Kentucky FHA Mortgage Loans—updated�Guidelines

via Kentucky FHA Loan Louisville Kentucky Mortgage Guidelines.

via Kentucky FHA Loan Louisville Kentucky Mortgage Guidelines.

Kentucky FHA Mortgage Loans—updated�Guidelines

via Kentucky FHA Loan Louisville Kentucky Mortgage Guidelines.

via Kentucky FHA Loan Louisville Kentucky Mortgage Guidelines.

April 2012: The New (& Expensive) FHA Mortgage Insurance Premium (MIP) Schedule.

via April 2012: The New (& Expensive) FHA Mortgage Insurance Premium (MIP) Schedule.

The FHA will raise its mortgage insurance premiums April 1, 2012. All FHA mortgage applicants — first-time buyers, repeat buyers, and users of the FHA Streamline Refinance program — will be subject to the new fees.

New FHA Mortgage Insurance Premium Schedules

The new FHA mortgage insurance premium schedule raises FHA loan costs significantly.

FHA mortgage insurance is paid in two parts.

The first part is the “Upfront Mortgage Insurance Premium”. Sometimes abbreviated as UFMIP, upfront mortgage insurance premiums will rise from 1.000% of your FHA loan size to 1.750% of your FHA loan size.

For example, if you live in Chicago, Illinois and you borrow up to the FHA’s local loan limit of $417,000, your upfront mortgage insurance premium will rise 75% from $4,170 to $7,298. This amount is added to your loan size. FHA upfront MIP is not paid via cash. You’ll pay interest on this amount for the life of your loan.

The changes in the FHA’s annual mortgage insurance premiums (MIP) are less extreme, rising only 10 basis points.

The new schedule, for loans with case numbers assigned on or after April 1, 2012:

Furthermore, all FHA mortgages made for $625,500 or more will be subject to an additional 0.25 percent annual mortgage insurance fee.

Loans made prior to April 1, 2012 will use the old FHA mortgage insurance schedule:

Special Cases: FHA Streamline Refinance MIPs

As part of the FHA’s announcement, there was also reference to the FHA’s benchmark refinance program, the FHA Streamline Refinance.

The FHA suggested that a subset of households using the streamline refi program will get access to lower mortgage insurance premiums after refinancing — not higher.

No official announcement has been made, but it’s believed that mortgage insurance premiums — both upfront and annual — will be dramatically lowered for FHA Streamline Refinances used to replace an existing FHA mortgages originated prior to June 1, 2009. New FHA Streamline Refinances that replace loans originally originated after June 1, 2009 will still pay the new, standard FHA mortgage insurance rates listed above.

The June 1, 2009 deadline should sound familiar — it’s the same deadline for Fannie Mae and Freddie Mac’s HARP 2.0 program.

The FHA is expected to confirm new FHA Streamline Refinance mortgage insurance premiums within a few weeks.

Lock Your FHA Rate Before The Price Hike

The FHA will make a formal announcement on its new FHA premiums in the coming days. Some of the exact numbers at top may change slightly. However, the FHA has confirmed the April 1, 2012 rollout date.

If you’re planning to use the FHA for your next home mortgage, get your loan application started today. If you wait, you’ll be subject to the FHA’s new premiums.

Source – Dan Green

Author’s note : This information is subject to final review by the FHA. It’s based on an initial FHA announcement made February 27, 2012. It’s unofficial until the FHA releases its mortgagee letter on the matter.

Changes to FHA Mortgage Insurance Announced.

The changes that were initially announced to be effective for cases assigned on and after April and June 1st are now effective for cases assigned on and after April 9, 2012 and on and after June 11, 2012 for loan amounts that exceed $625,500. Additional information was also added regarding reduced up-front and annual premiums for certain FHA streamline refinances and applies for cases assigned on and after June 11, 2012.

Warning to all- HUD couldn’t have made it any more confusing for us. We will all be challenged in the coming months with making sure we have communications and systems in place to assure we are using the correct MI premiums as determined by case assignment date, loan term, loan type, loan amount and LTV. Below I have attempted to lay it out in as organized a fashion as I’ve been able to determine after uncrossing my eyes which crossed while reading through the Mortgagee Letter.

Up-Front MIP Increase

• If the FHA case is assigned on and after 04/09/2012: UFMIP = 1.75% per Mortgagee Letter 2012-4

• If the FHA case is assigned 10/04/2010 – 04/08/2012: UFMIP = 1.00%

Annual MI Increases

If the FHA case is assigned on or after 04/09/2012 per Mortgagee Letter 2012-4

• > 15 yr Term: > 95% LTV = 1.25%

<=95% LTV = 1.20%

• < = 15 yr Term: > 90% LTV = .60%

>=79% LTV = .35%

• Single Family forward mortgages with amortization terms of 15 years or less, and a loan-to-value (LTV) ratio of 78 percent or less, remain exempt from the Annual MIP (see Mortgagee Letter 2011-35).

If the FHA case is assigned 04/18/2011 – 04/08/2012

• > 15 yr Term: > 95% LTV = 1.15%

<=95% LTV = 1.10%

• < = 15 yr Term: > 90% LTV = .50%

>=79% LTV = .25%

• Single Family forward mortgages with amortization terms of 15 years or less, and a loan-to-value (LTV) ratio of 78 percent or less, remain exempt from the Annual MIP (see Mortgagee Letter 2011-35).

If the FHA case is assigned on or after 06/11/2012 AND the base loan amount exceeds $625,500 Mortgagee Letter 2012-4:

• > 15 yr Term: > 95% LTV = 1.50%

<=95% LTV = 1.45%

• < = 15 yr Term: > 90% LTV = .85%

>=79% LTV = .60%

• Single Family forward mortgages with amortization terms of 15 years or less, and a loan-to-value (LTV) ratio of 78 percent or less, remain exempt from the Annual MIP (see Mortgagee Letter 2011-35).

Up-Front MIP Decreases for Certain FHA to FHA Streamline Refinances

If FHA case assignment is dated on and after 06/11/2012 and the current FHA loan being paid off was endorsed prior to 06/01/2009 per Case Query in FHA Connection, up-front MIP = .01% and annual MI = .55%.

FHA determined that these increases are necessary to encourage the return of private capital in the residential mortgage market and strengthen the Federal Housing Administration’s (FHA) Mutual Mortgage Insurance Fund. Taken together, these premium changes will enable FHA to increase revenues at a time that is critical to the ongoing stability of its Mutual Mortgage Insurance (MMI) Fund, contributing more than $1 billion to the Fund, based on current volume projections through Fiscal Year 2013. FHA estimates that the increase to the upfront premium will cost new borrowers an average of approximately $5 more per month.

Kentucky FHA loans have always been a great alternative for people who don’t quite qualify for Conventional financing. The guidelines are more forgiving allowing for smaller down payments, higher debt to income ratios, some credit issues, and more sources for the down payment.

The great thing is that the interest rate is only slightly higher than a conventional loan. Sometimes the interest rate is actually lower. Remember this! IF you go to a Kentucky Mortgage Broker or a Bank and the rate quoted is exceptionally higher, they are charging you too much. Call around for quotes. You will usually get a better rate from a Kentucky Mortgage broker.

Advantages:

Disadvantages:

Kentucky FHA Streamline loans can help homeowners lower monthly mortgage payments and interest rates. But what do you need to qualify for an FHA Streamline loan? To begin, you need an existing FHA mortgage—if you don’t have an Kentucky FHA loan but want to refinance, your options include conventional refinancing or applying for an Kentucky FHA refinancing loan.

If you have a conventional loan you wish to refinance with an FHA refinancing loan, you’ll need to apply with the usual credit check, employment verification, debt-to-income ratio requirements and other considerations. An FHA Refinancing loan can get you many of the same results—if you refinance from a conventional loan to an FHA-insured refinancing loan you may get better rates and lower payments.

For those who do have an Kentucky FHA home loan, the other requirements for FHA Streamline include:

There is another Streamline product made for those who want a refinancing plan to help them modify or improve the home. This is known as an FHA Streamline 203(k) Loan. The 203(k) is similar to ordinary Streamline loans with a few exceptions.

There are restrictions on 203(k) Streamline refinancing loans. You cannot use the 203(k) loan to do major structural repairs such as altering a load-bearing wall or work that needs architectural plans. If your home improvement work exceeds $15,000 the FHA requires you to have a third-party inspection after the job is done.

You are permitted to make two payments to each contractor. If you do the work yourself as a qualified builder, the same rule applies.

When borrowing under the FHA Streamline 203(k) program you must “close out” the loan when the work is complete. According to FHA.gov, you may be required to furnish “mortgagor’s acknowledgement of satisfactory completion…mortgagee’s inspection report(s), change orders, mortgagee accounting of the escrow funds, and record of disbursements.” It’s important to keep records of these items and more to prove the work was completed according to the agreement and in a timely manner.

A list of home inspectors in Louisville Kentucky.

Home Inspector Louisville – Independent Non-Biased Opinion

Call 502-759-6355 You are my CLIENT

Comprehensive Inpsections

Mar 21, 2011 – Kentucky Home Inspectors Association promoting the interests of Kentucky Home Inspectors and Kentucky Home Inspection Consumers.

Thorough home inspection service in Louisville, Kentucky and Southern Indiana. Click to visit or call today 502-648-9294.

|

3044 Bardstown Rd. # 226, Louisville |

Top quality home inspections in the Louisville area.

|

1234 Boyle Street, Louisville |

Mark Oerther Associates, Inc. is a home inspection service that was founded in 1992. Located in Louisville Kentucky, we provide home inspection services to …

|

2021 Tyler Lane, Louisville |

InspectHomes4U promises our INdepth knowledge, answers to your INquires and the ability to make an INformed decision. You field report is reviewed by …

|

5208 Moccasin Trail, Louisville |

Whether you are a buyer or a seller, your home is most likely your single-largest personal investment. ServiceUSA Home Inspections is ready to help …

|

3332 Willis Avenue, St. Matthews |

|

2931 Rainbow Drive, Louisville |

The purchase of a home is probably the largest single investment you will ever make. A home inspection will help you make an informed decision

|

100 Bauer Avenue, Louisville Place page More results near Louisville, KY » Rate places to improve your recommendations » |

Home inspector in Louisville KY finds electrical concern … Corroded pipe found by Louisville Kentucky home inspection …

Safe At Home Inspections, LLC is a professional property and home inspection company servicing Louisville, KY and surrounding areas. …

K & I Home Inspection Services … K&I Inspections – All Rights Reserved Louisville, Kentucky Phone: (502) 640-4005 After Hours: (800) 862-3183 …

Greg Jones Home Inspections, LLC. Services offered in the Louisville Metro area. … 7321 New LaGrange Rd Ste 113, Louisville KY 40222 · 502-429-9379 · …

Home Inspectors Directory for Louisville,Kentucky KY. Find Customer-Rated, Prescreened Home Improvement Professionals for Louisville, KY.

Skyline Inspection Services offers a full line of Home Inspection … Trimble County Kentucky, Woodford County Kentucky, Louisville, La Grange, LaGrange

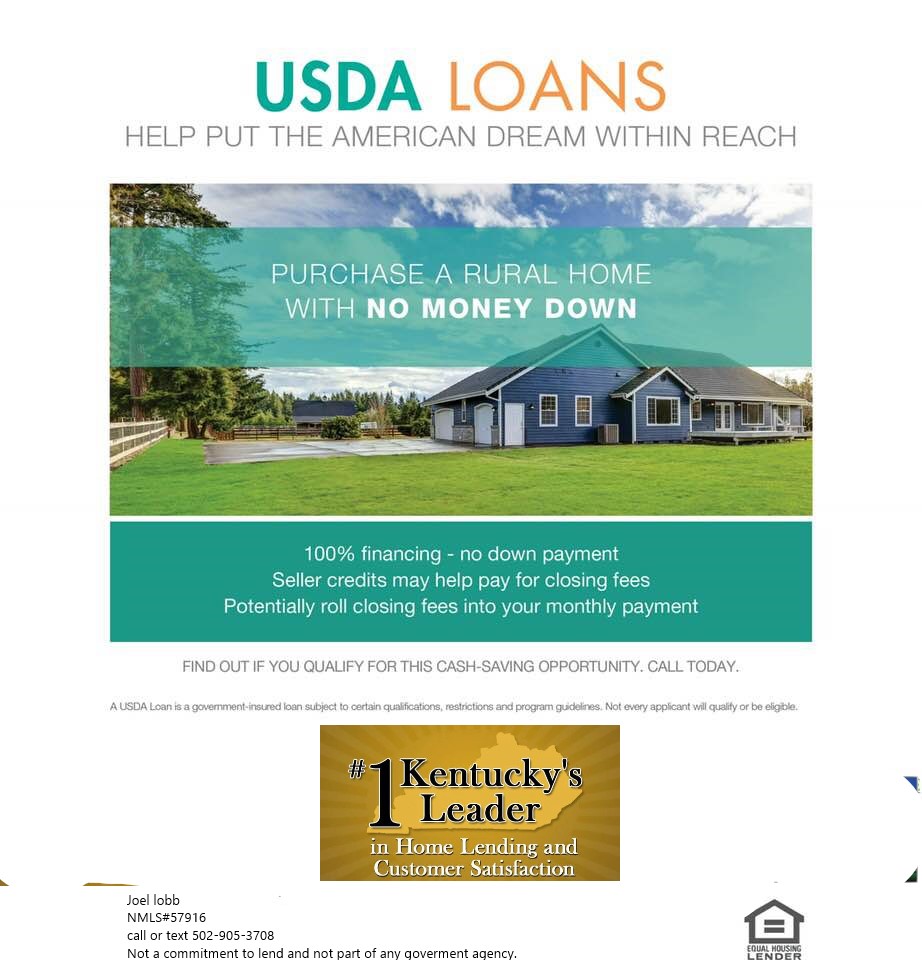

USDA Home Loans in Kentucky?

Kentucky USDA Home Loans supplies 100% financing for a home purchase, or refinancing in a USDA designated area.

Many large metropolitan cities have suburban areas that qualify for the USDA mortgage program. Click Here for an interactive map of eligible areas in Kentucky here!

The KY USDA home loans are perfect for first time buyers for many reasons. They have low interest rates, absolutely no down payment, no mortgage insurance, flexible credit guidelines, and most of the closing costs can be worked into the overall amount of the loan.

Advantages of a USDA vs. FHA & Other Loans

The USDA Home Loan program offers many advantages that traditional mortgage programs simply do not offer. First of all, all USDA home loans come with low interest rates, 100% financing, and require zero down payment. In fact, the USDA home loan program is the only home loan program in the country, besides the military, that requires absolutely no money for the purchase of a home. Instead, these funds can be used to pay to furnish the home, closing costs, make home renovations.

USDA home loans also have very flexible credit guidelines compared to most traditional lenders, with non-traditional credit histories being accepted. FHA home loans require a minimum of 3.5% down payment and have relatively high monthly mortgage insurance premiums.

Kentucky USDA Income Eligibility

Because USDA home loans are designed for moderate, to low income families, there are income limit restrictions. To be eligible for a USDA loan, your adjusted annual household income cannot exceed 115% of the median average income for that area.

This means if your total household income is above the average median income for that area, you may not be able to qualify. However, there are special deductions in place, such as childcare expenses, caring for elderly family members, or children in college, that can help to reduce your overall annual income. The borrower’s total housing and other consumer credit payments should account for no more than 4% of the total income. Income limits vary by county. Check your county Kentucky income limits here!

USDA Credit Eligibility

While it is true that USDA home loan program offers some the most credit flexible guidelines available, you still will need to have a minimum credit score of 620 to 640 to qualify.

However, some lenders may accept a credit score of as low as 580, if you can prove that some of your debts were circumstantial, temporary in nature, or beyond your control.

You must also have any bankruptcies or foreclosures discharged in the last 3 years, no outstanding tax liens and no accounts that have gone to collections within the past 12 months.

Joel LobbSenior Loan Officer(NMLS#57916) Company ID #1364 | MB73346

http://mylouisvillekentuckymortgage.com/

text or call my phone: (502) 905-3708

email me at kentuckyloan@gmail.com

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

Kentucky FHA Mortgage Insurance Premiums 2011

Kentucky FHA Mortgage Insurance Premium Amounts

EFFECTIVE FOR CASE ASSIGNMENTS DATED ON OR AFTER APRIL 18, 2011

|

|

||||||||||||||||||||||||||||||||