Joel Lobb specializes in a wide array of mortgage loans, including:

– **FHA Loans**: These loans are a great fit for buyers with lower credit scores or those who can afford only a minimal down payment.

– **VA Loans**: Tailored for veterans and active military members, offering favorable terms with little to no down payment.

– **USDA Loans**: Designed for rural home buyers, providing 100% financing options.

– **KHC Loans**: In collaboration with the Kentucky Housing Corporation, these loans come with down payment assistance, making them ideal for first-time buyers.

Complete Guide to FHA Loan Requirements in Kentucky

FHA loans are a popular choice for many first-time homebuyers in Kentucky. This is due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

- Credit Score Requirements:

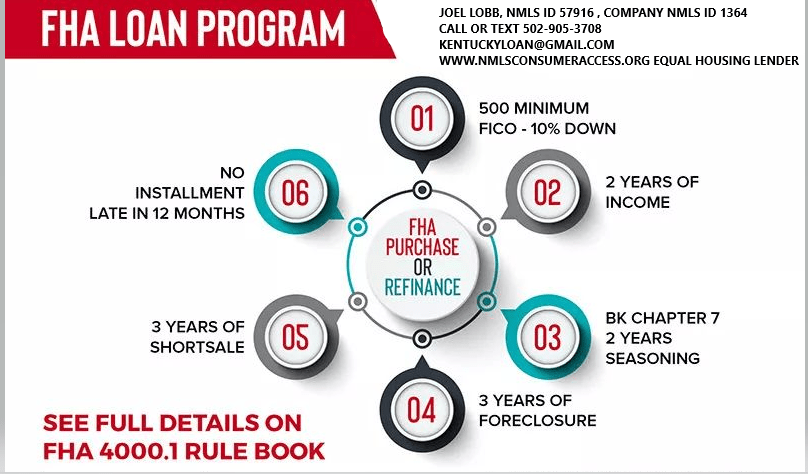

- FHA loans are known for accommodating borrowers with lower credit scores. The minimum required credit score can vary. Typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. Borrowers with credit scores between 500 and 579 might still qualify. They will need a higher down payment, usually around 10%.

- Down Payment:

- The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

- Work History:

- Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history is beneficial. It is preferable to have worked with the same employer or within the same field. This helps demonstrate financial stability and the ability to repay the loan.

- Debt-to-Income Ratio (DTI):

- The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income. It can go higher up to 56% with good credit scores, a large down payment, or a shorter-term loan. Lenders may also consider higher ratios in certain cases if compensating factors are present.

- Bankruptcy and Foreclosure:

- FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years. This is possible if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

- Mortgage Term:

- FHA loans offer various mortgage term options, including 15-year, 20 year, 25 year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

- Occupancy: Primary residences with 1-4 units. Not for investment properties or second homes.

- Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

- can be used for refinances, not only for purchases.

- No income limits nor property restrictions on where home is located

- Can close within 30 days typically with good appraisal and title work

FHA Loan Requirements in Kentucky for Credit scores, Down payment, Debt Ratio and work history below

| Requirement | Details |

|---|---|

| Credit Score | – 580+: Eligible for a 3.5% down payment. – 500-579: Requires a 10% down payment. |

| Down Payment | Minimum of 3.5% for qualified buyers; 10% for lower credit scores below 580 to 500 score range |

| Debt-to-Income Ratio (DTI) | – Ideal: 45% or lower on front end ratio or housing ratio. – Acceptable: Up to 57% with compensating factors. There are two ratios. Front end and back end with front end being maxed at 45% and the backed end ratio being 56.99% with an AUS approval. If manually underwritten, see guidelines here |

| Employment History | Must provide at least **2 years of consistent employment—College transcripts can supplement with a less than 2 year work history |

Key Benefits of FHA Loans in Kentucky

- Low Credit Score Requirements

- FHA loans accept borrowers with credit scores as low as 500. However, a score of 580+ qualifies you for the lowest down payment option.

- Low Down Payment Options

- You can purchase a home with as little as 3.5% down if you meet credit requirements, making FHA loans more accessible than conventional loans.

- Competitive Interest Rates

- FHA loans typically offer rates comparable to conventional mortgages. They may even offer lower rates. This could save you money over the life of the loan.

- Flexible Loan Uses

- With an FHA 203(k) loan, you can bundle home purchase and renovation costs into a single mortgage.

- Assumable Loans

- FHA loans can be transferred to a new buyer. This feature is especially valuable if you sell your home when interest rates are higher.

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can provide valuable guidance. They offer assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

Any questions, please don’t hesitate to reach out via, text, email, or call. Advice is always free.

One of Kentucky’s highest rated mortgage loan officers for FHA, VA, USDA, Kentucky Housing KHC and conventional mortgage loans.

1 –  Email – kentuckyloan@gmail.com

Email – kentuckyloan@gmail.com

Email – kentuckyloan@gmail.com 2.  Call/Text – 502-905-3708

Call/Text – 502-905-3708

Call/Text – 502-905-3708Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com

Website: www.mylouisvillekentuckymortgage.com Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

(www.nmlsconsumeraccess.org).

(www.nmlsconsumeraccess.org).

Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans

MINIMUM CREDIT SCORES REQUIRED FOR KENTUCKY FHA, VA, USDA MORTGAGE LOANS

-

Kentucky FHA Loans: Kentucky FHA loans are known for their lenient credit score requirements, making them accessible to borrowers with lower credit scores. However, a minimum score of 500 to 580 is typically required, depending on the down payment.

-

Kentucky VA Loans: VA loans offer flexible credit score requirements, while on paper VA states they don’t require a minimum score to insure the mortgage loan, most lenders preferring a FICO score of 620 or higher. Veterans, active-duty service members, and eligible spouses can benefit from VA loan options.

-

Kentucky USDA Loans: USDA loans are designed for rural homebuyers and require no minimum FICO score , but most lenders will want a credit score of 640 or higher. These loans offer zero down payment options for eligible properties.

-

KHC Mortgage Loans: Kentucky Housing Corporation (KHC) mortgage loans may vary in credit score requirements depending on the lender. It’s essential to work with a knowledgeable mortgage broker like Joel Lobb to understand specific lender guidelines. KHC requires a minimum 620 credit score for FHA, VA, USDA and 660 for Conventional loan programs

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

Credit Score Requirements for Kentucky Home Buyers

What Credit Score Do You Need to Buy a House in Kentucky?

There is no single “magic number.” The credit score needed depends on the loan program (Conventional, USDA, FHA, VA, or Kentucky Housing Corporation down payment assistance). Here’s how it works in the real world for Kentucky buyers.

Conventional Loans in Kentucky

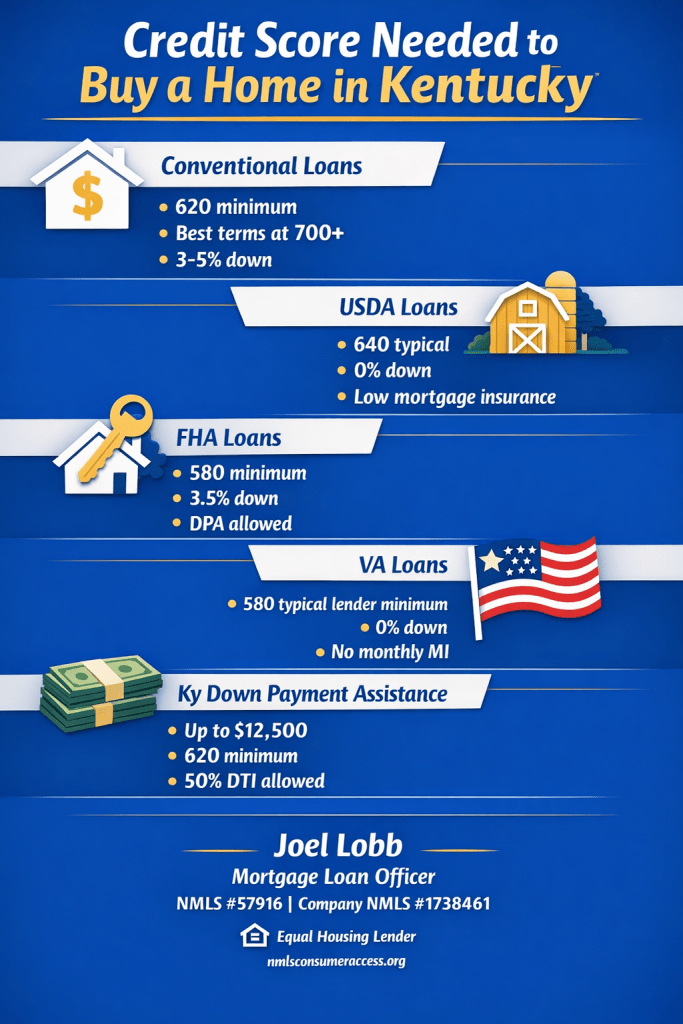

- Minimum credit score generally starts at 620.

- Most lenders prefer higher scores for 3%–5% down options.

- Best pricing and easier approvals are typically with strong credit (often 700+).

- Mortgage insurance (PMI) usually improves as scores increase.

USDA Rural Housing Loans in Kentucky

- Many lenders target around 640 for automated approval through GUS (Guaranteed Underwriting System).

- Manual underwriting may be possible when automated approval is not available.

- 0% down payment required (eligible rural/suburban areas).

- Typical fees include a 1% upfront guarantee fee and 0.35% annual fee (paid monthly).

USDA can be one of the best value options for Kentucky buyers with limited cash, provided the property is in an eligible area and the file meets income and underwriting requirements.

Kentucky FHA Loans

- As low as 580 credit score with 3.5% down (typical baseline).

- Gift funds, grants, and down payment assistance may be allowed.

- Mortgage insurance is generally higher than USDA or VA, but rates can still be competitive.

- Common waiting periods: 2 years after bankruptcy and 3 years after foreclosure (standard guideline).

Kentucky VA Loans

- VA does not set a minimum credit score in its guidelines, but most lenders do.

- Many VA lenders target around 580+ (lender overlay varies).

- 0% down and no monthly mortgage insurance.

- Clear CAIVRS is required (for federal delinquency screening).

Kentucky Down Payment Assistance (KHC)

- Kentucky Housing Corporation (KHC) often offers up to $12,500 down payment assistance (program terms and funding can change).

- Typically structured as a second mortgage paid back over 15 years.

- Minimum credit score is commonly 620 across many KHC options; KHC conventional often requires 660.

- Maximum debt-to-income ratios are commonly around 50/50 (program and investor rules apply).

Next step: get a clear pre-approval target

If you share your approximate credit score range, income type, and whether you’re looking in Louisville, Lexington, or rural Kentucky, I can point you to the most realistic program and the exact score threshold that will matter for approval.

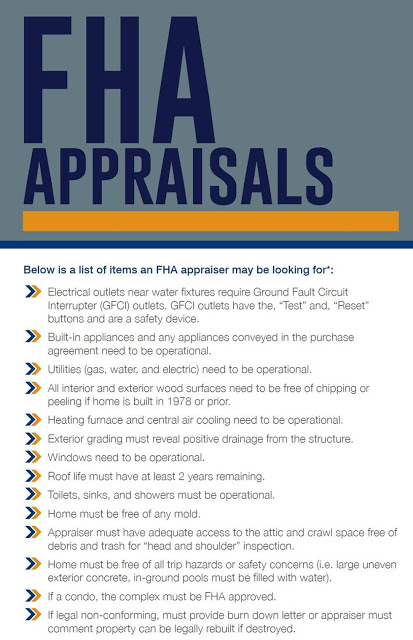

Kentucky FHA Appraisal Requirements For A Mortgage Loan Approval.

- Ordered through a third party source. Interested/vested parties may not initiate the appraisal. I.E> buyers, sellers, realtors, loan officer, family members

- Property must meet HUD’s minimum property standards. i.e.: permanent heat source, utilities must be on and in working order at time of inspection

- Flips < 90 days – not allowed Per HUD -If current owner owned less than 90 days FHA will not insure. Sometimes a second appraisal will be required by FHA investor if sold within the last 6 months for a large profit. Receipts of work done may be needed to substantiate increase in value of home in short-time period.

- Transferred appraisal – ok

- Appraisal valid 120 days – 30 day extension possible*

- Property eligibility – No location restrictions.

- New Construction Available

FHA MORTGAGE LOANS AND FLIPPING RULE FOR APPRAISALS

Resales Occurring 90 Days or Fewer after Acquisition:

Not eligible for FHA financing

Resales occurring between 91 days and 180 Days after Acquisition:

Obtain 2nd appraisal if resold between 91 to 180 days after acquisition

Obtain 2nd appraisal if resale price is 100% or more over price paid by seller

If 2nd appraisal is more than 5% lower than value of first appraisal, the lower value must be used

Borrower not allowed to pay for 2nd appraisal

Exceptions to FHA Flipping Rules:

Property purchased by an employer or relocation company due to relocation of an employee

Resales by HUD – REO program

Sales by other government agencies (i.e., IRS, court-ordered, DEA, etc.)

Sales of non-profit agencies approved to purchase HUD properties

Acquisition due to inheritance

Sales of properties by federally chartered financial institutions

Sales of properties by GSE’s

Sales of properties by local or state governments

Sales by builders selling a new home

Sales of properties in federally declared disaster areas

NOTE: Mortgage Company must obtain a 12-month chain of title to document time restrictions above.

VA MORTGAGE AND FLIPPING RULE

No Flipping Rules – Overlays may apply or at Underwriter’s discretion

USDA RURAL HOUSING MORTGAGE FLIPPING RULES

Lender is responsible to ensure that any recently sold property’s value is strongly supported when a significant

increase between sale and purchase occurs.

Lender must ensure that the appraisal value is supported with validated comps and protect the borrower from

predatory lending.

Fannie Mae Appraisal Flipping Rules

No Flipping Rules – Lender overlays may apply

Freddie Mac

No Flipping Rules – Lender overlays may apply

Applies to case numbers assigned on or after June 1, 2022

Updates the initial appraisal validity period from 120 days to 180 days from the effective date of the appraisal report;

Extends the appraisal update validity period from 240 days to one year from the effective date of the initial appraisal report;

Allows the appraisal update to be ordered AFTER an appraisal expires; and

Eliminates the optional 30-day extension.

✨This is big news for FHA ✨

The guideline change also puts FHA appraisal expirations on par with conventional loan expiration dates.

Kentucky FHA appraisals can take home buyers by surprise. That’s why we’ve put together some good-to-know info about the process. Feel free to use this to help educate your clients.

Joel Lobb

Senior Loan Officer

Senior Loan Officer

(NMLS#57916)

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.

Kentucky FHA Loan Credit Score Requirements

What credit score do you need to qualify for a Kentucky FHA loan? Straight talk: the Federal Housing Administration (FHA) requires a minimum credit score of 500 to be eligible. However, your final terms depend on your score and your lender’s additional requirements (known as overlays).

FHA Minimum Credit Guidelines (HUD)

- 580 and up: Eligible for 96.5% financing — 3.5% down.

- 500–579: Eligible for 90% financing — 10% down.

- Under 500: Not eligible for FHA financing.

Two Things You Must Satisfy

There are two layers of approval you must clear:

- HUD/FHA rules: The official, baseline eligibility outlined in the HUD Handbook (FHA’s mortgage insurance rules).

- Lender overlays: Individual lenders can and do impose stricter standards — often requiring scores from 580 to 620 or higher.

Why Lenders Use Overlays

Lenders add overlays to manage risk. Even if you meet FHA’s minimums, lenders evaluate:

- Debt-to-income (DTI) ratio

- Employment and income stability

- Source of down payment

- Recent credit history (late payments, collections, bankruptcies)

What Score Range Gets Approved Most Often?

In practice, most FHA approvals fall in the 600–699 range. Lower-score approvals (500–579) are possible but typically carry higher down payments, stricter DTI limits, and sometimes higher rates.

Next Steps — If Your Score Is Below 580

If you’re below 580, you have tactical options:

- Consider targeted credit repair to remove inaccurate items and lower utilization.

- Increase your down payment to reduce lender risk.

- Shop lenders — some local Kentucky lenders have more flexible overlays than others.

- Explore alternative programs: VA loans, USDA loans, and KHC programs may have different criteria.

Bottom Line

Meet FHA’s minimum of 500 to be eligible, but 580 or higher is the practical target to get the best terms (3.5% down and competitive rates). Your lender’s overlay will often be the deciding factor — so work with a lender who understands Kentucky’s market and can help you position your application.

Get pre-approved — Start your free applicationHow to Get A Kentucky FHA Upfront Mortgage Insurance Premium (UFMIP) Refund

FHA Mortgage Insurance Premium (MIP) guidelines is correct. As of March 2025, FHA loans require an upfront MIP of 1.75% of the loan amount. The annual MIP rates and their duration are influenced by factors. These factors include the loan term, loan amount, and loan-to-value (LTV) ratio.

Annual MIP Rates for FHA Loans with Terms Greater Than 15 Years:

- Loan Amounts ≤ $726,200:

- LTV ≤ 90%: Annual MIP of 0.50% for 11 years.

- LTV > 90% and ≤ 95%: Annual MIP of 0.50% for the life of the loan.

- LTV > 95%: Annual MIP of 0.55% for the life of the loan.

- Loan Amounts > $726,200:

- LTV ≤ 90%: Annual MIP of 0.70% for 11 years.

- LTV > 90% and ≤ 95%: Annual MIP of 0.70% for the life of the loan.

- LTV > 95%: Annual MIP of 0.75% for the life of the loan.

Annual MIP Rates for FHA Loans with Terms 15 Years or Less:

- Loan Amounts ≤ $726,200:

- LTV ≤ 90%: Annual MIP of 0.15% for 11 years.

- LTV > 90%: Annual MIP of 0.40% for the life of the loan.

- Loan Amounts > $726,200:

- LTV ≤ 78%: Annual MIP of 0.15% for 11 years.

- LTV > 78% and ≤ 90%: Annual MIP of 0.40% for 11 years.

- LTV > 90%: Annual MIP of 0.65% for the life of the loan.

1 – Email – kentuckyloan@gmail.com

2. Call/Text – 502-905-3708

Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

If you are an individual with disabilities who needs accommodation, please contact us at 502-905-3708. If you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications. These include income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals depend on underwriting guidelines, interest rates, and program guidelines. These can change without notice based on the applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

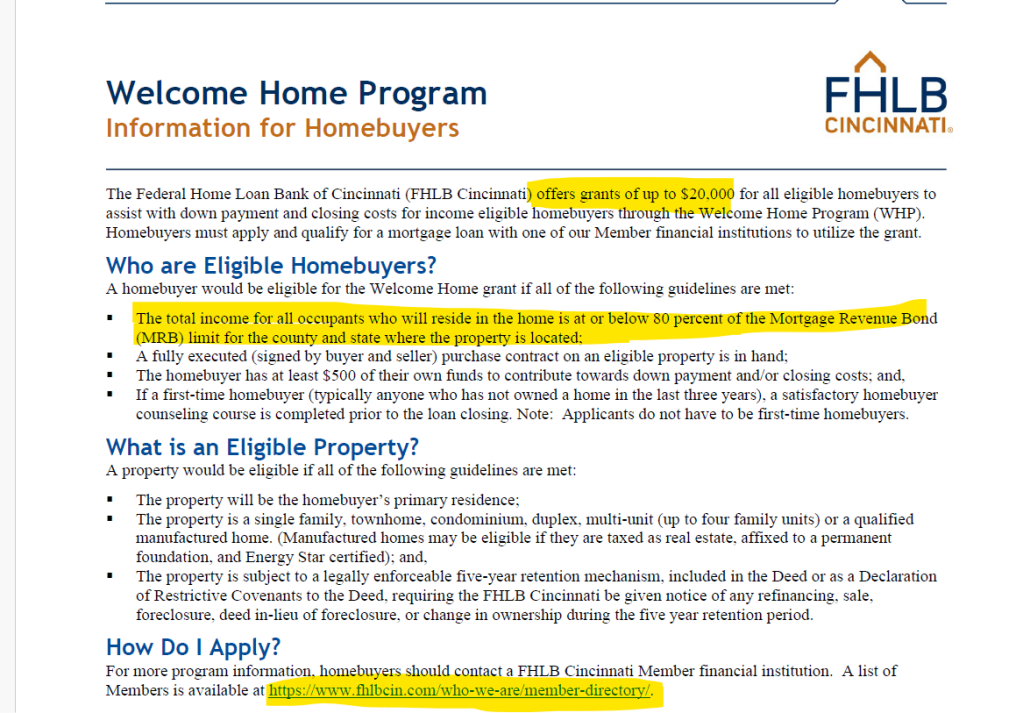

The income limits for the Kentucky Welcome Home Grant

1 – Email – kentuckyloan@gmail.com 2. Call/Text – 502-905-3708

Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.