The mortgage process can often be a confusing one — whether you’ve bought a home before or not. There’s a lot of prep work and moving parts, and most of the terminology is unfamiliar to the average consumer.

Fortunately, that last part is an easy fix.

Are you getting ready to buy a home or refinance your current mortgage? Take a look at some of the lesser-known terms you might want to know.

Annual Percentage Rate (APR): This number reflects the total annual cost of taking out your mortgage loan. It’s different from your mortgage interest rate and includes some extra fees.

Underwriting: When a loan professional evaluates your application and verifies all your financial details, that’s underwriting. It’s important to ensure that you have the means to manage your new monthly payment.

Escrow: An escrow account is used to hold funds prior to closing, including your earnest money deposit. You might also pay into an escrow account to cover property taxes, homeowners insurance and private mortgage insurance (if you have it).

Closing Disclosure: This is a document that you’ll be given at least three days before your closing date. It should detail all the final costs of your loan, as well as what you’ll be expected to pay on closing day.

Mortgage Note: You’ll sign this document at closing.It outlines the terms of your home loan and includes how much you’re borrowing, whether it’s a fixed-rate or adjustable-rate mortgage and more.

Prepaid Costs: These also come up at closing and will go into your escrow account. They usually cover mortgage interest, property taxes and homeowners insurance expenses that occur between your closing date and the date your first mortgage payment is due.

If you need help understanding any part of the mortgage process, get in touch today.

(1) Public Water Supply System The Mortgagee must confirm that a connection is made to a public or Community Water System whenever feasible and available at a reasonable cost. If connection costs to the public or community system are not reasonable, the existing onsite systems are acceptable, provided they are functioning properly and meet the requirements of the local health department.

(2) Individual Water Supply Systems (Wells) When an Individual Water Supply System is present, the Mortgagee must ensure that the water quality meets the requirements of the health authority with jurisdiction. If there are no local (or state) water quality standards, then water quality must meet the standards set by the EPA, as presented in the National Primary Drinking Water regulations in 40 CFR §§ 141 and 142. Soil poisoning is an unacceptable method for treating termites unless the Mortgagee obtains satisfactory assurance that the treatment will not endanger the quality of the water supply. Requirements for the location of wells for FHA-insured Properties are located in 24 CFR § 200.926d (f) (3). The following tables provide the minimum distance required between wells and sources of pollution for Existing Construction:

Individual Water Supply System for Minimum Property

Requirements for Existing Construction*

1

Property line/10 feet

2

Septic tank/50 feet

3

Drain field/100 feet

4

Septic tank drain field reduced to 75 feet if allowed by local authority

5

If the subject Property line is adjacent to residential Property then local well distance requirements prevail. If the subject Property is adjacent to non-residential Property or roadway, there needs to be a separation distance of at least 10 feet from the property line.

* distance requirements of local authority prevail if greater than stated above

The following provides the minimum requirements for water wells:

Water Wells Minimum Property Standards for New Construction

24 CFR § 200.926d(f)(1)

1

Lead-free piping

2

If no local chemical and bacteriological water standards, state standards apply

3

Connection of public water whenever feasible

4

Wells must deliver water flow of five gallons per minute over at least a four-hour period

Water Wells Minimum Property Requirements for Existing Construction

1

Existing wells must deliver water flow of three to five gallons per minute

2

No exposure to environmental contamination

3

Continuing supply of safe and potable water

4

Domestic hot water

5

Water quality must meet requirements of local jurisdiction or the EPA if no local standard

Shared WellsThe Mortgagee must confirm that a Shared Well:

serves existing Properties that cannot feasibly be connected to an acceptable public or Community Water supply System;

is capable of providing a continuous supply of water to involved Dwelling Units so that each existing Property simultaneously will be assured of at least three gallons per minute (five gallons per minute for Proposed Construction) over a continuous four-hour period. (The well itself may have a lesser yield if pressurized storage is provided in an amount that will make 720 gallons of water available to each connected existing dwelling during a continuous four-hour period or 1,200 gallons of water available to each proposed dwelling during a continuous four-hour period. The shared well system yield must be demonstrated by a certified pumping test or other means acceptable to all agreeing parties.);

provides safe and potable water. An inspection is required under the same circumstances as an individual well. This may be evidenced by a letter from the health authority having jurisdiction or, in the absence of local health department standards, by a certified water quality analysis demonstrating that the well water complies with the EPA’s National Interim Primary Drinking Water Regulations;

has a valve on each dwelling service line as it leaves the well so that water may be shut off to each served dwelling without interrupting service to the other Properties; and

serves no more than four living units or Properties.

For both proposed and existing Properties, the Mortgagee must ensure that the shared well agreement complies with the guidance provided in the following table.

Item

Provisions that must be reflected in any acceptable shared well agreement include the following:

1

Require that the agreement is binding upon signatory parties and their successors in title, recorded in local deed records when executed and recorded, and reflects joiner by any Mortgagee holding a Mortgage on any Property connected to the Shared Well.

2

Permit well water sampling and testing by the local authority at the request of any party at any time.

3

Require that corrective measures be implemented if testing reveals a significant water quality deficiency, but only with the consent of a majority of all parties.

4

Ensure continuity of water service to “supplied” parties if the “supplying” party has no further need for the shared well system. (“Supplied” parties normally should assume all costs for their continuing water supply.)

5

Prohibit well water usage by any party for other than bona fide domestic purposes.

6

Prohibit connection of any additional living unit to the shared well system without:· the consent of all parties;

· the appropriate amendment of the agreement; and

· compliance with item 3.

7

Prohibit any party from locating or relocating any element of an individual sewage disposal system within 75 feet (100 feet for Proposed Construction) of the Shared Well.

8

Establish Easements for all elements of the system, ensuring access and necessary working space for system operation, maintenance, improvement, inspection and testing.

9

Specify that no party may install landscaping or improvements that will impair use of the Easements.

10

Specify that any removal and replacement of preexisting site improvements, necessary for system operation, maintenance, replacement, improvement, inspection or testing, will be at the cost of their owner, except for costs to remove and replace common boundary fencing or walls, which must be shared equally between or among parties.

11

Establish the right of any party to act to correct an emergency in the absence of the other parties onsite. An emergency must be defined as failure of any shared portion of the system to deliver water upon demand.

12

Permit an agreement amendment to ensure equitable readjustment of shared costs when there may be significant changes in well pump energy rates or the occupancy or use of an involved Property.

13

Require the consent of a majority of all parties upon cost sharing, except in emergencies, before actions are taken for system maintenance, replacement or improvement.

14

Require that any necessary replacement or improvement of a system element(s) will at least restore original system performance.

15

Specify required cost sharing for:· the energy supply for the well pump;

· system maintenance, including repairs, testing, inspection and disinfection;

· system component replacement due to wear, obsolescence, incrustation or corrosion; and

· system improvement to increase the service life of a material or component to restore well yield or to provide necessary system protection.

16

Specify that no party is responsible for unilaterally incurred shared well debts of another party, except for correction of emergency situations. Emergency correction costs must be equally shared.

17

Require that each party be responsible for:· prompt repair of any detected leak in this water service line or plumbing system;

· repair costs to correct system damage caused by a resident or guest at their Property; and

· necessary repair or replacement of the service line connecting the system to the dwelling.

18

Require equal sharing of repair costs for system damage caused by persons other than a resident or guest at a Property sharing the well.

19

Ensure equal sharing of costs for abandoning all or part of the shared system so that contamination of ground water or other hazards will be avoided.

20

Ensure prompt collection from all parties and prompt payment of system operation, maintenance, replacement or improvement costs.

21

Specify that the recorded agreement may not be amended during the term of a federally-insured or -guaranteed Mortgage on any Property served, except as provided in items 5 and 11 above.

22

Provide for binding arbitration of any dispute or impasse between parties with regard to the system or terms of agreement. Binding arbitration must be through the American Arbitration Association or a similar body and may be initiated at any time by any party to the agreement. Parties to the agreement must equally share arbitration costs.

Joel Lobb

Mortgage Broker – FHA, VA, USDA, KHC, Fannie Mae

EVO Mortgage • Helping Kentucky Homebuyers Since 2001

FHA | VA | USDA | KHC Down Payment Assistance | Fannie Mae

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval and program requirements.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

FHA has published the following guideline updates, which will be effective for all Kentucky FHA loans with case numbers assigned on or after September 9th

Specific verbiage for Well Water Testing has been added indicating that it must be performed by a disinterested party in a method acceptable to the local health authority. The borrower or any other interested party may not have contact with the sample. Additionally, cases mandating a Well Water Test have been added to include (but not limited to) the following

Newly constructed properties and/or wells

Properties with deficiencies in the well or well water as determined by an appraiser

Areas where water has been reported or is otherwise known to be unsafe

Properties located in close proximity to dumps, landfills, industrial sites, farms, or other sites that could contain hazardous waste

Properties where distance between well and septic systems is less than 100 feet

Average Overtime, Bonus, or Tip income earned over the previous 2 years (or if earned less than 2 years, the total length of time it has been received); OR

Average Overtime, Bonus, or Tip income earned over the previous year

All requirements regarding unreimbursed business expenses and Commission Income or Automobile Allowances has been completely removed to align with current IRS tax laws

Rent Below Fair Market has been defined as an inducement to purchase when the borrower is allowed to live in the property rent free or at a rental amount more than 10 percent under the fair market rent as determined by the appraiser.

Clarification has been added that Reduction in Term for Kentucky FHA Mortgage Streamline Refinances refers specifically to the reduction of the remaining amortization period of the existing mortgage.

FHA Guidelines For Bankruptcy, income, down payment, mortgage insurance, credit scores, work history for FHA loan

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

This web site is not the FHA, VA, USDA, HUD or any other government organization responsible for managing, insuring, regulating or issuing residential mortgage loans.

All approvals and rates are not guaranteed, and are only issued based on standard mortgage qualifying guidelines

Remember, we are even available this weekend for pre-qualifications or questions. Call our cell phone or email us. If you miss us, leave a message and we WILL call you back

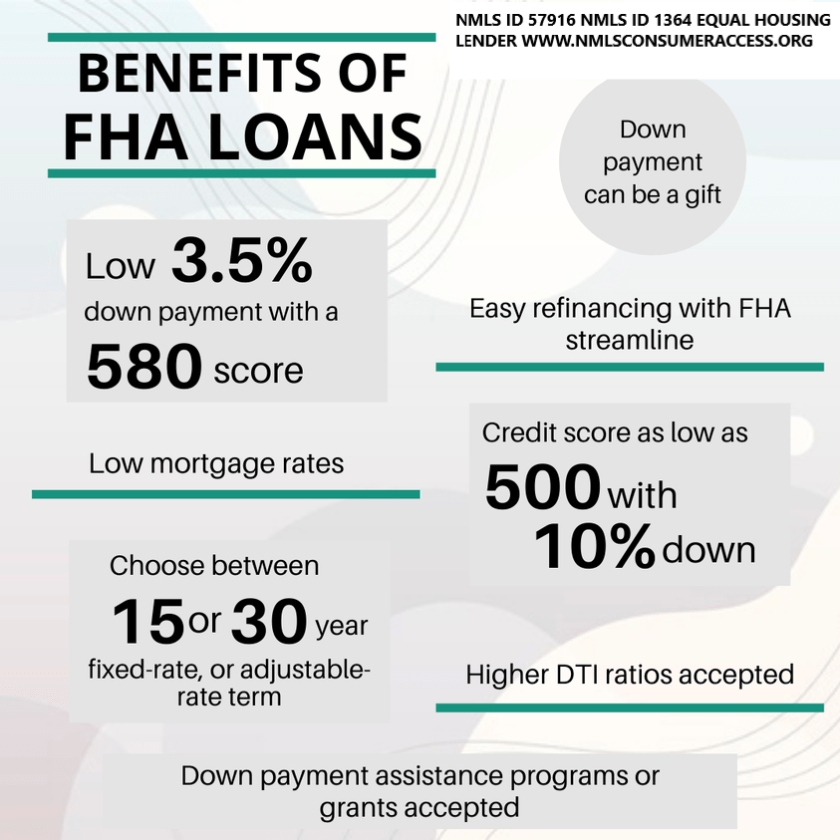

Here are some benefits of Kentucky FHA loans 🤩 ✅ Low down payment options ✅ Down payment assistance programs available ✅ Higher DTI ratios accepted

FHA requires you to establish that the income is in fact stable. I am covering Time on Job, Part Time Income, Seasonal Income and Job Gaps below.

Time on Job

There is not a minimum length of time a borrower must have held a position for the income to be eligible. However, the application must identify the most recent 2 years of employment.

If the borrower’s employment history indicates that they were in school or in the military, then the borrower must provide evidence supporting this such as college transcripts or discharge papers.

The current type of employment has to be supported by the college transcripts or discharge papers showing that he borrower’s training enabled them to gain employment in their field of training.

Part Time Income

Part-time and second job income can be used to qualify if documentation is obtained to prove that the borrower has worked the part-time job uninterrupted for the past two years, and plans to continue.

For Qualifying purposed, “part-time” income refers to jobs taken to supplement the borrower’s main income from regular employment, such as a second job that is less than 40 hours per week.

Income: Is averaged over the previous 2 years. If there was a pay rate increase and we can document the increase in pay, you can average the new pay rate over 12 months.

Seasonal Income

Seasonal income may be acceptable for qualifying. It is not unusual to have out-of-season income from unemployment income. If the borrower has a 2 year history and continuance is probable, this type of income may be allowed to qualify the borrower.

The key here is history and continuance.

Job Gaps

The borrower must provide a signed explanation for gaps in employment as follows:

Income can be considered effective if the following can be verified:

1. Borrower has been employed in the current job for at least six months at the time of the case number assignment AND

2. A two year work history prior to the absence from employment.

What does FHA stand for?

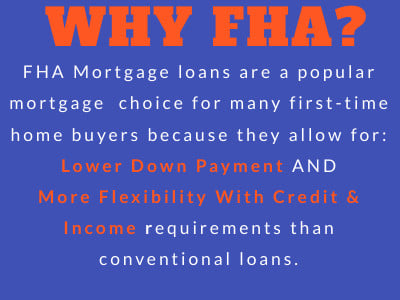

FHA stands for Federal Housing Administration, and the FHA is a government agency that insures mortgages. It was created just after the Great Depression, at a time when homeownership was prohibitively expensive and difficult to achieve because so many Americans lacked the savings and credit history to qualify for a loan. The government stepped in and began backing mortgages with more accessible terms. Approved lenders began funding FHA loans, which offered more reasonable down payment and credit score standards.

Today, government-backed mortgages still offer a safety net to lenders—because a federal entity (in this case, the FHA) is guaranteeing the loans, there’s less financial risk if a borrower defaults on their payments. Lenders are then able to loosen their qualifying guidelines, making mortgages available to middle and low income borrowers who might not otherwise be approved under conventional standards.

What’s the difference between FHA and conventional loans?

Home loans fall into two broad categories: government and conventional. A conventional loan is any mortgage that is not insured by a federal entity. Because private lenders assume all the risk in funding conventional loans, the requirements to qualify for these loans are more strict. Generally speaking, FHA loans might be a good fit if you have less money set aside to fund your down payment and/or you have a below-average credit score. While low down payment minimums and competitive interest rates are still possible with a conventional loan, you’ll need to show a strong credit score to qualify for those advantages.

Each loan type has advantages and disadvantages—including different mortgage insurance requirements, loan limits, and property appraisal guidelines—so choosing the one that works best for you really depends on your financial profile and your homebuying priorities.

FHA loans pros and cons

FHA loans are meant to make homeownership more accessible to people with fewer savings set aside and lower credit scores. They can be a great fit for some borrowers, particularly first time homebuyers who often need lower down payment options, but you should weigh the costs and benefits of any mortgage before committing. Here’s a breakdown of the key pros and cons when it comes to FHA loans:

Pros

Cons

Low down payment. Down payments make up the majority of cash to close in any purchase loan, and saving up for one can be a significant barrier for some borrowers. FHA loans make it possible to put down as little as 3.5% upfront and still get competitive rates.

Mandatory MIP payments. FHA loans are more lenient, but they also come with insurance costs to mitigate risk to the lender. You’ll have to pay Mortgage Insurance Premiums (MIP) no matter what—either for 11 years or for the life of your loan, depending on your down payment.

Lower credit score. Credit scores can be a major hurdle when it comes to conventional loans, but borrowers with credit scores starting at 500 can qualify for FHA loans.

Less competitive. Sometimes sellers can be more hesitant to accept FHA loans. In a competitive market, you might not win out against conventional loan bids.

Higher DTI accepted. Your debt-to-income (DTI) ratio gives lenders an understanding of other major financial obligations in your life. This ratio is a key factor in any loan application because it indicates your ability to afford a mortgage based on current household income and existing debt. Again, FHA loans offer more leniency here and borrowers at or below 43% DTI can qualify.

Stricter property standards. To offset risk and further protect lenders, FHA loans have strict criteria when it comes to assessing the condition of any property being purchased with an FHA loan. The downside? The house you want to buy might not qualify for an FHA loan. The upside? You’re less likely to be financially burdened by a home that requires expensive repairs or updates.

No income limitations. It’s a common misconception that FHA loans are only available to first-time homebuyers or borrowers with limited income—but they’re not. There’s no maximum income limit that would disqualify you from this type of loan.

Loan limits: FHA loan limits are typically lower than conventional loan limits, which means you might not be able to get funding for more expensive houses. This isn’t necessarily a bad thing, since it helps ensure that borrowers get loans they can afford to repay.

How to qualify for an FHA loan

Qualifying for an FHA loan is generally easier than qualifying for a conventional loan, but you’ll still need to meet some basic minimum standards set by the FHA. While the government insures these loans, the funding itself comes through FHA-approved lenders each lending institution may have slightly different qualifying guidelines for its borrowers. Keep in mind that, while these FHA standards offer a basic framework, you’ll need to confirm the individual qualifying rules with your specific lender.

Credit score minimum 500. Your exact credit score will play a big role in determining your down payment minimum; typically, the higher your credit score, the lower your down payment and the more favorable your interest rate.

Debt-to-income ratio at or below 56.9%. DTI is a standard way of comparing the amount of money you earn to the amount you spend paying off other debts, and FHA loans are more lax on this number.

Steady income and proof of employment. Being able to provide at least 2 years of income and employment records is a standard requirement for all loans.

Down payment between 3.5%-10%. The down payment minimum for an FHA loan is typically lower than conventional loan, and can be as little as 3.5% depending on your credit score and lender.

Property standards apply. You won’t qualify for an FHA loan if the house you want to buy doesn’t pass the appraisal process, which is more strict with this type of loan than conventional mortgages.

Maximum FHA loan amount. The amount of money you borrow cannot exceed the FHA loan limits; this number changes based on your county and is determined by how expensive the local market is; the maximum FHA loan limit in 2021 is $420,000 (check HUD resources to confirm the latest limits.)

Joel Lobb Senior Loan Officer (NMLS#57916)

American Mortgage Solutions, Inc. 10602 Timberwood Circle, Suite 3 Louisville, KY 40223

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency.

The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (http://www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky. All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.

Joel E Lobb American Mortgage 5029053708 email us here

Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.

The FHA is actually not the lender. They insure the loans that are issued by FHA-approved lenders. FHA loans are gear more toward borrower’s with less than 20% down payment and credit issues in the past.

Qualifying for a FHA Loan Mortgage In Kentucky

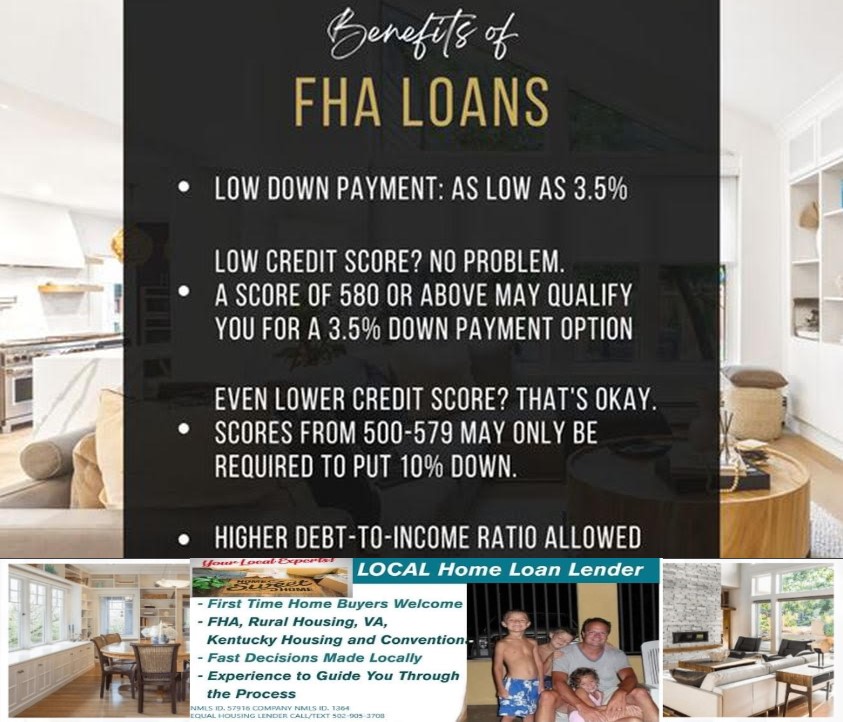

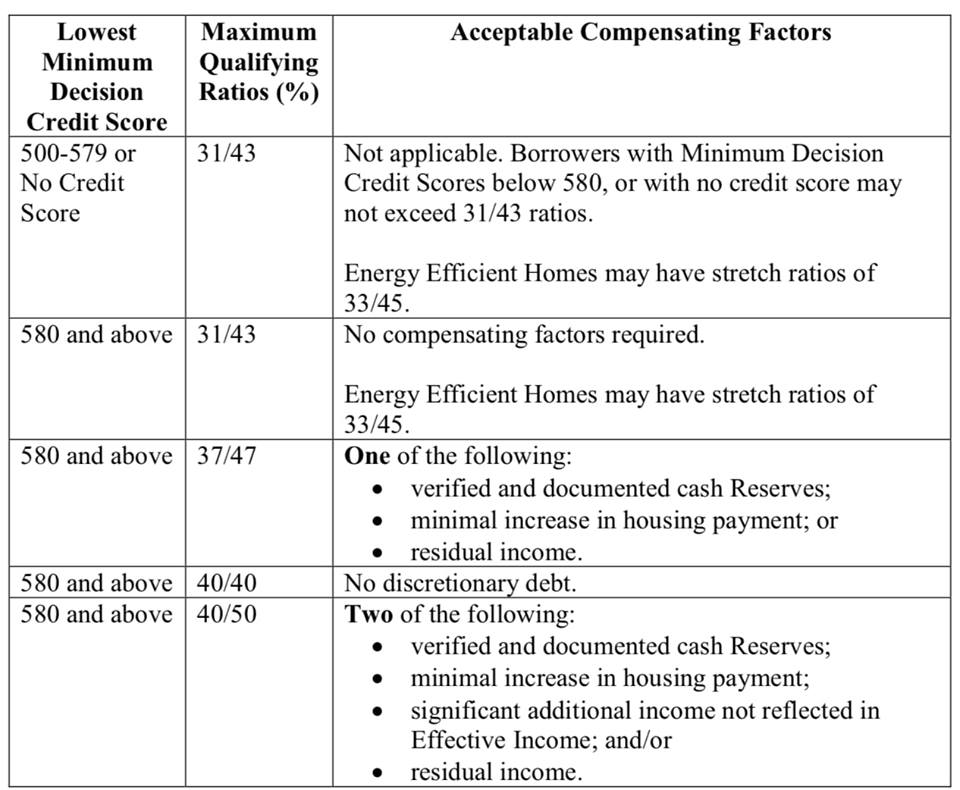

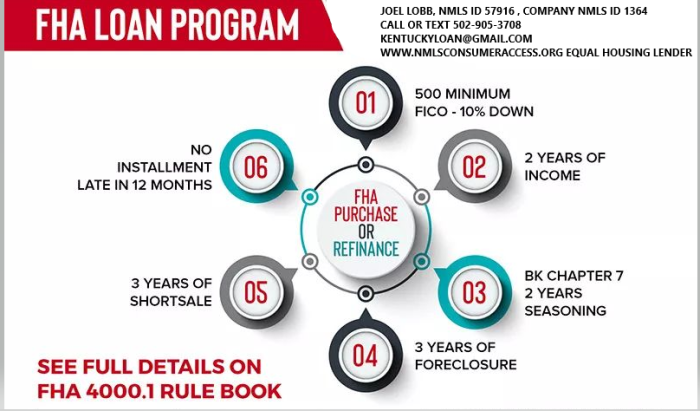

Credit Scores and Down Payment Percentages – Each year, the rules for qualifying for these loans changes. For 2020, applicants need a minimum credit score of 580 in order to get the low down payment, which is 3.5 percent.

For those whose credit score is less than 580, they will have to come up with 10 percent for their down payment. This does not guaranteed a mortgage loan approval if you have the certain credit scores, just a the minimum required.

Compensating Factors for FHA loan Approval

The credit score is just one part of the story. The FHA will also evaluate the borrower’s bankruptcies, foreclosures, prior payment history on other debts. They will also want information on difficulties that kept the borrower from making payments on other debts in the past.

Negative strikes against qualifying for the loan include not having any credit history or a bankruptcy.

Someone with a bankruptcy will have to wait for two or more years after their bankruptcy before applying for an FHA-insured loan.

If you have late payments on debt obligations, it is best to wait until you have had a full year of on-time payments before you apply for a FHA-insured loan.

If you have had a foreclosure in the past, you may still be able to get a FHA-insured loan three years after your foreclosure. The lender will be looking at the circumstances behind the foreclosure.

If you have had any civil judgement against you for money owed, collections actions or unpaid/unresolved federal debt, the FHA-approved lender will be required by the FHA to establish that all of these outstanding issues are resolved or paid before you can go through closing.

Watch out for student loans if they are delinquent because sometime this can cause a lien against you in the form of a CAVIRS Alert with HUD

As you can see, many types of borrowers who would not be eligible for a traditional mortgage, or who would face exorbitant interest rates, will be able to qualify for a FHA-insured loan at attractive interest rates.

Your income has to be verifiable in some way, whether that be through pay stubs, your income tax returns. No bank statements or cash deposits , or undocumented income can be used for income qualifying purposes.

Debt-to-Income Ratio Requirements –

Depending on the automated underwriting system from Desktop Originator, your Debt-to-income ratio is the percentage of your income before taxes that you spend on monthly debt.

Taking into account the proposed mortgage payment as well as the other debts, the FHA requires that these debts all total less than 43 percent of your pretax income in order to qualify for the loan.

If your debt load is too high, you will struggle to pay all of your bills and mortgage expenses and care for yourself and your family.

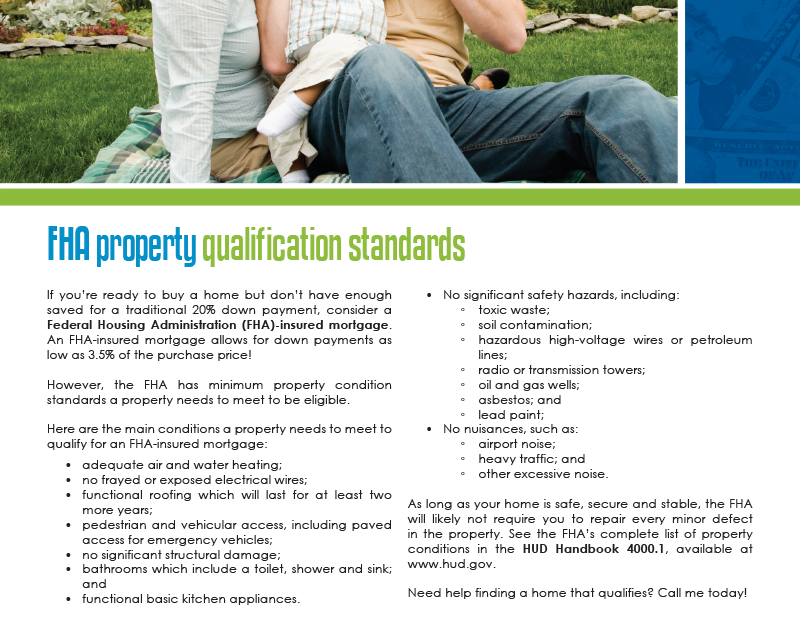

Property Requirements for a Kentucky FHA Loan

It must be the place where you intend to reside. You must move into the home within 60 days of closing the loan. The home cannot be an investment. There will be an inspection to ensure that the home is safe and habitable.

It is really not too hard to pass FHA loans and the appraisal process.

Pros of FHA Loans –

New homebuyers and those who have lower credit scores or who have other blemishes on their credit history will often qualify for FHA-insured loans.

Even though these borrowers are considered “subprime” to a traditional lender, they will receive attractive interest rates through the FHA-insured mortgage programs.

The down payments required from borrowers are lower than those required by traditional mortgage lenders.

These loans can be combined with other forms of public assistance for lower income or new borrowers so that the borrower will not need to come up with a down payment of any kind.

Cons of FHA Loans –

Since the FHA is not actually the lender, and you have to go through FHA-approved lenders, you may not qualify due to stricter standards that the lender has for the loan.

Because you are not paying 20 percent as a down payment, the FHA requires two mortgage insurance premiums to be paid. One is an upfront premium that is 1.75 percent of the loan amount. Lenders often will allow you to make that mortgage insurance premium a part of your loan. The second is an annual mortgage insurance premium that is .45 percent or 1.05 percent. This premium is paid monthly.

What credit score do I need to qualify for a Kentucky FHA loan is one of the most common questions I hear from Kentucky homebuyers?

The short answer is you must have a minimum credit score of 500 to be eligible for an FHA loan in Kentucky. Anything lower than 500 disqualifies you from consideration for an FHA loan.

There are two sets of credit score requirements for a Kentucky FHA Loan

One important thing to understand is that the Federal Housing Administration (FHA) does not lend money directly to home buyers. You will fill out an application with a regular lender just as you would if you were applying for any other type of mortgage. What the FHA does is ensure your loan to help protect the lender in case you default.

You will be required not only to meet the FHA guidelines to qualify for a loan but also meet any additional qualifications required by the lender. This means there are two sets of requirements you have to meet with your credit score.

1. The first set of requirements comes from the Department of Housing and Urban Development (HUD). HUD oversees the FHA and determines what a borrower’s minimum eligibility requirements will be to obtain an FHA loan.

2. The second set of requirements comes from the mortgage lender. The mortgage lender has the right to add its requirements to those mandated by HUD.

What HUD requires of borrowers to be eligible for an FHA loan

The HUD Handbook 4000.1 includes the official guidelines when it comes to the FHA mortgage insurance program.

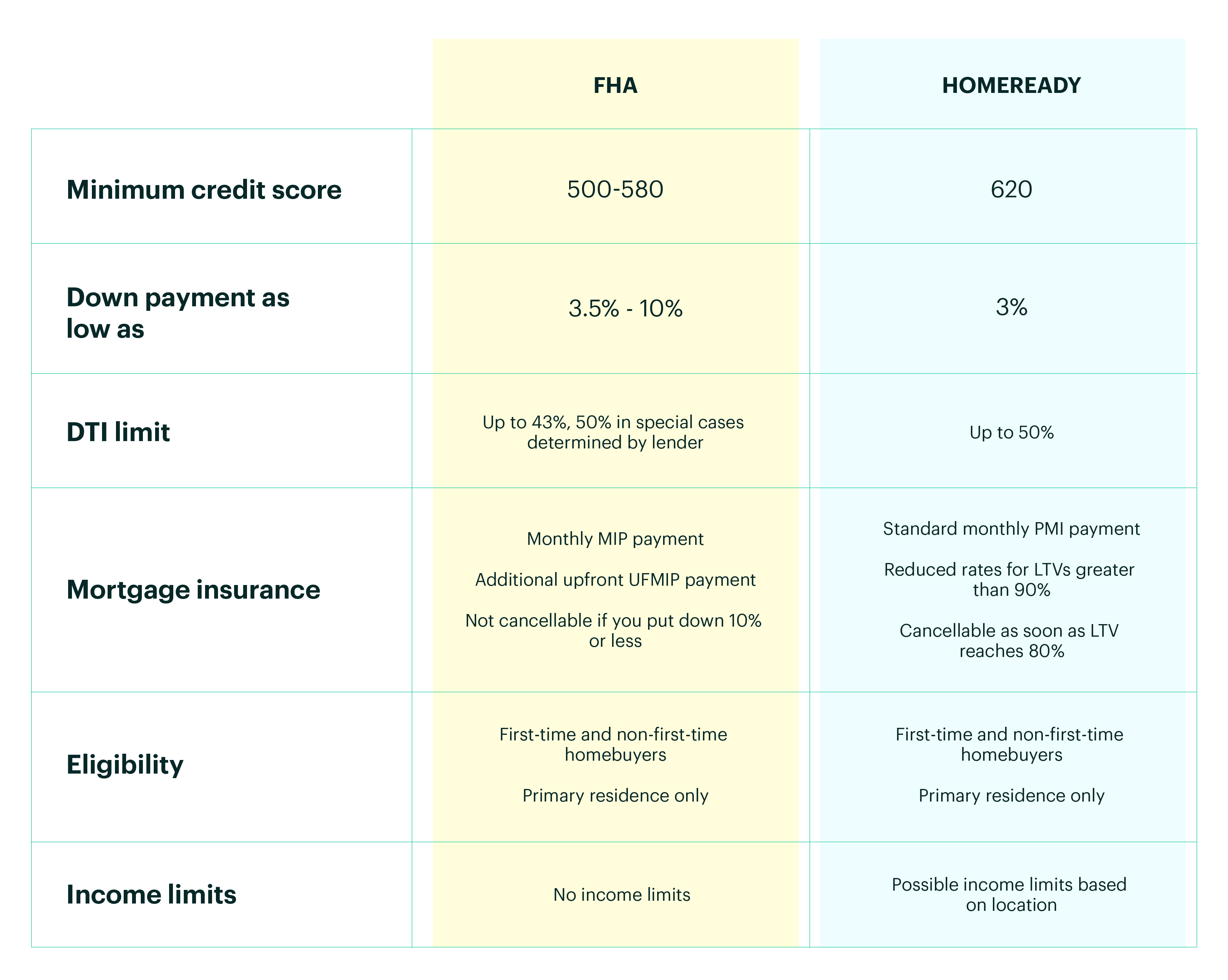

It states that in 2020 the Kentucky FHA borrowers with credit scores of 580 or higher are eligible for a 96.5% loan with 3.5% down.

Borrowers with credit scores from 500 to 579 are eligible for a 90% loan with 10% down.

Individuals with credit scores below 500 are not eligible for the FHA program.

What lenders may require of borrowers to be eligible for an Kentucky FHA loan

Lenders have the right to add requirements over and above the minimum requirements of HUD. These additional requirements are called overlays. Your lender may or may not require them.

This is not something that should come as a surprise to you, however. Requiring a credit score of 580 to 620 is not unusual. In addition to your credit score, you must have a manageable debt level that lenders are comfortable with and enough income to repay your loan.

What credit score do I need to qualify for FHA loan?

Each month Ellie Mae, the software company processing more than ⅓ of America’s mortgage loans, publishes an insight report for mortgage trends and standards. One of the things they track is average credit scores. The following is their report for November 2019 which shows what percentage of successful borrowers fall into what credit score ranges.

These percentages show that the majority of borrowers who successfully qualify for FHA loans fall into the 600 to 799 range. While it is true that some successfully qualify in the low range of 500 to 599, you have a much better chance of being approved for a loan with good terms and a low down payment if you fall into the higher range.

For your free credit report and analysis call us today at 502-905-3708 or email us at kentuckyloan@gmail.com

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

Kentucky FHA loan is a mortgage that is insured by the Government agency under Housing and Urban Development that is called FHA or short for Federal Housing Administration. The loan was established for Kentucky Home buyers will very little or no money down home loans with more lenient credit score and income requirements and tends to be more forgiving about credit history with regard to bankruptcy and foreclosures, higher debt to income ratios and job history with limited work history for home buyers will only 2 years work history or less.

The Kentucky FHA home loan program may accept credit scores as low as 580 and require at least a 3.5 percent down payment of the sales price on a purchase. If you have a credit score below 580, then a 10 percent down payment or more may be acceptable some FHA lenders in Kentucky , providing you meet all program guidelines in regards to debt to income ratios, assets, and income requirements . The loan cannot be used for rental properties and does allow for co-signers if they are related.

Remember, these guidelines are set forth by FHA and all lenders do not have to offer these guidelines, to whereas they may a higher credit score or more money down or income restrictions on how much you can qualify for.

In case you had a blemish on your credit report with a bankruptcy, short sale or foreclosure, follow these guidelines.

Kentucky FHA loans requires a passage of two years since the discharge date of a chapter 7 bankruptcy. A chapter 13 bankruptcy may be acceptable after at least 12 months of an on time pay-back period and the borrower has received permission from bankruptcy court to enter the mortgage transaction, and you qualify with the new house payment along with other debts on the credit report.

Three years must pass if you went through a short sale or foreclosure. The date starts when the home was sold, not when you entered the transaction toward foreclosure or short sale period. Sometimes the house will not sell to 1-2 years later after the foreclosure and this is when the passage date starts. Keep this in mind on your next FHA loan pre-approval if you have had a bankruptcy or foreclosure in the past.

FHA loans have two forms of mortgage insurance which protects the lender for any losses suffered if the borrower defaults on the payment. ne is called upfront mortgage insurance premium (UFMIP) which has a rate of 1.75% of the loan amount. The fee can be added to the loan amount or paid in full as part of your closing costs. In addition, FHA loans also have a 0.8-0.85% (of the loan amount) monthly mortgage insurance. In most cases, this mortgage insurance remains for the life of the loan. To eliminate the mortgage insurance, the borrower must refinance the loan into a non-FHA loan program and have 20% equity in the property.

In addition to the down payment requirements on a FHA loan, they’re closing costs and prepaids to pay at closing. The seller can contribute up to 6% of the sales price to help the buyer with closing costs and prepaid expenses. Closing costs vary from lender to lender and your prepaids would be the same no matter which lender you choose because this is a function of the property ‘s home insurance premium quote you obtain and the property tax bill on the home set by PVA.

Sometimes the lender can pay a credit toward these expenses at closing with a lender credit which lets the lender credit back to you with a higher rate to reduce the costs of the loan’s costs at closing for out of pocket expenses.

All Kentucky FHA loans are assumable, which means that when the homeowner sells a home, the buyer may be able to take on the existing loan and terms (e.g.: balance, rate and remaining loan amount). Of course, anyone interested in the assumable loan feature must go through the approval process (credit check, income verification) with the current lender on the property. This is a very rare occurrence because most sellers are going to sell the home for more than they owe on it.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

FHA stands for the Federal Housing Administration which is a government agency created to increase home-ownership across the United States all the way back in 1934. The agency itself doesn’t offer home loans but insures loan that are offered by private lenders (i.e. mortgage companies).

It’s important to understand the different types of loan programs available to you and what benefits and drawbacks there are to each type.

For example, if you’re looking to find a fixer upper this may not be the right loan program for you. But an FHA loan may be a better fit for you if you have little cash saved up for a down payment or if you don’t have a high credit score.

No age limit. just must be 18 years of age to apply.

Must occupy the home as a primary residence, no rental homes or investment property

An appraisal must be done by an FHA-approved appraiser.Typically FHA appraisal in Kentucky costs anywhere from low-end $325 to $525 with most FHA lenders in KY.

Home inspection is not required

Termite inspection not required

2 years removed from Chapter 7 bankruptcy, and 1 year in Chapter 13 bankruptcy is possible to get a loan while in bankruptcy

Foreclosure or short sale on previous home mortgage requires 3 years removal from those dates.

Mortgage insurance (MIP) is required

Upfront Mortgage Insurance Premium is 1.75% and monthly mortgage insurance is .85% or .80% depending on loan term and loan to value.

Mortgage insurance is for life of loan.

No matter your credit scores, everyone pays the same mortgage insurance premiums.

Must have 2 years of employment history proving a reliable source of income

500 FICO score requirement with at least 10% down payment

580 FICO score requirement with at least 3.5% down payment

Gifts and down payment assistance programs are allowed to meet your down payment requirements. Cannot come from seller, but seller can contribute up to 6% of the sales price toward buyer’s closing costs and prepaids.

Student loan payments are factored into the debt-to-income ratio when applying. Typically if loans are deferred, or in an income=based repayment plan, the FHA underwriters will use 1% of the outstanding balance, which sometimes can make it difficult to qualify.

Your debt-to-income ratio must not be higher than 31% or total debt obligation cannot be higher than 43% of your current income. This is for a manual underwriter, meaning that if the AUS underwriting system by mortgage lenders will approve you for a higher debt to income ratio, that is fine.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204