|

|

|

|

What are the requirements to qualify for a Kentucky FHA Mortgage in 2020?

Kentucky FHA loan is a mortgage that is insured by the Government agency under Housing and Urban Development that is called FHA or short for Federal Housing Administration. The loan was established for Kentucky Home buyers will very little or no money down home loans with more lenient credit score and income requirements and tends to be more forgiving about credit history with regard to bankruptcy and foreclosures, higher debt to income ratios and job history with limited work history for home buyers will only 2 years work history or less.

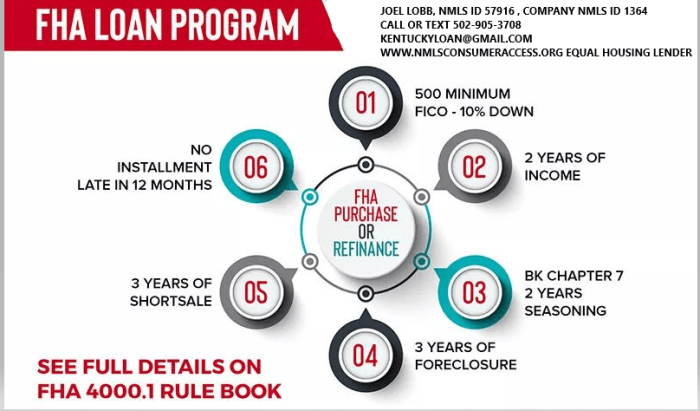

Kentucky FHA Credit Score Requirements and Down Payment Requirements

The Kentucky FHA home loan program may accept credit scores as low as 580 and require at least a 3.5 percent down payment of the sales price on a purchase. If you have a credit score below 580, then a 10 percent down payment or more may be acceptable some FHA lenders in Kentucky , providing you meet all program guidelines in regards to debt to income ratios, assets, and income requirements . The loan cannot be used for rental properties and does allow for co-signers if they are related.

Remember, these guidelines are set forth by FHA and all lenders do not have to offer these guidelines, to whereas they may a higher credit score or more money down or income restrictions on how much you can qualify for.

Kentucky FHA Mortgage Loans and Bankruptcy or Foreclosure

In case you had a blemish on your credit report with a bankruptcy, short sale or foreclosure, follow these guidelines.

Kentucky FHA loans requires a passage of two years since the discharge date of a chapter 7 bankruptcy. A chapter 13 bankruptcy may be acceptable after at least 12 months of an on time pay-back period and the borrower has received permission from bankruptcy court to enter the mortgage transaction, and you qualify with the new house payment along with other debts on the credit report.

Three years must pass if you went through a short sale or foreclosure. The date starts when the home was sold, not when you entered the transaction toward foreclosure or short sale period. Sometimes the house will not sell to 1-2 years later after the foreclosure and this is when the passage date starts. Keep this in mind on your next FHA loan pre-approval if you have had a bankruptcy or foreclosure in the past.

Kentucky FHA Loans and Mortgage Insurance

FHA loans have two forms of mortgage insurance which protects the lender for any losses suffered if the borrower defaults on the payment. ne is called upfront mortgage insurance premium (UFMIP) which has a rate of 1.75% of the loan amount. The fee can be added to the loan amount or paid in full as part of your closing costs. In addition, FHA loans also have a 0.8-0.85% (of the loan amount) monthly mortgage insurance. In most cases, this mortgage insurance remains for the life of the loan. To eliminate the mortgage insurance, the borrower must refinance the loan into a non-FHA loan program and have 20% equity in the property.

In addition to the down payment requirements on a FHA loan, they’re closing costs and prepaids to pay at closing. The seller can contribute up to 6% of the sales price to help the buyer with closing costs and prepaid expenses. Closing costs vary from lender to lender and your prepaids would be the same no matter which lender you choose because this is a function of the property ‘s home insurance premium quote you obtain and the property tax bill on the home set by PVA.

Sometimes the lender can pay a credit toward these expenses at closing with a lender credit which lets the lender credit back to you with a higher rate to reduce the costs of the loan’s costs at closing for out of pocket expenses.

All Kentucky FHA loans are assumable, which means that when the homeowner sells a home, the buyer may be able to take on the existing loan and terms (e.g.: balance, rate and remaining loan amount). Of course, anyone interested in the assumable loan feature must go through the approval process (credit check, income verification) with the current lender on the property. This is a very rare occurrence because most sellers are going to sell the home for more than they owe on it.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

|

FHA Loans in Kentucky – Gifts to Pay off Debt Do you know that a gift can be used to pay off Borrower’s debts to qualify on an Kentucky FHA Loan? A regular gift (this does not include a gift of equity) may be used to pay off a Borrower’s debt(s) for qualifying purposes as long as both the gift funds and the debt(s) being paid off with the gift funds are accurately disclosed and assessed by AUS TOTAL Scorecard. Whenever a gift is received on an Kentucky FHA loan, regardless of what it is being used for, it carries certain risks that must be assessed by TOTAL Scorecard for qualifying purposes. When a gift is received to pay off debt(s), follow the steps below to ensure that TOTAL Scorecard accurately assesses the risk of using gift funds in paying off debt for qualifying:

|

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

2018 KENTUCKY FHA MORTGAGE GUIDELINES FOR APPROVAL WITH STUDENT LOANS

Student Loan Payment Calculation

Must include all student loans in the borrower’s liabilities, regardless of the payment type or status of payments.

Calculation of monthly obligation, regardless of the payment status, must use either:

the greater of:

• 1 percent of the outstanding balance on the loan; or

• the monthly payment reported on the borrower’s credit report; or

the actual documented payment, provided the payment will fully amortize the loan over its term.

Additional documentation required if the payment used for the monthly obligation is:

• less than 1 percent of the outstanding balance reported on the borrower’s credit report;and

• less than the monthly payment reported on the borrower’s credit report.

Provide written documentation of the actual monthly payment, the payment status, and evidence of the outstanding balance and terms from the creditor.

Guide Reference – 4000.1 II.A.4.b.iv(H) (TOTAL) and II.A.5.a.iv.(G) (Manual)

I can answer your questions and usually get you pre-approved the same day.

Call or Text me at 502-905-3708 with your mortgage questions.

Email Kentuckyloan@gmail.com

Text/call 502-905-3708

kentuckyloan@gmail.com

|

Kentucky FHA Loan Limits for 2019

FHA has announced new loan limits for 2019. For all FHA loans with Case Numbers assigned on or after January 1st, the following will be effective

these values are updated to coincide with the new FNMA loan limit floor values.

|

FHA mortgage lending limits in KENTUCKY vary based on a variety of housing types and the cost of local housing. FHA loans are designed for borrowers who are unable to make large down payments.

That is an increase from 2018 when the limit was set at $294,515.

Text/call 502-905-3708

kentuckyloan@gmail.com

FHA Handbook 4000.1 Updates

Administration (FHA) Single Family Housing Policy Handbook 4000.1. These updates are effective September 30, 2016 and

Clarification that an Upfront Mortgage Insurance Premium (UFMIP) refund calculation applies even if original UFMIP was

not financed.

Mortgage Debt Not Included in Credit Report: Clarification that a manual downgrade is not required when there is no history of late payments, as detailed below.

o Not currently delinquent; and

o No 30 day late payments within 12 months of the case number assignment date; and

o No more than 2 x 30 day late payments within 24 months of the case number assignment date.

A link has been added in the FHA Product Description from Mortgage Payment History requirements to “Credit History

Requirements for Manually Underwritten Loans.”

Appliances that add contributory value must be operable.

Mechanical components and utilities: The appraiser must report the utility, safety, and capacity of the mechanical systems.

The appraiser must observe and operate all applicable mechanical systems and utilities. In conjunction with this guidance,

existing FHA Handbook guidance on the following topics will be added:

o Electrical System

o Heating and Cooling

o Plumbing

o Utilities

Here is what you need to know: When someone’s Louisville Kentucky FHA loan goes into foreclosure, that home becomes a HUD home. HUD becomes the owner of the home and offers the home for sale to recover the loss on the foreclosure. This can create a big opportunity for Louisville Kentucky First Time Home Buyers, because HUD will allow you to obtain an FHA loanand instead of 3.5% down, you only have to put $100 down.

Other things to consider:

So you’re asking how do I find these homes. As mentioned, only certain homes are available for the $100 down HUD program, so you need a Realtor that is knowledgeable about the program and has access to the bidding process. The bidding process can be overwhelming unless you are working with the right people. Call me today to get pre-approved and I can refer you to a Realtor in your area that can get you a home, with only $100 down.

Kentucky FHA loans are great loan program that is not just for first-time buyers!

Kentucky FHA loans are great loan program that is not just for first-time buyers!