Buying your first house in Kentucky involves several steps, which can vary depending on the type of loan program you choose. Here’s a detailed guide on the steps and requirements for various Kentucky First Time Home Buyer loan programs:

1. Kentucky FHA Loans

Credit Score:

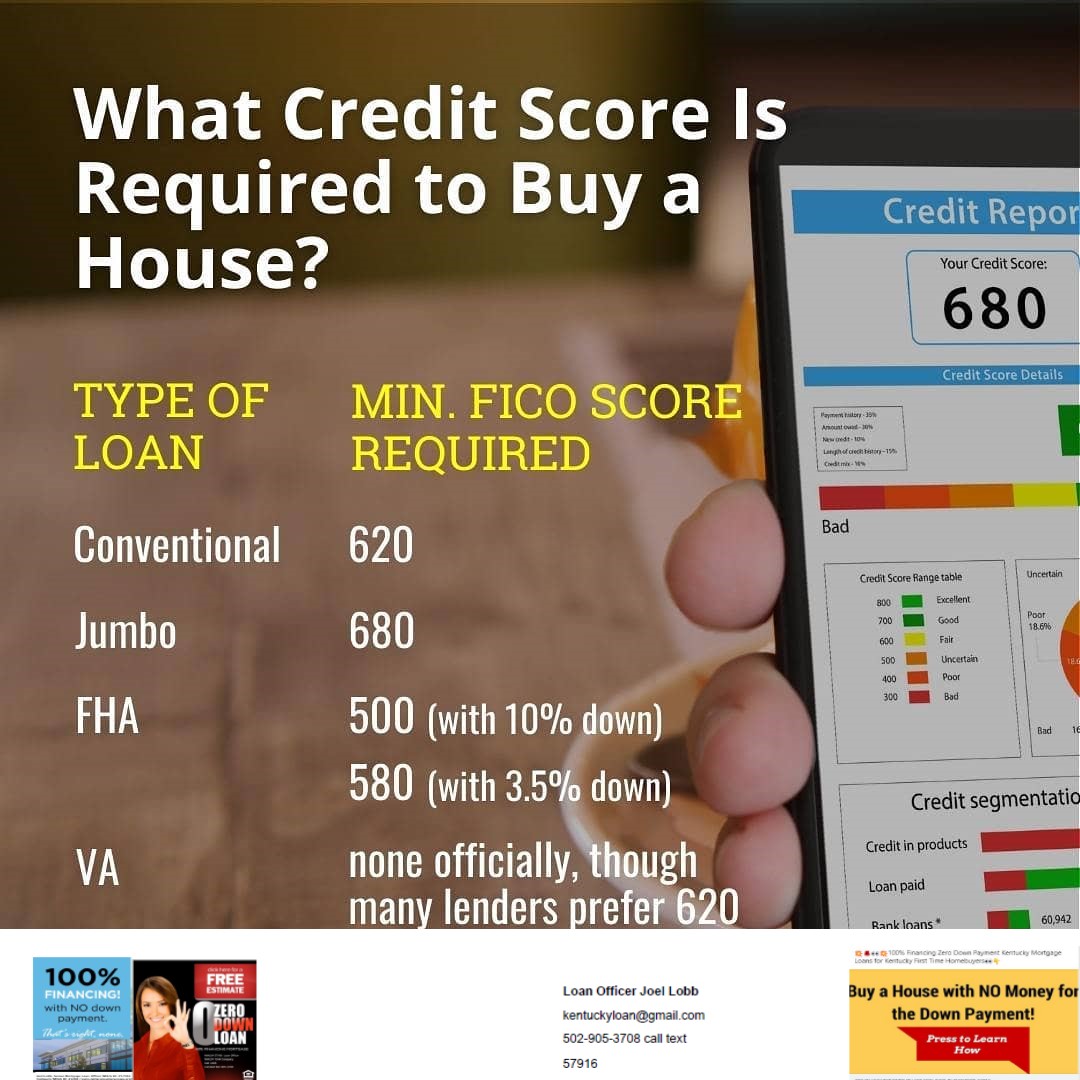

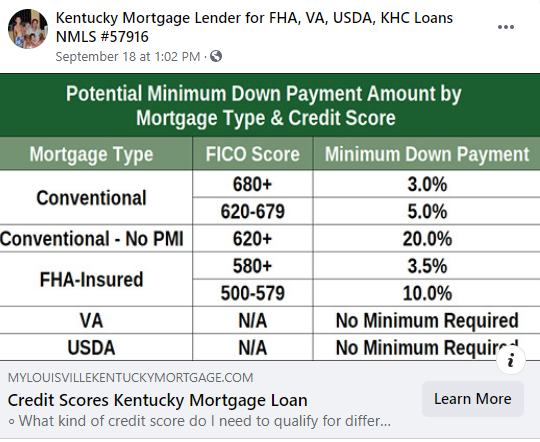

- Minimum credit score typically required is 580 for 3.5% down payment.

- Scores between 500-579 may qualify with a 10% down payment.

Income:

- Stable and sufficient income to cover the mortgage payments.

Work History:

- At least 2 years of consistent employment history.

Down Payment:

- 3.5% of the purchase price if the credit score is 580 or higher.

FICO Score:

- Minimum FICO score of 580 for maximum financing.

Bankruptcy and Foreclosure:

- Chapter 7 bankruptcy: 2 years from discharge with reestablished good credit.

- Chapter 13 bankruptcy: 1 year of the payout period with satisfactory payment history.

- Foreclosure: 3 years from completion date.

Debt Ratio:

- Typically, a maximum debt-to-income (DTI) ratio of 56.9% on backend and 45% on the front end debt ratio.

Collections:

- Must be addressed if they affect the borrower’s ability to repay the loan. Collections not required to be paid but must count in debt to income ratio sometimes if aggregate total on credit report is over $1000 total…Non-medical bills only, medical bills don’t count and usually not required to be paid or figure a payment unless you have a judgement of garnishment against your paystubs.

Mortgage Insurance:

- Required for all FHA loans. Includes an upfront mortgage insurance premium (UFMIP) and monthly mortgage insurance premiums (MIP).

Time to Close:

- Approximately 30-45 days.

Appraisal Requirements:

- Property must meet minimum property standards set by HUD.

Mortgage Documents Needed for Pre-Approval Letter in Kentucky to Buy a House using a Kentucky FHA loan:

- Proof of income (pay stubs, last two years W-2s, tax returns).

- Proof of employment. Last two years

- Proof of assets (last two bank statements). 401k or retirement account and stocks and bonds.

- Kentucky Mortgage Credit report for all three credit bureaus Experian, Equifax and Transunion

2. Kentucky USDA Rural Housing Loans

Credit Score:

- Minimum credit score of 640 is preferred for automated underwriting. No minimum score required.

- Scores below 640 may qualify with manual underwriting down to a 580 credit score

Income:

- Must meet USDA income eligibility guidelines (typically low to moderate income). 2 year history of income.

Work History:

- Stable employment history, usually for the past 2 years.

Down Payment:

- No down payment required (100% financing).

FICO Score:

- Minimum FICO score of 640 for automated underwriting. can go down to 580 possible

Bankruptcy and Foreclosure:

- Chapter 7 bankruptcy: 3 years from discharge.

- Chapter 13 bankruptcy: 1 year of the payout period with satisfactory payment history.

- Foreclosure: 3 years from completion date.

Debt Ratio:

- Typically, 33% for housing expenses and 45% for total DTI.

Collections:

- Must be resolved if they impact the ability to repay the loan. Collections typically don’t have to be paid but may have to count a payment in your debt to income ratio if aggregate is over 1k and non-medical

Mortgage Insurance:

- Annual fee and upfront guarantee fee. Currently 1% upfront and .35% month

Time to Close:

- Approximately 30-45 days, including USDA processing time.

Appraisal Requirements:

- Must meet HUD FHA standards.

Mortgage Documents Needed for Pre-Approval:

- Proof of income (pay stubs, last two years W-2s, tax returns).

- Proof of employment. Last two years

- Proof of assets (last two bank statements). 401k or retirement account and stocks and bonds.

- Kentucky Mortgage Credit report for all three credit bureaus Experian, Equifax and Transunion

3. Kentucky VA Home Loan

Credit Score:

- No minimum credit score requirement by the VA, but lenders typically require a score of 620.

Income:

- Sufficient income to cover mortgage payments and other obligations.

Work History:

- Stable employment, usually for the past 2 years.

Down Payment:

- No down payment required (100% financing).

FICO Score:

- Typically, a minimum FICO score of 620.

Bankruptcy and Foreclosure:

- Chapter 7 bankruptcy: 2 years from discharge.

- Chapter 13 bankruptcy: 1 year of the payout period with satisfactory payment history.

- Foreclosure: 2 years from completion date.

Debt Ratio:

- Typically, a maximum DTI ratio of 41%.

Collections:

- Must be resolved if they impact the ability to repay the loan.

Mortgage Insurance:

- No mortgage insurance, but a VA funding fee is required.

Time to Close:

- Approximately 30-45 days.

Appraisal Requirements:

- Property must meet VA Minimum Property Requirements (MPRs).

Mortgage Documents Needed for Pre-Approval:

Advertisement

- Certificate of Eligibility (COE).

- Credit report.

- Proof of income (pay stubs, last two years W-2s, tax returns).

- Proof of employment. Last two years

- Proof of assets (last two bank statements). 401k or retirement account and stocks and bonds.

- Kentucky Mortgage Credit report for all three credit bureaus Experian, Equifax and Transunion

4. Kentucky Down Payment Assistance Loans

Credit Score:

- Varies depending on the program; typically, a minimum of 580 for some programs and with KHC it requires a 620 score. .

Income:

- Must meet specific program income limits.

Work History:

- Stable employment history. Last two years

Down Payment:

- Assistance provided to cover down payment and closing costs. 25k welcome home grant, 10k down payment assistance loan from KHC and 5% grant used available toward closing costs and down payment

FICO Score:

- Minimum FICO score requirement varies by program.

Bankruptcy and Foreclosure:

- Varies by program.

Debt Ratio:

- Typically aligns with Kentucky FHA, VA, or USDA requirements.

Collections:

- Must be addressed if they impact the ability to repay the loan.

Mortgage Insurance:

- Depends on the primary loan program (FHA, VA, USDA).

Time to Close:

- Approximately 45-60 days.

Appraisal Requirements:

- Must meet the requirements of the primary loan program.

Mortgage Documents Needed for Pre-Approval:

- Proof of income (pay stubs, W-2s, tax returns).

- Proof of employment.

- Proof of assets (bank statements).

- Credit report.

5. 100% Financing Loans in Kentucky

Credit Score:

- Varies depending on the program; typically, a minimum of 620-640.

Income:

- Must meet specific program income limits.

Work History:

- Stable employment history.

Down Payment:

- No down payment required (100% financing).

FICO Score:

- Minimum FICO score requirement varies by program.

Bankruptcy and Foreclosure:

- Varies by program; typically 2-3 years from discharge or completion.

Debt Ratio:

- Varies by program, typically around 41-45%.

Collections:

- Must be addressed if they impact the ability to repay the loan.

Mortgage Insurance:

- Depends on the primary loan program (FHA, VA, USDA).

Time to Close:

- Approximately 30-45 days.

Appraisal Requirements:

- Must meet the requirements of the primary loan program.

Mortgage Documents Needed for Pre-Approval:

- Proof of income (pay stubs, W-2s, tax returns).

- Proof of employment.

- Proof of assets (bank statements).

- Credit report.

General Steps for Buying Your First Home in Kentucky

- Check Your Credit Score:

- Obtain a copy of your credit report and check your credit score.

- Determine Your Budget:

- Use a mortgage calculator to estimate your monthly payments and determine a comfortable budget.

- Get Pre-Approved:

- Contact a mortgage lender to get pre-approved for a loan. Provide necessary documents for income, employment, and assets.

- Choose a Real Estate Agent:

- Select a knowledgeable real estate agent to help you find a home that meets your needs and budget.

- Start House Hunting:

- Visit properties, attend open houses, and narrow down your choices.

- Make an Offer:

- Once you find a home, work with your real estate agent to make a competitive offer.

- Home Inspection:

- Hire a professional inspector to check the condition of the home.

- Finalize Your Loan:

- Work with your lender to finalize the loan application and submit all required documents.

- Appraisal:

- The lender will order an appraisal to determine the home’s value.

- Closing:

- Review and sign all closing documents. Pay any remaining closing costs and receive the keys to your new home.

Following these steps and meeting the specific requirements of your chosen loan program will help you successfully purchase your first home in Kentucky.

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574