Kentucky FHA Streamline Refinance: Lower Your FHA Payment With Less Hassle

If you already have an FHA mortgage in Kentucky and you’re searching online for a way to lower your house payment, an FHA Streamline Refinance may be the fastest path to a lower monthly payment. In many cases it requires less documentation than a standard refinance, and it often does not require a new appraisal.

This guide breaks down how an FHA Streamline Refinance works in Kentucky, what “mortgage insurance” (MI) changes mean for your payment, how streamline differs from a regular refinance, and what the closing costs typically look like. Then you’ll see a side-by-side payment example so you can quickly estimate how much you might save.

Call or text 502-905-3708 for a free FHA refinance review (Kentucky only).

An FHA Streamline Refinance is a refinance option for homeowners who already have an FHA-insured mortgage. It’s called “streamline” because the process can be simpler than a standard refinance.

In many cases, a streamline can be used to:

Lower your interest rate and reduce your monthly principal-and-interest payment

Move from an adjustable-rate to a fixed-rate mortgage (or vice versa)

Shorten your term (for example, 30 years to 15 years) or adjust the term to fit your budget

Potentially improve long-term cost if your current FHA mortgage insurance is high

Important: FHA streamline refinances generally require a “net tangible benefit,” meaning the refinance must clearly improve your situation (most commonly a lower payment or more stable terms).

People often ask, “Is streamline the same as a normal refinance?” It’s not. Here’s the practical difference for Kentucky homeowners.

Category

FHA Streamline Refinance

Regular Refinance (full documentation)

Who it’s for

Only borrowers with an existing FHA mortgage

FHA, Conventional, VA, USDA refis (depending on eligibility)

Appraisal

Often not required (depends on lender/transaction type)

Typically required

Income/asset documentation

Often reduced compared to a full refinance (lender overlays may apply)

Full documentation is standard

Credit qualification

Can be simplified (lender overlays may require a minimum score)

Full credit underwriting is standard

Cash out

Not a cash-out program

Cash-out may be available (program rules apply)

Main goal

Lower payment and/or improve terms with fewer steps

Rate/term improvement, payoff liens, or cash-out depending on goals

If you want to pull equity out, you’re usually looking at a different product (such as an FHA cash-out refinance or another cash-out option). A streamline is built for payment improvement, not cash-out.

Closing costs for a streamline: what you’ll actually pay

Even when a streamline is “simpler,” there are still real costs. Here are the common categories you’ll see on a Loan Estimate:

Lender fees (origination/underwriting/processing, if charged)

Title work and settlement fees

Recording and state/local charges

Prepaid interest, escrow setup (taxes/insurance), if applicable

Mortgage insurance items (depending on FHA rules for your specific case)

Many homeowners search for “no-cost FHA streamline.” What that usually means is the lender credit covers some or all closing costs. It does not mean the refinance is free. A lender credit typically comes with a slightly higher rate. The right choice depends on your break-even timeline and how long you plan to keep the home.

CTA: Call or text 502-905-3708 and I’ll run both options side-by-side: (1) lowest rate, (2) lowest out-of-pocket.

Payment example chart: interest rate vs mortgage insurance

Most borrowers focus only on interest rate. With FHA loans, mortgage insurance can also be a meaningful part of the monthly payment. Below is a simple example to help you compare.

Example assumptions (for illustration only):

Base loan amount: $200,000

30-year term

Principal and interest only (taxes and insurance not included)

Mortgage insurance shown as an estimated monthly MI amount

Scenario

Interest rate

Estimated monthly P&I

Estimated monthly FHA MI

Estimated total (P&I + MI)

Estimated monthly savings

Current FHA loan (example)

7.00%

$1,330

$170

$1,500

—

Streamline refinance (example)

5.75%

$1,168

$135

$1,303

$197

How to read this:

The rate reduction lowers principal and interest.

Mortgage insurance may also change based on FHA rules for your specific FHA case number/endorsement date and the new loan structure.

Your real payment change depends on your current balance, remaining term, current MI factor, escrow, and pricing on the day you lock.

If you want, I can run your exact numbers and provide a clear “before vs after” worksheet.

How to apply for an FHA Streamline Refinance in Kentucky

Here’s the clean step-by-step path I use with Kentucky FHA homeowners:

Quick review call (10 minutes): current FHA loan, payment, goals, occupancy, and timeframe.

Case-specific eligibility check: confirm streamline eligibility and net tangible benefit.

Pricing options: compare “lowest rate” vs “lender credit/no out-of-pocket” options.

Disclosures and documentation: provide whatever your lender’s overlay requires (often reduced vs full refi).

Title work and closing: finalize closing costs, escrows, and signing.

Primary CTA:

Call or text 502-905-3708 for a free Kentucky FHA Streamline Refinance review. You’ll get a clear estimate of payment savings, costs, and break-even timeline.

External links for topical authority (add as needed):

Will an FHA streamline refinance require an appraisal in Kentucky?

Often, no. Many streamline refinances are completed without a new appraisal, but lender overlays and transaction specifics can change the requirements.

Can I do an FHA Streamline if my home value is down?

Possibly. Since many streamlines do not require a new appraisal, value changes may not prevent approval. The final answer depends on the lender’s overlay and the exact streamline type.

Can I roll closing costs into the loan?

In many refinance structures, some costs may be financed or offset with lender credit. The right approach depends on your break-even timeline and monthly savings.

Is a streamline always the best refinance choice?

No. If you need cash-out, want to remove mortgage insurance via a different program, or need to restructure debt, a full refinance may be a better fit. The correct recommendation comes from a side-by-side comparison.

Free Kentucky FHA refinance review

Joel Lobb Mortgage Broker NMLS #57916 Licensed in Kentucky only Company NMLS #1738461 Call or text: 502-905-3708 www.nmlsconsumeraccess.org

Not a commitment to lend. All loans subject to credit approval and underwriting. Program guidelines and lender overlays can change without notice. Not affiliated with any government agency, including FHA.

This type of loan is administered by KHC in the state of Kentucky. They typically have $12,500 down payment assistance year around, that is in the form of a second mortgage that you pay back over 15 years at a interest rate of 4.75% depending on your income in the household.

Joel has worked with KHC for 12 of his 20 years in the mortgage lending business. Joel said, “A lot of my clients would not have been able to purchase a home of their own or possibly delayed their purchase due to lack of down payment but with the $6,000 DAP loan program, this gets them into a house sooner and starts their path to homeownership while building equity instead of throwing their money away.”

<!– WordPress.com-friendly page content (no , no , no ) –>

Kentucky FHA Loans (2026): Requirements, Down Payment, Credit Scores, and How to Get Approved

If you are buying a home in Kentucky and want a low down payment option with more flexible credit guidelines,

an FHA loan is often the most practical path. This guide covers the FHA rules that matter in 2026, the common

underwriting issues that slow people down, and the fastest way to get a clean pre-approval.

Minimum down payment: 3.5% with 580+ credit score; 10% with 500–579 (case-by-case).

Primary residence only (no investment property).

FHA appraisal required and the home must meet FHA property standards.

Seller concessions allowed up to 6% of the sales price toward certain closing costs and fees.

Mortgage insurance is required (upfront + monthly/annual).

Want me to price your payment and cash-to-close fast? Text “FHA” to

502-905-3708

and I will reply with a document checklist.

Credit Score Guidelines for Kentucky FHA Loans

FHA guidelines allow:

580+ credit score: eligible for the 3.5% minimum down payment option.

500–579 credit score: may be eligible with 10% down (approval depends on the full file).

Below 500: generally not eligible for FHA financing.

Important: lenders can add “overlays” (stricter requirements than FHA). That is why two lenders can give two

different answers on the same borrower. If you want a straight answer, I will review your scenario and tell you

what is realistically approvable.

Down Payment and Closing Costs (What Kentucky Buyers Actually Pay)

FHA requires a minimum down payment based on credit score. Closing costs are separate and typically include lender

fees, title, escrow, and prepaid items like taxes and homeowners insurance.

3 ways Kentucky FHA buyers reduce cash-to-close

Seller concessions (up to 6% of the sales price, when allowed and properly structured).

KHC Down Payment Assistance (for eligible borrowers using a KHC first mortgage).

Lender credits (higher rate trade-off to reduce upfront costs, when it makes sense).

FHA loan limits change by county and are updated periodically. The cleanest way to avoid outdated numbers is to

pull your county limit directly from HUD.

If you text me your county (or the property address), I will confirm the current FHA limit and your max purchase price:

502-905-3708.

Debt-to-Income Ratio (DTI): What FHA Looks At

FHA underwriting looks at housing expense compared to income and total monthly debts compared to income.

A common baseline guideline you will see referenced is 31% for housing and 43% for total debt, with exceptions

possible depending on automated underwriting results and compensating factors.

Housing ratio (front-end): proposed house payment compared to gross monthly income.

Total DTI (back-end): house payment plus monthly debts compared to gross monthly income.

If your DTI is tight, the fix is usually one of these: adjust purchase price, restructure debt, improve credit,

or document additional qualifying income correctly.

Types of FHA Loans Kentucky Buyers Use Most

FHA 203(b) Standard Purchase

The most common FHA loan for buying a primary residence in Kentucky.

FHA 203(k) Renovation Loan

Combines purchase plus renovation costs into one loan for qualifying homes that need repairs or updates.

FHA Streamline Refinance

For existing FHA borrowers looking to reduce payment with simplified documentation (when eligible).

FHA Cash-Out Refinance

For homeowners who want to access equity (subject to FHA rules and underwriting).

Kentucky Housing Corporation (KHC) offers down payment assistance for eligible borrowers using a KHC first mortgage.

KHC’s Regular DAP has been listed as assistance up to $12,500, repayable over 15 years at 4.75% (subject to program

terms, eligibility, and availability). Confirm current options here:

KHC Down Payment Assistance.

If you want a straight answer on eligibility (income limits, purchase price limits, and which first mortgage fits),

call or text me:

502-905-3708.

How to Apply for an FHA Loan in Kentucky (Simple Process)

Quick consult (10 minutes): goals, county, price range, and down payment plan.

Document review: paystubs, W-2s, bank statements, and ID.

Run automated underwriting and issue a clean pre-approval.

Kentucky offers several grant programs to help residents achieve their dream of homeownership. These programs provide financial assistance to eligible buyers, making the purchase of a home more affordable. Here’s an overview of the current grant options available to Kentucky homebuyers:

1. Kentucky Housing Corporation (KHC) Down Payment Assistance Program

The KHC offers up to $12,500 in down payment assistance to eligible first-time homebuyers. This program can be used in conjunction with KHC’s first mortgage loans.

Eligibility:

Must be a first-time homebuyer or not have owned a home in the past three years

Meet income and purchase price limits, which vary by county

Complete a homebuyer education course

2. Kentucky Affordable Housing Trust Fund

This program provides funds to create or preserve affordable housing for low-income households. While not a direct grant to homebuyers, it can help create affordable housing opportunities.

3. USDA Rural Development Grant

Although not specific to Kentucky, this federal program is available in many rural areas of the state.

Key features:

Provides loans and grants for low-income individuals in rural areas

Can be used for home purchases or repairs

Income limits and location restrictions apply

4. Louisville Metro Down Payment Assistance Program

Specific to Louisville, this program offers forgivable loans of up to $25,000 to help with down payment and closing costs.

Eligibility:

Must be a first-time homebuyer

Income must be at or below 80% of the area median income

Property must be located within Louisville Metro

5. Lexington Homeownership Assistance Program

This program, specific to Lexington, provides up to $15,000 in down payment and closing cost assistance.

Eligibility:

Must be a first-time homebuyer

Income must be at or below 80% of the area median income

Property must be located within Lexington-Fayette Urban County

6. Individual Development Account (IDA) Program

While not exclusive to homebuying, this program can help prospective homeowners save for a down payment.

Key features:

Provides matching funds for savings (typically $2 for every $1 saved)

Can be used for homeownership, education, or starting a small business

Income and asset limits apply

7. Welcome Home Grant

Feature

Welcome Home Grant

KHC DPA

Type

Grant (no repayment if retained)

Repayable loan (second mortgage)

Amount Typical

Up to ~$20,000*

Up to $12,500

Payback

None if stays 5+ years*

Monthly payments over 15 yrs

Retention/Terms

5-year deed restriction

Standard mortgage second lien

Income Limits

≤80% MRB household

MRB or Secondary Market

Qualifying Income

Household inclusive

Dependent on mortgage product underwriter

First-Time Buyer

Optional

Depends on mortgage product

Access

Through FHLB member lenders

Through KHC-approved lenders

Availability

Seasonal, limited

Ongoing

How to Apply

To apply for these grants, contact the respective program administrators:

For city-specific programs: Contact your local housing authority or visit the city’s official website

Welcome Home Grant

Program is administered through participating FHLB Cincinnati member lenders (banks and credit unions that belong to the FHLB system).

Buyers must contact a participating mortgage lender early and reserve funds once the program opens (often first-come, first-served).

A fully executed purchase contract and signed mortgage application are typically required to reserve funds.

KHC DPA

Must work with a KHC-approved lender; you cannot apply directly to KHC.

The KHC-approved lender will bundle the first mortgage and the DPA second mortgage into one closing transaction.

Implication:

Both programs require lender participation. The Welcome Home Grant is tied to a different funding source (FHLB) than KHC’s internal DPA loan.

Remember that grant availability and terms may change, so it’s essential to check with the program administrators for the most up-to-date information. Additionally, many of these programs require participants to complete homebuyer education courses. These courses can provide valuable information about the homebuying process.

By taking advantage of these grant programs, Kentucky residents can make their dream of homeownership more attainable. Be sure to explore all options and consult with housing counselors or financial advisors to determine the best path to homeownership for your specific situation.

The mortgage process can often be a confusing one — whether you’ve bought a home before or not. There’s a lot of prep work and moving parts, and most of the terminology is unfamiliar to the average consumer.

Fortunately, that last part is an easy fix.

Are you getting ready to buy a home or refinance your current mortgage? Take a look at some of the lesser-known terms you might want to know.

Annual Percentage Rate (APR): This number reflects the total annual cost of taking out your mortgage loan. It’s different from your mortgage interest rate and includes some extra fees.

Underwriting: When a loan professional evaluates your application and verifies all your financial details, that’s underwriting. It’s important to ensure that you have the means to manage your new monthly payment.

Escrow: An escrow account is used to hold funds prior to closing, including your earnest money deposit. You might also pay into an escrow account to cover property taxes, homeowners insurance and private mortgage insurance (if you have it).

Closing Disclosure: This is a document that you’ll be given at least three days before your closing date. It should detail all the final costs of your loan, as well as what you’ll be expected to pay on closing day.

Mortgage Note: You’ll sign this document at closing.It outlines the terms of your home loan and includes how much you’re borrowing, whether it’s a fixed-rate or adjustable-rate mortgage and more.

Prepaid Costs: These also come up at closing and will go into your escrow account. They usually cover mortgage interest, property taxes and homeowners insurance expenses that occur between your closing date and the date your first mortgage payment is due.

If you need help understanding any part of the mortgage process, get in touch today.

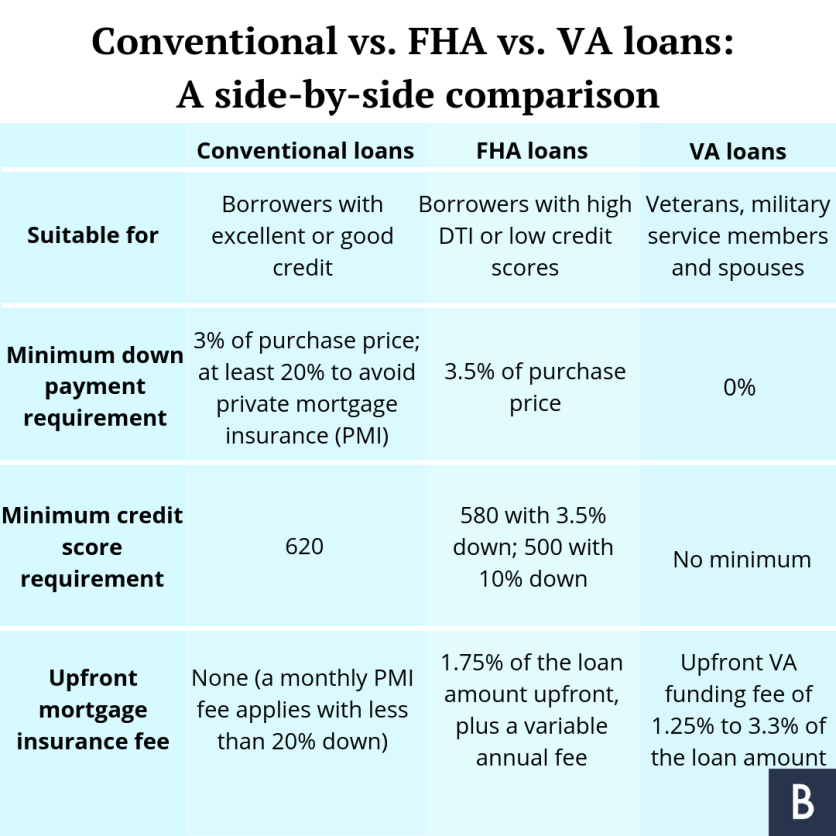

FHA vs. Conventional Loans: Which Is Better for Kentucky Homebuyers?

Compare FHA and conventional loans for Kentucky homebuyers. Learn credit requirements, down payments, mortgage insurance, and which loan fits your situation.

When comparing FHA loans vs conventional loans in Kentucky, the decision comes down to four core factors: credit score, down payment, debt-to-income ratio, and mortgage insurance. Both loan programs are widely used across Louisville, Lexington, Northern Kentucky, and rural areas, but they serve very different borrower profiles.

FHA Loans: Built for Flexibility

Kentucky FHA loans are designed for buyers who need more flexibility. FHA financing is often a strong option for borrowers with credit scores under 680, limited savings, or little to no cash reserves after closing. FHA also allows buyers to qualify sooner after major credit events, including foreclosures that are three to seven years old and short sales that occurred two to four years ago.

Another major advantage of FHA loans in Kentucky is gifting. The entire down payment and most closing costs can be covered with gift funds from approved sources. This makes FHA especially popular with first-time homebuyers and buyers using down payment assistance programs.

FHA Mortgage Insurance (MIP) Breakdown:

Upfront mortgage insurance premium: 1.75% of loan amount (rolled into the loan)

30-year loans with less than 5% down: 0.85% annually

30-year loans with 5%+ down: 0.80% annually

15-year loans: 0.45% to 0.70% annually (depending on down payment)

Conventional Loans: For Stronger Credit

Kentucky conventional loans are best suited for borrowers with stronger credit and more money saved. Conventional financing generally favors buyers with credit scores above 680, at least five percent down, and reserves remaining after closing. Borrowers with foreclosures over seven years old or short sales that occurred five to seven years ago typically fit conventional guidelines more easily.

One of the biggest advantages of conventional loans is mortgage insurance flexibility. Unlike FHA, there is no upfront mortgage insurance premium. Monthly private mortgage insurance can be lower for borrowers with strong credit, and PMI automatically drops off once the loan reaches roughly 80 percent loan-to-value. FHA mortgage insurance, by contrast, usually lasts for the life of the loan when the down payment is less than ten percent.

Quick Comparison Table

Factor

FHA Loans

Conventional Loans

Credit Score Required

580+ 3.5% down payment (some lenders 500+ 10% down payment)

720+ typically

Down Payment

3.5% (with 580+ score)

3-5% minimum, typically 5%

Mortgage Insurance

Required on all loans (lifetime with <10% down)

Only if less than 20% down; drops at 80% LTV

Upfront Insurance Premium

1.75%

None

Gift Funds

100% of down payment allowed

Limited or restricted

Max Debt-to-Income

Up to 56.99% (with compensating factors)

Typically 45%

Property Types

Owner-occupied only

Owner-occupied and investment

Appraisal Standards

Stricter

More flexible

The Bottom Line

FHA loans are ideal for Kentucky buyers rebuilding credit, using gift funds, or purchasing with limited savings. Conventional loans reward borrowers with stronger credit, larger down payments, and long-term equity goals.

Most homeowners do not keep a mortgage for 30 years. Because many refinance or sell within five to seven years, FHA’s lifetime mortgage insurance is often less of a concern than it appears on paper. In many cases, the lower interest rate and easier approval standards outweigh the insurance cost.

Joel Lobb

Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae

EVO Mortgage • Helping Kentucky Homebuyers Since 2001

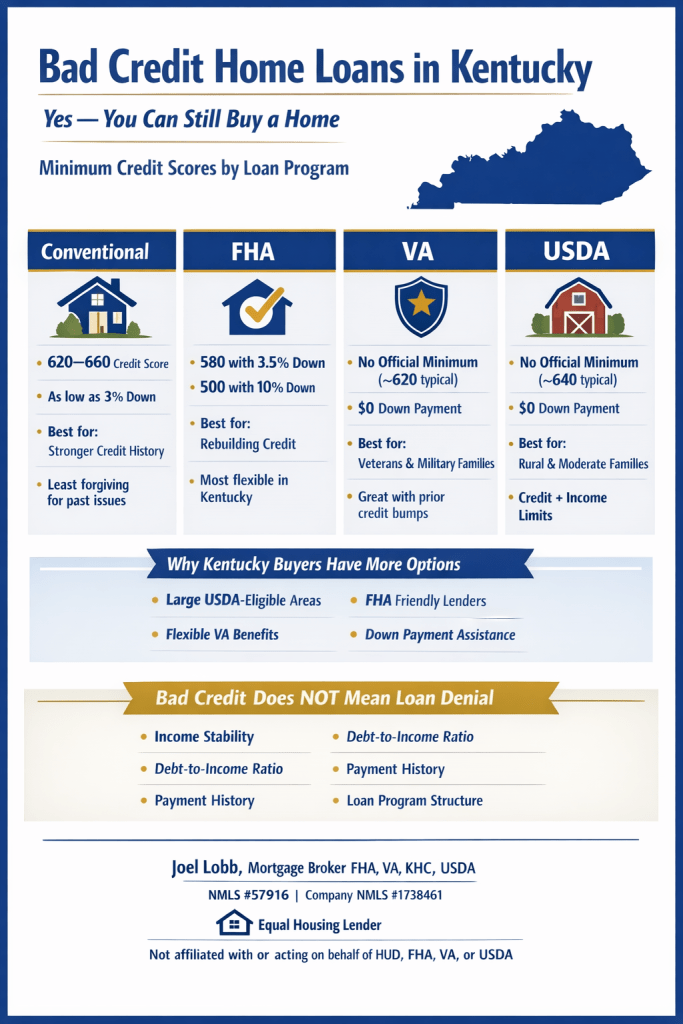

Many Kentucky homebuyers assume a low credit score automatically disqualifies them from buying a home.

That assumption is incorrect. Several mortgage programs are specifically designed to help buyers with past credit issues qualify for financing sooner than expected.

In Kentucky, the most common loan options for buyers with bad or fair credit include FHA, VA, USDA,

and select conventional loan programs. Each option has different credit score thresholds, down payment requirements,

and underwriting flexibility.

Minimum Credit Score Requirements by Loan Type

Conventional loans typically require a minimum credit score between 620 and 660, depending on the program and automated underwriting results.

While down payments can be as low as 3 percent, conventional loans are generally the least forgiving when it comes to recent late payments, collections, or limited credit history.

FHA loans in Kentucky are the most common solution for buyers rebuilding credit.

FHA financing allows approvals with credit scores as low as 580 with only 3.5 percent down.

In limited cases, buyers with scores down to 500 may qualify with a 10 percent down payment, provided the overall risk profile is strong.

Eligible service members and veterans may benefit from

VA loans in Kentucky, which do not have an official minimum credit score requirement set by the agency.

Most lenders look for scores around 620, but VA loans remain one of the most flexible options available, offering zero down payment and no monthly mortgage insurance.

For buyers purchasing outside major metro areas,

USDA loans in Kentucky can provide 100 percent financing with competitive interest rates.

While there is no official minimum credit score, most USDA lenders require a 640 score for automated approval, along with meeting income and household eligibility guidelines.

Why Kentucky Buyers Often Qualify With Lower Credit Scores

Large portions of Kentucky qualify for USDA rural housing loans

FHA loans are widely accepted by Kentucky lenders

VA loans provide exceptional flexibility for eligible veterans

Down payment assistance programs can be layered correctly with the right loan structure

What Mortgage Underwriters Actually Review

Mortgage approval is based on the full financial picture, not just the credit score. Underwriters evaluate income stability,

work history, debt-to-income ratio, recent payment behavior, available assets, and how the loan is structured.

In many cases, a borrower with a lower credit score but strong income stability and clean recent payment history

can be a stronger approval than someone with a higher score and excessive debt.

Bottom Line for Kentucky Homebuyers

Bad credit does not automatically mean loan denial. The right loan program, structured correctly from the start,

often matters more than the credit score alone. Many Kentucky buyers qualify months or even years sooner than they expect

once their options are reviewed properly.

NMLS #57916 | Company NMLS #1738461

Equal Housing Lender.

This is not a commitment to lend. All loans are subject to credit approval and program requirements.

Kentucky FHA Loans: New Guidelines for Collections & Disputes 2026

Kentucky FHA Loans: New 2026 Guidelines

Collections, Disputes & Judgements Explained

If you’re a Kentucky first-time homebuyer with collections, disputes, or judgements on your credit report, you’re not alone—and you’re not disqualified from homeownership. The Federal Housing Administration (FHA) recently updated its lending guidelines to provide more flexibility and clarity around credit challenges.

Whether you’ve faced financial hardship, billing disputes, or collection accounts, understanding these new FHA rules could be the key to securing your Kentucky mortgage.

📋 Effective Date: All loans with case numbers assigned on or after September 9th, 2026

Understanding FHA Loans with Bad Credit, Disputes & Collections

What Are Disputed Accounts on Your Credit Report?

A disputed account appears on your credit report when you’ve officially challenged information you believe is inaccurate or incorrect. Many Kentucky borrowers don’t realize that disputed accounts can affect their ability to qualify for an FHA loan. The good news? FHA has clarified how these accounts will be evaluated going forward.

Collection Accounts & FHA Loan Qualification

Collection accounts are one of the biggest obstacles for Kentucky first-time homebuyers trying to get approved. Under the new 2026 FHA guidelines, the agency has provided specific underwriting rules that actually offer more opportunity than you might think.

Judgements on Credit Reports

If you have judgements on your credit report, FHA underwriters will evaluate them carefully, but they don’t automatically disqualify you. The new guidelines provide specific direction on how these accounts are assessed during the mortgage approval process.

New FHA Guidelines for Collections, Judgements & Disputes

Collection Account Rules: The $2,000 Threshold

Here’s how FHA Fannie Mae’s DU (Desktop Underwriter) system now handles collection accounts:

If your collection accounts total $2,000 or more cumulatively:

Pay in Full — The collection debt(s) must be paid in full prior to or at closing, OR

Payment Plan — You can establish a payment arrangement with the creditor, and the monthly payment is included in your debt-to-income ratio, OR

5% Payment Calculation — Include a monthly payment of 5% of the outstanding balances of each collection account in your debt-to-income ratio

If your collection accounts total less than $2,000: These may be treated more favorably during underwriting, though FHA DU will still require verification.

💡 Important for Kentucky Borrowers: If you’re married and in a community property state, collection accounts from your spouse are also counted toward this threshold—even if they’re a non-borrowing spouse.

Manual Underwriting Triggers

Certain credit situations require manual underwriting instead of automated approval. Your Kentucky FHA application will likely be manually reviewed if:

$1,000 or more in disputed derogatory credit accounts appears on your credit report

20% or greater decline in self-employed income

Mortgage lates within the last 12 months

While manual underwriting takes longer, it doesn’t mean you’ll be denied. Many Kentucky borrowers with credit challenges are successfully approved through manual underwriting because a trained loan officer can explain your circumstances and compensating factors.

Payment History Requirements for FHA Approval

FHA has strict (but achievable) payment history standards:

All mortgage and installment loan payments must be on time within the last 12 months

No more than two 30-day late payments within the last 24 months

No derogatory credit on revolving accounts (credit cards, lines of credit) in the last 12 months

Collection accounts must be addressed per the guidelines above

Additional 2026 FHA Updates

New Well Water Testing Requirements

If you’re purchasing a Kentucky home with a private well, be aware of updated FHA requirements for well water testing:

Well water tests must now be:

Performed by a disinterested third party (not you, the seller, or anyone with a financial interest in the transaction)

Conducted using a method acceptable to your local health authority

Documented before approval

Well water testing is now required for:

Newly constructed properties and/or new wells

Properties with deficiencies in the well or water quality identified by an appraiser

Areas where water safety issues have been reported or are known

Properties near dumps, landfills, industrial sites, farms, or hazardous waste areas

Properties where the well and septic system are less than 100 feet apart

Overtime, Bonus & Tip Income: Simplified Calculations

Good news for Kentucky borrowers with variable income: FHA has clarified how overtime, bonuses, and tips are calculated for loan qualification.

Your overtime, bonus, or tip income will be calculated as the LESSER of:

Average income earned over the previous 2 years (or the total time if earned less than 2 years), OR

Average income earned over the previous year

Commission & Business Expense Requirements Removed

FHA has completely eliminated previous requirements regarding unreimbursed business expenses and commission income or automobile allowances. This aligns FHA guidelines with current IRS tax law, making it easier for self-employed borrowers and those with commission-based income to qualify.

Interested Party Contribution (IPC) Limits

Under the 2026 guidelines, mortgagees and third-party originators are now explicitly included in IPC limits. This means:

Lenders cannot contribute toward your down payment to artificially lower your upfront costs

Exception: Premium pricing credits don’t count against IPC limits—unless the lender is also acting as the seller, agent, builder, or developer

DTI Requirements & Qualification

31% Front-End / 43% Back-End FHA

31% of your gross monthly income can go toward housing costs. 43% of your gross monthly income can go toward all monthly debts.

No compensating factors required to meet these ratios, making FHA one of the most accessible loan programs for Kentucky borrowers.

Documentation You’ll Need for Underwriting

If your Kentucky FHA application requires manual underwriting due to credit challenges, be prepared to provide:

Employment & Income Documentation

Verbal Verification of Employment (VOE)

Paystubs covering the most recent 30-day period

W2s for the past 2 years

2-year employment history

Housing & Credit History

Verification of Rent (VOR) or 12 months of cancelled checks if credit report doesn’t show last 12 months of housing payment history

Letter of Explanation (LOX) for any derogatory credit or late payments within the last 24 months

Cash Reserves

At least 1 month in reserves from your own funds (cannot be a gift)

3 months required if purchasing a 3-4 unit property

Ready to Get Approved for a Kentucky FHA Loan?

With over 20 years of experience helping Kentucky families overcome credit challenges to achieve homeownership, I specialize in FHA loans for borrowers with collections, disputes, judgements, late payments, and more.

I offer free FHA mortgage applications with same-day approvals. Let’s discuss your options today.

About Joel Lobb – Kentucky Mortgage Loan Officer

With over 20 years of mortgage industry experience, I’ve helped more than 1,300 Kentucky families secure homeownership through FHA, VA, USDA, KHC, and Fannie Mae programs.

Your Guide to Disputed Accounts & Collections 2026

💰

Collection Accounts: The $2,000 Threshold

Step 1: Check Total

Add up all collection accounts on your credit report

Step 2: Compare

$2,000?

Is your total more or less?

Step 3: Choose Path

Select your payment strategy

1

Pay in Full

Pay before or at closing

2

Payment Plan

Monthly payment included in DTI

3

5% Calculation

5% of balance added to DTI

❓

Disputed Accounts

What Triggers Manual Underwriting?

If you have $1,000 or more in disputed derogatory accounts, your application will be reviewed by a human underwriter instead of automated approval. This isn’t bad news—it means your circumstances can be explained!

The Best Kentucky Mortgage Loan Options When Looking for your first house in Kentucky Kentucky First-time Home Buyer Programs👀💯👇‼

Kentucky Mortgage Requirements for FHA, VA, USDA and Fannie Mae

FHA loan in Kentucky you will be confronted with minimum credit score requirements set forth by FHA and the lender. Even though FHA will insure the mortgage loan at a certain credit score, you will see that lenders will create “credit-overlays” to protect their risk and ask for a higher credit score.

So keep in mind when you are getting an FHA lenders will have higher credit score minimums in addition to the FHA Mortgage Insurance program.

For a Kentucky Homebuyer wanting to purchase a home or refinance their existing FHA loan, FHA requires a 3.5% down payment and the borrower must have a 580 FICO Credit Score. If the score is below 580, then you would need 10% down and still qualify on a manual underwrite.

You must have a FICO score of at least 500 to be eligible for a Kentucky FHA loan. If your FICO score is from 500 to 579, your down payment on the loan is 10 percent of the loan.

If your FICO score is 580 or higher, your down payment is only 3.5 percent. If your credit score is less than 580, it may be more cost-effective to take the necessary steps to improve your score before taking out the loan, rather than putting the money into a larger down payment.

How do they get the credit score: There are three main credit bureaus in the US. Equifax, Experian, and Transunion. The three scores vary but should be relatively close as long as the same creditors are reporting to the same bureaus.

You will get a variation in the scores due to all creditors or collection companies don’t report to all three bureaus. This is why they take the mid score. So if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying credit score would be 620

Based on my experience with lenders that I deal with in Kentucky on FHA loans, most lenders require 620 middle credit score for consideration for loan approval.

How do they get the score: They take the mid score, so if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying score would be 620.

If your score is below 620, a manual underwrite is where the AUS (Automated Underwriting System) refers your loan to a human being, and they look at the entire file to see if they can overturn and approve the mortgage loan because the Desktop Underwriting Automated Software could not approve you.

With scores below 620, they typically will want to verify your rent history, have no bankruptcies in the last two years, and no foreclosures in the last 3 years.

If you have had any lates since the bankruptcy this will probably result in a denial on a refer manual underwrite file.

Your max house payment will be set at 31% of your gross monthly income, and your new house payment plus the bills you are paying on the credit report cannot be more than 43%.

Typically, on scores below 620 for FHA loans, they will also look at reserves or money you have saved up after the loan is made to try and qualify you. For example, if you have a 401k or savings account that has at least 4 months reserves (take your mortgage payment x 4) and this would equal your reserves. They look at this as a rainy day fund and could help you keep up on your bills if you were unemployed or could not work.

The first thing to keep in mind is that qualifying for a mortgage involves a lot more than just a credit score. While your FICO score is a very important ingredient, it is just one factor. Lenders also look at your income and level of debt, among other things.

A FICO score between 600 and 640 is considered fair to good credit. But keep in mind, this range of credit scores does not guarantee you will qualify for a mortgage, and if you do qualify, it won’t get you the lowest interest rate possible. Still, to buy a home aim for a score of at least 620, recognizing that other factors weigh in the decision and that some banks may require a higher score.

What credit score do you need to get a low rate mortgage?

It uses to be that a score of about 720 would yield the lowest mortgage rates available. Today, the best rates kick in with a FICO score of 760. And interest rates go up significantly as your credit score drops. To give you an idea, the following table shows current rates by credit score and calculates a monthly principal and interest payment based on a $300,000 loan:

lenders will pull what they call a “tri-merge” credit report which will show three different fico scores from Transunion, Equifax, and Experian. The lenders will throw out the high and low scores and take the “middle score.” For example, if you had a 614, 610, and 629 score from the three main credit bureaus, your qualifying score would be 614.

So if you only have one score, you may not qualify. Lenders will have to pull their own credit report and scores so if you had it ran somewhere else or saw it on a website or credit card you may own, it will not matter to the lender, because they have to use their own credit report and scores.

Lastly, lenders will pull your credit report for free nowadays so this should not be a big deal as long as your scores are high enough.

offered by FHA, VA, USDA, Fannie Mae, and KHC all have their minimum fico score requirements and lenders will create overlays in addition to what the Government agencies will accept, so even if on paper FHA says they will go down to 580 or 500 in some cases on fico scores,

If you have low fico scores it may make sense to check around with different lenders to see what their minimum fico scores are for loans.

The lenders I currently deal with have the following fico cutoffs for credit scores:

As you can see, different government-backed loan programs have different minimum score requirements with most lenders for an FHA, VA, or Fannie Mae loan, and 620 is required for the no down payment programs offered by USDA and KHC in Kentucky for First Time Home Buyers wanting to go no money down.

By paying down your credit card balances (credit utilization) and having a good pay history (payment history) ,this is the best way to raise your score.

The credit bureaus don’t update immediately, so I would not add to the balance or open any new bills or have any other lender do an inquiry on your credit report while we wait for the scores to hopefully go up in the next 30 days. Try to keep everything status quo and make your payments on time and keep your balances low or lower than what is now reporting on the credit report.

How to improve your credit score!

Pay Every Single Bill on Time, or Early, Every Month

Please understand one thing; paying your bills on time each month is the single most important thing you can do to increase your credit scores.

Depending on the credit bureau, there are 4 or 5 main items that determine everyone’s credit score. Of those items, your history of paying bills makes up about 35% of the score. THIS IS HUGE!

Paying your bills on time shows lenders that you are responsible. It will also spare you from paying late fees whether it is a charge from a credit card or an added fee from your landlord.

Use a calendar, or a phone app, or some other organized system to make sure that you pay your bills on time every single month.

Another big factor in calculating a credit score is the amount of credit card debt. Credit bureaus look at two things when analyzing your credit cards.

First, they look at your available credit limit. Second, they look at the existing balance on each card. From these two figures an available ratio is developed. As the ratio goes higher, so too will your credit score increase.

Here is one simple example. Suppose a person has the following credit cards, corresponding balances, and credit limits

Credit Card

Current Balance

Credit Limit

Chase Visa

$105

$1,000

MarterCard from local bank

$236

$1,500

BP MasterCard

$87

$500

Totals

$428

$3,000

From these numbers, we get the following calculation

$428/$3,000 = 14%

In other words, the person is using 14% of their available credit and they have 86% available credit. The closer that ratio is to 100%, the better the credit score will be.

MAIN TIP: Keep all credit card balances as low as possible.In this particular example, if they had a problem with their car, or needed medical attention or some other emergency, the person would have the money necessary to handle the situation without incurring new debt. This is wise on the consumer’s part and lenders like to see this kind of money management.

Credit Cards Part 2: 1 or 2 is Better Than a Wallet Full

The previous example showed a person that utilized just three credit cards. This is much better than someone who has 5+ credit cards, all with available balances. Why? Lenders do not like to see someone that has the potential to get too far in debt in a short amount of time.

Some people have 5, 10 or more credit cards and they use many of them. This shows a lack of restraint and control. It is much better, and neater, to have only 2 or 3 cards with low rates that handle all of your transactions. A lower number of cards are easier to manage and it does not give a person the temptation to go on a huge shopping spree that could take years to payoff.

MAIN TIP: Try to limit yourself to no more than 2-3 credit cards.

Keep the Good Stuff Right Where it is

Too many people make the mistake of paying off old debts, such as old credit cards, and then closing the account. This is actually a bad idea.

A small part of the credit score is based on the length of time a person has had credit. If you have a couple of credit cards with a long track history of making payments on time and keeping the balance at a manageable level, it is a bad idea to close out the card.

Similarly, if you have been paying on a car or motorcycle for a long time, do not be in a hurry to pay off the balance. Continue to make the payments like clockwork each month.

An account that has a good record will help your scores. An account that has a good record and multiple years of use will have an even better impact on your score.

MAIN TIP: Keep old accounts open if you have a good payment history with them.

Stop Filling Out Credit Applications

Multiple credit inquiries in a short amount of time can really hurt your credit scores. Lenders view the various inquiries as someone that is desperate and possibly on the verge of making a bad financial choice.Too many people make the mistake of getting more credit after they are approved for a loan. For example, if someone is approved for a new credit card, they feel good about their finances and decide to apply for credit with a local furniture store. If they get approved for the new furniture, they may decide to upgrade their car. This requires yet another loan. They are surprised to learn that their credit score has dropped and the interest rate on the new car loan will be much higher. What happened?

If you currently have 2 or 3 credit cards along with either a car loan or a student loan, don’t apply for any more debt. Make sure the payments on your current debt are all up to date and focus on paying them all down.

In a few months of making timely payments your scores should noticeably go up.

MAIN TIP: Limit your new loans as much as possible

Which credit scores do mortgage lenders use to qualify people for a mortgage?

While it’s common knowledge that mortgage lenders use FICO scores, most people with a credit history have three FICO scores, one from each of the three national credit bureaus (Experian, Equifax, and TransUnion).

Which FICO Score is Used for Mortgages

Most lenders determine a borrower’s creditworthiness based on FICO® scores, a Credit Score developed by Fair Isaac Corporation (FICO™). This score tells the lender what type of credit risk you are and what your interest rate should be to reflect that risk. FICO scores have different names at each of the three major United States credit reporting companies. And there are different versions of the FICO formula. Here are the specific versions of the FICO formula used by mortgage lenders:

Equifax Beacon 5.0

Experian/Fair Isaac Risk Model v2

TransUnion FICO Risk Score 04

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

Which Score Gets Used?

Since most people have three FICO scores, one from each credit bureau, how do lenders choose which one to use?

For a FICO score to be considered “usable”, it must be based on adequate, concrete information. If there is too little information, or if the information is inaccurate, the FICO score may be deemed unusable for the mortgage underwriting process. Once the underwriter has determined if a score is usable or not, here’s how they decide which score(s) to use for an individual borrower:

If all three scores are different, they use the middle score

If two of the scores are the same, they use that score, regardless of whether the two repeated scores are higher or lower than the third score

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

Kentucky First-Time Home Buyer Programs 2026: Complete Guide to FHA, VA, USDA & KHC Loans

Kentucky First-Time Home Buyer Programs in 2026: Your Complete Guide to FHA, VA, USDA, Conventional, and KHC Loans

Buying your first home in Kentucky in 2026? You’re entering a market with more options than ever before. Updated loan limits, competitive interest rates, and powerful down payment assistance programs are making homeownership more accessible for Kentucky families across all 120 counties.

What are the best Kentucky homebuyer programs for 2026?

The main options for Kentucky homebuyers in 2026 include Conventional Loans, FHA Loans, VA Loans, USDA Loans, and Kentucky Housing Corporation (KHC) Down Payment Assistance programs. Each offers distinct advantages depending on your credit score, down payment savings, income level, and location.

This comprehensive guide breaks down every program, updated with 2026 loan limits, credit requirements, and qualification guidelines to help you make informed decisions about your home purchase.

Conventional Mortgage Loans in Kentucky (2026)

Conventional loans remain the most popular choice for Kentucky homebuyers with good credit and stable income. These loans are not government-backed, which means they follow stricter underwriting standards but offer significant benefits for qualified borrowers.

2026 Conventional Loan Requirements:

Credit Score: Minimum 620 (preferred 740+ for best rates)

Down Payment: As low as 3% for qualified first-time buyers; 5% for repeat buyers

Debt-to-Income Ratio (DTI): Maximum 43-50% (varies by lender and compensating factors)

2026 Loan Limits for Kentucky:

Single-Family Home: $832,750

Two-Unit Property: $1,066,000

Three-Unit Property: $1,288,750

Four-Unit Property: $1,601,750

Additional Requirements:

Work History: Two years of consistent employment in the same field or industry

Bankruptcy & Foreclosure Waiting Periods:

No foreclosure in the past 7 years

No Chapter 7 bankruptcy in the past 4 years

Chapter 13 bankruptcy allowed after 2 years of discharge with court approval

Loan-to-Value (LTV): Up to 97% for qualified first-time buyers

Private Mortgage Insurance (PMI): Required for down payments under 20%; can be canceled once you reach 20% equity

Required Documentation:

Last two years of W-2 forms

Last 30 days of pay stubs

Two years of federal tax returns (self-employed or commissioned income)

Last two months of bank statements

Tri-merge credit report from lender

Why Choose Conventional? Borrowers with credit scores of 740+ and 20% down payments often prefer conventional loans because they can avoid mortgage insurance entirely and typically secure the lowest interest rates available.

Kentucky FHA Loans (2026)

FHA loans are designed specifically for first-time homebuyers and those with lower credit scores or limited savings. Backed by the Federal Housing Administration, these loans offer the most flexible qualification guidelines of any mortgage program.

2026 FHA Loan Requirements:

Credit Score:

580+ for 3.5% down payment

500-579 for 10% down payment

Down Payment: As low as 3.5%

Debt-to-Income Ratio:

Front-End Ratio: Maximum 31% (housing costs only)

Back-End Ratio: Maximum 43-57% with compensating factors

2026 FHA Loan Limits for All Kentucky Counties:

Single-Family Home: $541,287

Two-Unit Property: $693,050

Three-Unit Property: $837,700

Four-Unit Property: $1,041,125

FHA Waiting Periods:

Foreclosure: 3 years minimum

Chapter 7 Bankruptcy: 2 years minimum

Chapter 13 Bankruptcy: 12 months of on-time payments with trustee approval

Work History Requirements:

Two years of steady employment in the same industry

Gaps exceeding 6 months in the past 2 years must be explained

Multiple job changes (3+ in 12 months) may require additional documentation

Recent college graduates can substitute education for work history

FHA Mortgage Insurance:

Upfront Premium: 1.75% of loan amount (can be financed into loan)

Annual Premium: 0.45% to 1.05% (paid monthly), based on loan amount and down payment

Required Documentation:

Same as conventional loans, plus:

12-24 months of rental payment history (if manually underwritten)

Verification of non-traditional credit (if applicable)

Why Choose FHA? Perfect for first-time buyers rebuilding credit, those with limited savings, or anyone who has experienced past financial challenges. FHA loans are more forgiving and accessible than conventional financing.

Kentucky VA Home Loans (2026)

VA loans provide unmatched benefits for eligible veterans, active-duty service members, National Guard members, Reservists, and qualifying surviving spouses. These loans eliminate major barriers to homeownership.

2026 VA Loan Benefits:

Down Payment: Zero down payment required

Mortgage Insurance: No monthly PMI required (major savings)

Credit Score: Minimum 580-620 (varies by lender)

Debt-to-Income Ratio: No maximum DTI with sufficient residual income

2026 VA Loan Limits for Kentucky:

Veterans with full entitlement have no loan limit

Partial entitlement follows conforming limits: $832,750 for single-family homes

VA Loan Requirements:

Certificate of Eligibility (COE): Required; obtain through VA website or your lender

Work History: Two years of consistent employment

Waiting Periods:

No foreclosure in the past 2 years

No Chapter 7 bankruptcy in the past 2 years

Chapter 13 bankruptcy allowed after 12 months with trustee approval

Loan-to-Value (LTV): Up to 100% for purchases; 100% for cash-out refinances

VA Funding Fee: 1.25% to 3.3% of loan amount (waived for disabled veterans)

Required Documentation:

Certificate of Eligibility (COE)

DD-214 (for veterans)

Statement of Service (for active duty)

Standard income/asset documentation

Why Choose VA? The combination of no down payment, no monthly mortgage insurance, and competitive interest rates makes VA loans the most powerful financing option available for eligible borrowers.

USDA Loans in Kentucky (2026)

USDA loans offer 100% financing for eligible rural and suburban properties throughout Kentucky. Despite the “rural” designation, many suburban areas qualify, including parts of major metro areas.

2026 USDA Loan Requirements:

Credit Score: Minimum 620 (preferred 640+ for automated approval)

Down Payment: Zero down payment required

Debt-to-Income Ratio:

Front-End: Maximum 29-32%

Back-End: Maximum 41-45% (higher with compensating factors through GUS system)

Income Limits: Must not exceed 115% of area median income (varies by county and household size)

Property Eligibility: Home must be in USDA-designated eligible area

USDA Waiting Periods:

Foreclosure: 3 years minimum

Chapter 7 Bankruptcy: 3 years minimum

Chapter 13 Bankruptcy: 12 months of on-time payments with trustee approval

USDA Guarantee Fee:

Upfront Fee: 1% of loan amount (can be financed)

Annual Fee: 0.35% (paid monthly)

Work History Requirements:

Two years of steady employment

Seasonal or temporary work may qualify with sufficient documentation

Why Choose USDA? Perfect for buyers purchasing in eligible rural or suburban areas who want 100% financing. Many Kentucky locations qualify, including areas near Louisville, Lexington, and other cities.

The Kentucky Housing Corporation offers the most comprehensive suite of programs for first-time homebuyers in the state, combining competitive interest rates with substantial down payment assistance.

KHC Down Payment Assistance Program (2026):

Assistance Amount: Up to $12,500

Structure: Second mortgage at 3.75% interest rate for 10 years

Usage: Can be used for down payment, closing costs, and prepaid expenses

Repayment: Monthly payments required; not forgivable

2026 KHC Program Options:

1. Conventional Preferred Program

Down payment as low as 3%

Available to low- to moderate-income borrowers

Private mortgage insurance required

Income limits apply (varies by county)

2. Conventional Preferred Plus 80 Program

Down payment as low as 3%

Available to higher-income borrowers (up to $181,300+ depending on county)

First-time and repeat buyers eligible

PMI required

3. Mortgage Revenue Bond (MRB) Program

Below-market interest rates

Available with FHA, VA, USDA, or Conventional loans

First-time buyer requirement (waived in targeted areas)

Maximum purchase price: $544,232

2026 KHC Income Limits (Examples):

Income limits vary by county and household size. Here are representative examples:

Jefferson County (Louisville): $95,000-$181,300 (depending on program and household size)

Fayette County (Lexington): $92,000-$176,000

Rural Counties: Generally lower limits; check with KHC-approved lender

KHC Purchase Price Limits (2026):

Maximum Purchase Price: $544,232 for most programs

Some programs have lower limits; verify with your lender

KHC Eligibility Requirements:

Must purchase primary residence in Kentucky

Property must meet KHC appraisal standards

Income and purchase price limits apply

First-time homebuyer requirement for most programs (waived in targeted areas)

Must complete homebuyer education course

Why Choose KHC? The combination of below-market interest rates and up to $12,500 in down payment assistance can save Kentucky homebuyers thousands of dollars over the life of their loan.

2026 Kentucky Welcome Home Grant

The Kentucky Welcome Home Grant is expected to return in March 2026, offering additional down payment assistance to eligible Kentucky homebuyers.

2026 Welcome Home Grant Details:

Grant Amount: To be announced (historically $7,500-$20,000)

Availability: First-come, first-served basis; funds typically depleted within weeks

Structure: Forgivable grant (not a loan)

Eligibility: Income limits and first-time buyer requirements apply

Launch Date: Expected March 2026

Important: The Welcome Home Grant consistently sells out within days of opening. Get pre-approved now and be ready to act immediately when the program launches.

Comparison: Kentucky Mortgage Loan Program Requirements (2026)

Program

Min. Credit Score

Down Payment

Max DTI

2026 Loan Limit (1-Unit)

Conventional

620

3-5%

43-50%

$832,750

FHA

580

3.5%

31/43-57%

$541,287

VA

580-620

0%

No max*

$832,750 (or unlimited)

USDA

620

0%

29/41-45%

Based on income limits

KHC Programs

Varies

3-3.5%

Varies by loan type

$544,232

*VA loans evaluate residual income rather than strict DTI limits

Step-by-Step: How to Apply for a Kentucky Home Loan in 2026

Step 1: Check Your Credit Score

Obtain free credit reports from all three bureaus

Review for errors and dispute inaccuracies

Work on improving your score if below 620

Step 2: Calculate Your Budget

Determine how much you can afford monthly

Factor in property taxes, insurance, HOA fees

Use online mortgage calculators for estimates

Step 3: Get Pre-Approved

Contact a Kentucky-licensed mortgage professional

Submit required documentation

Receive pre-approval letter (typically same-day)

Step 4: Choose Your Loan Program

Compare options based on your situation

Consider credit score, down payment, income, and location

Ask about combining KHC assistance with other programs

Step 5: Find Your Home

Work with a licensed Kentucky real estate agent

Stay within your pre-approved amount

Ensure property meets program requirements

Step 6: Submit Full Application

Complete formal loan application

Provide any additional documentation requested

Coordinate home inspection and appraisal

Step 7: Close on Your Home

Review closing disclosure carefully

Bring required funds to closing

Sign documents and receive keys

Frequently Asked Questions

Q: Can I combine KHC down payment assistance with FHA or VA loans?

A: Yes! KHC assistance can be layered with FHA, VA, USDA, or Conventional loans, making it possible to buy with minimal out-of-pocket costs.

Q: What’s the difference between the Welcome Home Grant and KHC down payment assistance?

A: The Welcome Home Grant is a forgivable grant (not repaid), while KHC down payment assistance is a second mortgage with monthly payments at 3.75% interest.

Q: Do all Kentucky counties have the same FHA loan limits?

A: Yes. For 2026, all 120 Kentucky counties use the same FHA floor limit of $541,287 for single-family homes.

Q: Can I buy a multi-unit property with these programs?

A: Yes! FHA, VA, and Conventional loans all allow 2-4 unit purchases, with the requirement that you occupy one unit as your primary residence.

Q: How long does the mortgage approval process take?

A: Pre-approval typically happens within 24 hours. Full approval to closing typically takes 30-45 days depending on the loan type and your responsiveness.

Q: What if I have student loan debt?

A: All programs allow student loan debt. Lenders will calculate either 0.5-1% of the balance or use your actual payment amount in DTI calculations.

Why Work With a Kentucky Mortgage Specialist?

Navigating multiple loan programs, down payment assistance options, and changing requirements requires expertise and local knowledge. Working with a Kentucky-licensed mortgage professional who specializes in first-time homebuyer programs ensures:

✓Accurate Pre-Approval: Same-day approvals with correct numbers

✓Program Expertise: Knowledge of all available KHC and state programs

✓Competitive Rates: Access to wholesale pricing and special programs

✓Local Market Knowledge: Understanding of Kentucky’s 120 counties

✓Personalized Service: One-on-one guidance throughout the entire process

Get Started Today

Ready to explore your Kentucky home buying options? The 2026 loan limits and programs provide more opportunities than ever for Kentucky families to achieve homeownership.

Joel Lobb

Mortgage Loan Officer – Kentucky Mortgage Loan Specialist

20+ Years Experience | 1,300+ Families Helped

NMLS Personal ID: 57916

Company NMLS ID: 1738461

Services Available:

✓ Free mortgage applications with same-day approval

✓ All 120 Kentucky counties served

✓ FHA, VA, USDA, Conventional, and KHC programs

✓ Down payment assistance guidance

✓ First-time homebuyer counseling

Equal Housing Lender | Licensed for Kentucky Mortgage Loans Only

Disclaimer: This website is not endorsed by or affiliated with the FHA, VA, USDA, or any government agency. Information provided is for educational purposes. Loan programs, rates, and requirements subject to change. All borrowers must meet program eligibility requirements.

2026 Kentucky Housing Market Outlook

Kentucky’s housing market continues to show strength in 2026, with steady home price appreciation and competitive interest rates creating favorable conditions for buyers. The increased loan limits provide greater purchasing power, while expanded down payment assistance programs make homeownership more accessible.

Whether you’re a first-time buyer, a veteran, or someone looking to purchase in a rural area, Kentucky’s diverse loan programs offer a pathway to homeownership that fits your unique financial situation.

Are you a prospective homebuyer in Kentucky searching for the best mortgage lenders? Joel Lobb is a trusted mortgage broker. He has a proven track record of helping clients secure competitive mortgage rates. He also helps clients with financing options. With Joel Lobb by your side, you can access top-notch mortgage lenders in Kentucky. He will help you make your dream of homeownership a reality.

Joel Lobb has established strong relationships with a network of reputable mortgage lenders in Kentucky. These lenders offer a wide range of loan programs. These programs can suit your unique needs and financial goals. Whether you’re a first-time homebuyer, a seasoned investor, or looking to refinance your existing mortgage, Joel Lobb can connect you with the best mortgage lenders that offer:

Competitive Interest Rates: Access mortgage loans with competitive interest rates. These rates can save you money over the life of your loan.

Flexible Loan Programs: Choose from a variety of loan programs. These include FHA, VA, USDA, conventional, jumbo loans, and more. They are tailored to your specific requirements.

Personalized Guidance: Receive personalized guidance and support throughout the mortgage process. This includes steps from pre-qualification to closing. These efforts ensure a smooth and stress-free experience.

Quick and Efficient Approval: Benefit from efficient loan processing. Experience quick approval times, allowing you to close on your new home faster.

Transparent and Honest Service: Experience transparent and honest communication throughout your mortgage journey. We provide full transparency on loan terms, fees, and requirements.

When you are looking for the best mortgage lenders in Kentucky, Joel Lobb stands out. He is a trusted advisor and advocate for his clients’ best interests. With Joel Lobb’s expertise and industry knowledge, you can navigate the complex world of mortgage lending with confidence. You can achieve your homeownership goals.

Contact Joel Lobb today. Learn more about the best mortgage lenders in Kentucky. Start your journey towards owning the perfect home for you and your family.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Click here to apply for Free Info & Homebuyer Advice →

Click here to apply for Free Info & Homebuyer Advice →