLAYS-NONE!

- FHA – 620+ FICO for PURCH, RT, C/O including Flips & High Balance

- FHA – 640+ REFERS OK!—no overlays -u/w directly to 4000.1

- FHA – 640+ MANUALS up to 50% DTI (with 2 comp factors)

- FHA – 620+ No DTI CAP – Follow AUS Findings!!! (with approved eligible)

- FHA – 620+ NO Minimum Credit History or Trades with AUS Approval!

- FHA – 620+ – No VOR Unless Required by DU Findings!

- FHA – Transfer appraisals from ANY lender/AMC OK!

- FHA – ORDER YOUR APPRAISAL FROM 20+ AMCs YOU CHOOSE!

- FHA – Collections – HUD Guides Apply –

- FHA – Mortgage Lates OK if AUS Approved!!!

- FHA – ESCROW STATE – Non Purchasing Spouse derogs ignored – only affects DTI

- FHA – Borrower w/ Work Permits, Non-Resident Alien OK!

- FHA – 1 Day off Market for Cashout Refi! – Must be off market before date of loan application!

- FHA – Rental Income on 2-4 units ok FTHB

- FHA – STREAMLINE – 620 Minimum

- FHA – Streamline – 620 Score – No Appraisal, No Income, No AVM, No Credit Qualifying!!!

- FHA – Streamline -Investment and 2nd Homes OK!

- FHA – Streamline – Mtg only on subject property only!

MINIMUM CREDIT SCORES REQUIRED FOR KENTUCKY FHA, VA, USDA MORTGAGE LOANS

What is the minimum credit score I need to qualify for a Kentucky FHA, VA, USDA and KHC Conventional mortgage loan?

What is the minimum credit score I need to qualify for a Kentucky FHA, VA, USDA and KHC Conventional mortgage loan?

What is an FHA Loan and Is It Right for You?

Source: What is an FHA Loan and Is It Right for You?

What Is An FHA Loan And Is It Right For You?

Sponsored by:

The Federal Housing Administration insures what are called FHA loans. These mortgage loans provide opportunities for buyers with less-than-perfect credit or limited down payments to purchase homes, but they aren’t without potential pitfalls.

FHA loans are available to borrowers with a credit score of at least 580, and you have to make a minimum 3.5% down payment. They’re a popular option for first-time home buyers.

Lenders such as banks and credit unions issue the mortgages, which are insured by the FHA. That protects the lender if the borrower defaults, which is why the terms are more favorable than a traditional mortgage.

Around eight million single-family homes have loans insured by the FHA.

What Can an FHA Loan be Used For?

You can use an FHA loan to refinance single-family houses, to buy a single-family home, to buy some multifamily homes and condos and certain mobile and manufactured homes. There are particular types of FHA loans that can be used to renovate an existing property or for new construction.

How is an FHA Loan Different from a Conventional Mortgage Loan?

The biggest differentiator between an FHA loan and a conventional mortgage is that it’s easier to qualify for an FHA loan. You may get a loan with a lower credit score than you would otherwise, and your mortgage insurance payments may be lower too.

There are also fewer restrictions as far as using gifts from family or donations for your down payment.

If you have a FICO score of at least 580, you have to make a 3.5% down payment. With a FICO score between 500 and 579, you’re required to make a 10% down payment, and mortgage insurance is required. Your debt-to-income ratio needs to be less than 43% whereas with a conventional loan it’s usually 36%. You do need to have proof of income and steady employment, as you would need with a conventional loan.

Are There FHA Loan Limits?

There are limits on the mortgage amount you can get with an FHA-guaranteed loan. The limits vary based on your county, and in 2020 these ranged from $331,760 to $765,600. The limit amounts are updated by the FHA each year based on fluctuations in home prices.

The Benefits of the FHA Loan

The primary benefits of an FHA loan are that buyers who wouldn’t otherwise qualify may be able to own a home and for a lower down payment. Sometimes the FHA will help facilitate coverage of closing costs. If you have problems making payments on an FHA loan you may be eligible for a forbearance period if you qualify.

What Are the Downsides of an FHA Loan?

You will have to pay an upfront mortgage insurance premium with an FHA loan to protect the lender. The fee is due when you close and it’s 1.75% of your loan. You will also have to pay an annual mortgage insurance premium for the life of your loan. The amount can range between 0.45% and 1.05%.

When you buy a home with an FHA loan, it has to meet strict standards in terms of health and safety.

Also, while there are set standards from the FHA, approved lenders can create their own requirements.

Applying for an FHA Loan

You’ll have to first find an FHA-approved lender to get one of these home loans. You’ll need some documents, including proof of U.S. citizenship, legal permanent residency, or eligibility to work in America. You’ll need bank statements for at least the past 30 days, and you’ll probably need to show pay stubs.

Some of the information your lender may be able to obtain on your behalf, such as your credit reports, tax returns and employment records.

There are advantages to an FHA loan because it expands homeownership to more people than conventional loans. It’s just important that if you’re considering this loan you understand the costs and that you’re not taking on more than you’re financially prepared for because of the less stringent approval requirements.

Written by Ashley Sutphin for http://www.RealtyTimes.com Copyright © 2020 Realty Times All Rights Reserved.

Kentucky FHA Loan Requirements For 2020

Kentucky FHA Mortgage Loans Guidelines

Types of Kentucky Mortgage Loans to Consider After Bankruptcy

Types of Kentucky Mortgage Loans to Consider After Bankruptcy

If you want to try to get a Kentucky mortgage after bankruptcy, you can research a number of different types of loans. Each mortgage loan has its own unique requirements for bankruptcy filers.

Kentucky FHA Loans

Federal Housing Administration (FHA) loans are managed by the federal government and may allow you to buy a house with a down payment that’s as little as 3.5% of the purchase price. The downfall of FHA loans, however, is that you’ll have to pay for mortgage insurance, which will result in higher monthly payments.

To get a mortgage after bankruptcy using an FHA loan, you’ll have to adhere to these waiting periods:

- Chapter 7: Two years from your discharge date

- Chapter 11: No waiting period

- Chapter 13: One year from your discharge date

Kentucky USDA Loans

U.S. Department of Agriculture (USDA) loans are designed for rural borrowers who meet certain income requirements. It may be a good option if you’d like to buy a house in a rural area, have a low or modest income, and aren’t eligible for a conventional loan. If you go this route, you may not have to put any money down and you may be able to secure a low interest rate.

Keep these waiting requirements in mind if you’re interested in getting a USDA mortgage after bankruptcy:

- Chapter 7: Three years from your discharge date

- Chapter 11: No waiting period

- Chapter 13: One year from your discharge date

Kentucky VA Loans

If you’re a veteran or currently serving in the military, you may be eligible for a Department of Veterans Affairs (VA) loan. A VA loan doesn’t require a down payment or charge private mortgage insurance and can give you the chance to lock in a low interest rate. If you pursue a VA loan, however, you’ll have to pay a funding fee, which will be a percentage of your home price.

Here are the waiting requirements you should be aware of if you’d like to get a VA loan after bankruptcy:

- Chapter 7: Two years from your discharge date

- Chapter 11: No waiting period

- Chapter 13: One year from your discharge date

Kentucky Conventional Loans

Since conventional loans are not guaranteed or insured by government agencies, you can expect stricter requirements, such as having a good credit score, if you apply for one. If you get a conventional loan and put down less than 20% of the cost of your new home, you’ll need to pay private mortgage insurance.

The waiting requirements for taking out a conventional loan after bankruptcy are as follows:

- Chapter 7: Four years from your discharge date

- Chapter 11: Four years from your discharge date

- Chapter 13: Two years from your discharge date or four years from your dismissal date

Chapter 7 Bankruptcy

A four-year waiting period is required, measured from the discharge or dismissal date of the bankruptcy action until the application date.

Chapter 13 Bankruptcy

two years from the discharge date to the application date, or four years from the dismissal date to the application date.

The shorter waiting period based on the discharge date recognizes that borrowers have already met a portion of the waiting period within the time needed for the successful completion of a Chapter 13 plan and subsequent discharge.

A borrower who was unable to complete the Chapter 13 plan and received a dismissal will be held to a four-year waiting period.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted after a Chapter 13 dismissal, if extenuating circumstances can be documented. There are no exceptions permitted to the two-year waiting period after a Chapter 13 discharge.

Foreclosure / Short Sale

A seven-year waiting period is required. In all instances, the “date of foreclosure” is considered the date of the foreclosure deed. The end date of the waiting period is the application date.

Foreclosure / Short Sale – Extenuating Circumstance A three-year waiting period is permitted if extenuating circumstances can be documented. Additional requirements apply between three and seven years, which include:

FHA Loan Guidelines for Bankruptcy and Foreclosure

Chapter 7

Chapter 7 bankruptcy discharged more than 24 months prior to the application date may be allowed.

Chapter 7 bankruptcy discharged between 12 and 24 months prior to the application date requires satisfactorily established credit and documentation showing the circumstances which caused the bankruptcy were beyond the borrower’s control (i.e. unemployment, medical bills not covered by insurance). In these instances, the file must be manually downgraded to a refer and manually underwritten. It falls upon the underwriter to make a final determination as to the overall quality of the file.

Chapter 7 bankruptcy discharged less than 12 months prior to the application date is not allowed.

Chapter 13

Loans where the borrower is currently in a Chapter 13 bankruptcy or had a Chapter 13 bankruptcy which was discharged within the previous 2 years require manual downgrade and must be underwritten manually. Note that manual underwrites require Underwriting Management approval.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for FHA financing provided all of the following conditions are met in addition to standard manual underwriting requirements:

Foreclosure / Short Sale

A foreclosure less than 3 years ago is not allowed.

In all instances, the “date of foreclosure” is considered the date of the foreclosure deed. The end date of the time frame is determined by the application date.

Kentucky VA Loan Guidelines for Bankruptcy and Foreclosure

Chapter 7

Chapter 7 bankruptcy discharged more than 24 months prior to application date may be disregarded.

Chapter 7 bankruptcy discharged between 12 and 24 months prior to application date requires satisfactorily established credit and documentation showing the circumstances which caused the bankruptcy were beyond the borrower’s control (i.e. unemployment, medical bills not covered by insurance). In these instances, the file must be manually downgraded to a refer and manually underwritten. It falls upon the underwriter to make a final determination as to the overall quality of the file.

Chapter 7 bankruptcy discharged less than 12 months prior to application date is not allowed.

Note that for High Balance Transactions a minimum of 7 years must have elapsed since the discharge date regardless of AUS findings.

Chapter 13

The borrower’s credit history since the bankruptcy, the circumstances behind the bankruptcy, and the discharge date all factor in to the final determination by the underwriter.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for VA financing

Foreclosure / Short Sale

Foreclosure more than 36 months prior to application date may be disregarded.

Foreclosure less than 36 months prior to application date is not allowed.

Note that for High Balance Transactions a minimum of 7 years must have elapsed since the foreclosure date regardless of AUS findings.

In all instances, the “date of foreclosure” is considered the date of the foreclosure deed.

USDA Guidelines for Bankruptcy and Foreclosure

Chapter 7

The Discharge date and GUS findings both play an important role in determining the viability and future repayment of the new loan. As such, Chapter 7 bankruptcy seasoning is evaluated by GUS.

Chapter 13

Loans where the borrower is currently in a Chapter 13 bankruptcy or had a Chapter 13 bankruptcy which was discharged within the previous 3 years require a manual downgrade and must be underwritten manually.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for RD financing provided all of the following conditions are met in addition to standard manual underwriting requirements:

• At least 12 months of payments have been made satisfactorily

• The Trustee or bankruptcy judge’s approval to enter into the mortgage transaction is documented

• Bankruptcy payments are included in the borrower’s debt ratio

Foreclosure / Short Sale

The foreclosure date and GUS findings both play an important role in determining the viability and future repayment of the new loan. As such, foreclosure seasoning is evaluated by GUS.

A foreclosure does not automatically disqualify a borrower from RD financing. In all instances, the “date of foreclosure” is considered the date of the foreclosure deed.

You can obtain a copy of your bankruptcy paperwork from the website below:

Bankruptcy Courts http://www.pacer.psc.uscourts.gov/

Joel Lobb (NMLS#57916)

Senior Loan Office

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.Posted by Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA Email ThisBlogThis!Share to TwitterShare to FacebookShare to PinterestLabels: 100% Financing, bad credit, bankruptcy, fico scores first time home buyer, foreclosure, Kentucky First Time Home buyer zero down payment

FHA Announces COVID-19 Temporary Guidance for Kentucky FHA Mortgage Loans

Kentucky FHA Temporary Guideline Changes:

Rental Income & Self-Employment Income

FHA Announces COVID-19 Temporary Guidance for Kentucky FHA Mortgage Loans

Due to the ongoing effect of COVID-19, FHA has announced in ML 2020-03, updates to the following temporary guidelines below effective with case number assignments on or after 8/12/2020 -11/30/2020:

Rental Income for Kentucky FHA Mortgage Loans

- When qualifying utilizing rental income, for each property generating rental income the following is required:

- Reduce the effective income associated with the calculation of rental income by 25%, or

- Verify 6 months PITI reserves, or

- Verify the borrower has received the previous 2 months rental payments as evidenced by borrower’s bank statements showing the deposit. (This option is applicable only for borrowers with a history of rental income from the property).

Self Employment Income for Kentucky FHA Mortgage loans

- Self-employment income must be stable with a reasonable expectation that it will continue. Verification of the existence of the borrower’s business within 10 calendar days prior to the date of the Note to confirm that the Borrower’s business is open and operating. One (1) of the following to verify and confirm that the business is open and operating:

- Evidence of current work (executed contracts or signed invoices that indicate the business is operating on the day the lender verifies self-employment);

- Evidence of current business receipts within 10 days (Note Fairway Policy) of the note date (payment for services performed);

- Lender certification that the business is open and operating (lender confirmed through a phone call or other means) (Note Fairway Policy); or

- Business website demonstrating activity supporting current business operations (timely appointments for estimates or service can be scheduled).

Joel Lobb

Mortgage Loan Officer

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

email: kentuckyloan@gmail.com

KENTUCKY USDA RURAL HOUSING LOAN PROGRAM GUIDELINES

2020 USDA Income limits, the Jefferson County Louisville, KY

Louisville Kentucky Mortgage Loans

via KENTUCKY USDA RURAL HOUSING LOAN PROGRAM GUIDELINES

With the new changes for 2020 USDA Income limits, the Jefferson County Louisville, KY Metro area (**) saw an increase of $90,300 for a family of four and up to $119,200 for a family of five or more. The metro area surrounding counties of Jefferson County includes Oldham, Bullitt, Spencer are included in these higher income limits for USDA loans.

Remember, the entire Jefferson County and Fayette County Kentucky counties are not eligible for USDA loans. Along with parts of the following counties Daviess (Owensboro), Mccracken (Paducah), Madison County, (Richmond), Clark County (Winchester), Warren (Bowling Green), Hardin (Fort Knox and Radcliff), Bullitt(Hillview, Maryville, Zoneton, Fairdale, Brooks), Franklin, (Frankfort), Henderson (Henderson City Limits), Christian County (Hopkinsville, Fort Campbell), Boyd County (Ashland city limits) and the most Northern Parts of Boone, Kenton, Campbell Counties of Northern Kentucky (Covington, Florence, Richwood, Hebron, Ludlow, Fort Thomas…

View original post 99 more words

FHA or USDA?

FHA or USDA?

Leave a comment

I’m a first time home buyer looking to buy an owner occupied income property. I’m still in the researching options phase and have not spoken with a lender. Though, I actually have a private lender that I can use and have spoken with them but I would get cheaper interest rates with FHA or USDA so I’m looking for general advice, insight, information, knowledge or personal experience with those loans.I’m not sure what the better option would be. I can do the 3.5% down for an FHA but it would break the bank. For obvious reasons I’m not comfortable with this.

I would prefer a USDA with no money down but it seems the stipulations for income property are that you must offer low income housing. I’m not against that at all as long as the numbers work. I’m just curious how that works? How is a cap on rent set? Is it a condition for the duration of the loan or just a certain amount of years? If I refinanced down the road would it be still be a stipulation? What are the pros and cons of this stipulation?

I’m just curious what others have done if in a similar situation or what you would recommend in general in this situation.

I should add that where I’m currently renting has gone into foreclosure and at some point (this year I imagine but with the virus who knows) I will have to move so waiting to save more money isn’t something I can really do or want to. I hate to hit my savings to move to another rental and would really like to purchase an income property instead. If your advice is to wait and keep renting though then tell me.

Thank you for any words of wisdom! They are appreciated.

More real estate tips at Program Realty Wix site

I’m a first time home buyer looking to buy an owner occupied income property. I’m still in the researching options phase and have not spoken with a lender. Though, I actually have a private lender that I can use and have spoken with them but I would get cheaper interest rates with FHA or USDA so I’m looking for general advice, insight, information, knowledge or personal experience with those loans.

I’m not sure what the better option would be. I can do the 3.5% down for an FHA but it would break the bank. For obvious reasons I’m not comfortable with this.

I would prefer a USDA with no money down but it seems the stipulations for income property are that you must offer low income housing. I’m not against that at all as long as the numbers work. I’m just curious how that works? How is a cap on…

View original post 162 more words

Kentucky FHA Home loan programs for people with bad credit

Score Requirement on Kentucky FHA Loans for people with bad credit

Lowers Minimum Credit Score Requirement on Kentucky FHA Loans

Kentucky FHA Home loan programs for people with bad credit

FHA loans are designed to make housing more affordable with lower down payment requirements than conventional loans on purchases and less home equity requirements on refinances. Less stringent qualification guidelines and the security of a government-insured loan makes FHA a popular choice for consumers.

Kentucky FHA Loans with 580 Credit scores and – Low Down Payment – 3.5% which can be gifted from relatives or borrowed off one’s retirement account. If your scores is between 500-579, 10% down needed for home loan and subject to underwriting approval.

- Low down payment

- 500 minimum credit score from 10% down, to 580 above credit score with 3.5% down payment

- Can be used with Grants for Down payment through Eligible Sources

- FHA max loan – $336,750 in the State of Kentucky

- FHA approved condos eligible

- Entire Down payment can be a gift, a down payment assistance program or grant funds

- Seller can pay 6% of purchase price toward closing costs

Quick guide to checking your credit score for Kentucky FHA loans

If you’re just starting to shop for home mortgages, it pays to know if banks think you have bad credit or not. Here’s how FICO, the main credit score provider in the U.S., breaks down credit scores:

- 800-plus: Exceptional

- 740-799: Very good

- 670-739: Good

- 580-699: Fair

- 579 and lower: Poor

Kentucky FHA loans

|

Kentucky FHA Loan Details

|

|

|---|---|

|

Credit score required

|

500, but banks have minimum underwriting

standards |

|

Down payment required

|

Credit score between 500-579: 10 percent

Credit score above 580: 3.5 percent |

|

Upfront financing fee

|

1.75 percent, which can be financed

|

|

Mortgage insurance

|

0.45 to .85 percent

|

|

Mortgage limits

|

Generally, $336,766 for single-family units, but it

varies by location and you should check the limits in your area |

|

Fine print

|

Mortgage insurance premiums are paid for the life of the loan,

except when putting 10 percent or more down. If your down payment is less than 20 percent but 10 percent or more, you must have mortgage insurance for 11 years. |

Quick take

If you have bad credit, an Kentucky FHA loan offers a more accessible mortgage. While credit standards vary by lender, you may qualify for the Kentucky FHA loan with a credit score as low as 500. With a credit score above the 580 threshold, you may qualify for the 3.5 percent down payment.

Unfortunately, an Kentucky FHA loan can be expensive because of mortgage insurance fees. In addition to paying ongoing mortgage premiums for the life of the loan, you’ll have to pay a 1.75 per

Pros:

Cons:

|

What Costs to Expect When Buying a Home – Cape Gazette

Complete Guide to Closing Costs in Kentucky

A Complete Guide to Closing Costs

Louisville Kentucky Mortgage Loans

If you’re researching the finances of buying your first home, the term “closing costs” likely keeps popping up. Closing costs are the charges and fees related to buying a house in your state and county and getting a home loan. It’s a vague term, we…

Source: What Costs to Expect When Buying a Home – Cape Gazette