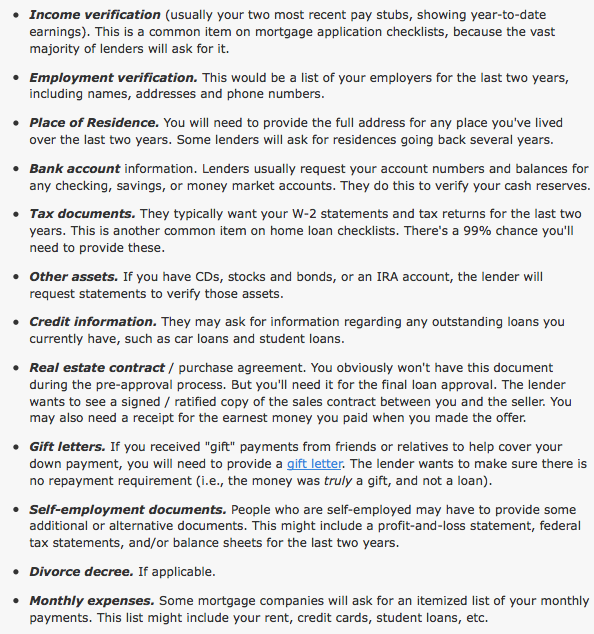

Here is a brief summary on getting a mortgage loan while in a Chapter 13 Bankruptcy:

You must have 12 payments paid into the Chapter 13 before you can apply for a mortgage loan.

The payments must be made on time for last 12 months or after 12 months if you have been in longer, so no late payments to the Chapter 13 while in it.

You have to ask permission from the courts to seek a mortgage loan. They usually grants this. I have never not seen them grant it.

You have to qualify with the new house payment along with Chapter 13 payments and other debts listed on credit report. Debt to income ratios usually center around 31 and 43% respectively, meaning the new house payment should not be more than 31% of your gross monthly income and your total house payment and debts listed on credit report along with Chapter 13 payment should not be more than 43% of your total gross monthly income.

Credit scores: Most FHA lenders I work with will want a 620 middle score. You have three fico scores from Experian, Equifax, and Transunion, and they throw out the high and low score and take middle score. For example, if you had a 598, 679, and 590 scores respectively for all three bureaus listed above, your qualifying score would be 598.

There are some FHA investors that I am set up with that will go down to 580, but I have seen in my past experiences 620 will get you a better deal and far greater chance of closing on your loan with FHA.

Down payment: For FHA loans, you will need to have at least 3.5% down payment saved up. It is extremely hard to find a no money down loan program to get you approved for a mortgage while you are in a Chapter 13 plan.

FHA and USDA are really the only two options that I know of that offer financing for a borrower with a current Chapter 13 Bankruptcy plan plan, so keep that in mind.

Conventional loan program offered by Fannie Mae will not allow a mortgage loan for someone in a Chapter 13 Bankruptcy plan.

On USDA loans, it is possible to get 100% Financing after you have paid into the plan for 12 months with a good pay history. The credit scores needed for a USDA loan approval really need to be above 640 in my past experience in getting them approved. A lot of USDA lenders will say they will do down to 620, but it is very difficult getting them approved. Best to get your scores up to increase your changes in qualifying for a USDA loan. There is not much that difference in getting your scores up to that range if you are at a 620 score now.

With USDA loans, they have income and property eligibility requirements that FHA does not have, so below is a rough run down of FHA vs USDA loan for you:

Typically, USDA-eligible properties are located in rural areas. It is a mistake, however, to think that you have to live far out in the country to qualify for a USDA loan. USDA-eligible properties are often located near urban areas.

A property’s eligibility is determined by its location with respect to USDA’s map of eligible locations. The USDA program also places limits on your household income based on median earnings in an area. If you exceed that limit, you can’t obtain a USDA loan.

The FHA, by contrast, does not place limits on household earnings. The FHA, however, does establish a maximum limit on the amount of money that can be borrowed through the program.

So if you were in a hurry to buy, after you have been in your Chapter 13 plan for 12 months, I can look at getting you approved to buy a home if you wish:

How to Get Approved for a Kentucky Mortgage While in A Chapter 13 Bankruptcy:

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

This web site is not the FHA, VA, USDA, HUD or any other government organization responsible for managing, insuring, regulating or issuing residential mortgage loans.

All approvals and rates are not guaranteed, and are only issued based on standard mortgage qualifying guidelines

Remember, we are even available this weekend for pre-qualifications or questions. Call our cell phone or email us. If you miss us, leave a message and we WILL call you back

Chapter 13 bankruptcy can impact your ability to qualify for various mortgage loan programs like FHA, VA, USDA, and Fannie Mae.

Chapter 13 bankruptcy can impact your ability to qualify for various mortgage loan programs like FHA, VA, USDA, and Fannie Mae. Here are the details for each program regarding waiting times, credit score requirements, down payment, and qualification criteria after a Chapter 13 bankruptcy:

FHA Loan after Chapter 13 Bankruptcy:

Waiting Time: Typically, you’ll need to wait at least two years after the discharge date of your Chapter 13 bankruptcy before applying for an FHA loan.

Credit Score: FHA loans are known for their flexibility with credit scores. While there’s no specific minimum score, a higher score (usually around 580 or above) can help you qualify for better terms.

Down Payment: The down payment requirement for an FHA loan after Chapter 13 bankruptcy is relatively low, usually starting at 3.5% of the purchase price.

Qualification with Chapter 13 Bankruptcy: To qualify, you must demonstrate that you’ve made all Chapter 13 payments on time for at least one year and receive approval from the bankruptcy court to take on new debt.

VA Loan after Chapter 13 Bankruptcy:

Waiting Time: The waiting time for a VA loan after Chapter 13 bankruptcy is generally two years from the discharge date.

Credit Score: VA loans also have flexible credit score requirements, with many lenders looking for scores around 620 or higher.

Down Payment: VA loans are known for offering zero-down financing, but eligibility depends on your military service record and whether you’ve used your VA loan benefits before.

Qualification with Chapter 13 Bankruptcy: Similar to FHA, you’ll need to demonstrate a consistent payment history under your Chapter 13 plan and receive approval from the bankruptcy court.

USDA Loan after Chapter 13 Bankruptcy:

Waiting Time: USDA loans typically require a waiting period of three years from the discharge date of your Chapter 13 bankruptcy.

Credit Score: While there’s no official minimum credit score, most lenders look for scores of 640 or higher for USDA loans.

Down Payment: USDA loans offer low to no down payment options, making them attractive for eligible borrowers in rural areas.

Qualification with Chapter 13 Bankruptcy: You’ll need to show that you’ve been making timely payments under your Chapter 13 plan for at least one year and obtain approval from the bankruptcy court.

Fannie Mae Loan after Chapter 13 Bankruptcy:

Waiting Time: Fannie Mae typically requires a waiting period of two years from the discharge date of your Chapter 13 bankruptcy.

Credit Score: Fannie Mae loans often have stricter credit score requirements compared to FHA, VA, and USDA loans. A score of around 620 or higher is generally needed.

Down Payment: Down payment requirements vary based on the type of Fannie Mae loan you apply for, but they can range from 3% to 20%.

Qualification with Chapter 13 Bankruptcy: You’ll need to demonstrate responsible financial management after bankruptcy, including rebuilding your credit and showing a stable income.

In all cases, it’s essential to work with a knowledgeable mortgage broker like Joel Lobb, who can guide you through the specific requirements and help you navigate the loan application process after a Chapter 13 bankruptcy.

Joel Lobb Mortgage Loan Officer NMLS 57916

EVO Mortgage 911 Barret Ave, Louisville, KY 40204 Company NMLS ID # 173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

Types of Kentucky Mortgage Loans to Consider After Bankruptcy

If you want to try to get a Kentucky mortgage after bankruptcy, you can research a number of different types of loans. Each mortgage loan has its own unique requirements for bankruptcy filers.

Kentucky FHA Loans

Federal Housing Administration (FHA) loans are managed by the federal government and may allow you to buy a house with a down payment that’s as little as 3.5% of the purchase price. The downfall of FHA loans, however, is that you’ll have to pay for mortgage insurance, which will result in higher monthly payments.

To get a mortgage after bankruptcy using an FHA loan, you’ll have to adhere to these waiting periods:

Chapter 7: Two years from your discharge date

Chapter 11: No waiting period

Chapter 13: One year from your discharge date

Kentucky USDA Loans

U.S. Department of Agriculture (USDA) loans are designed for rural borrowers who meet certain income requirements. It may be a good option if you’d like to buy a house in a rural area, have a low or modest income, and aren’t eligible for a conventional loan. If you go this route, you may not have to put any money down and you may be able to secure a low interest rate.

If you’re a veteran or currently serving in the military, you may be eligible for a Department of Veterans Affairs (VA) loan. A VA loan doesn’t require a down payment or charge private mortgage insurance and can give you the chance to lock in a low interest rate. If you pursue a VA loan, however, you’ll have to pay a funding fee, which will be a percentage of your home price.

Here are the waiting requirements you should be aware of if you’d like to get a VA loan after bankruptcy:

Chapter 7: Two years from your discharge date

Chapter 11: No waiting period

Chapter 13: One year from your discharge date

Kentucky Conventional Loans

Since conventional loans are not guaranteed or insured by government agencies, you can expect stricter requirements, such as having a good credit score, if you apply for one. If you get a conventional loan and put down less than 20% of the cost of your new home, you’ll need to pay private mortgage insurance.

The waiting requirements for taking out a conventional loan after bankruptcy are as follows:

Chapter 7: Four years from your discharge date

Chapter 11: Four years from your discharge date

Chapter 13: Two years from your discharge date or four years from your dismissal date

Chapter 7 Bankruptcy

A four-year waiting period is required, measured from the discharge or dismissal date of the bankruptcy action until the application date.

Chapter 13 Bankruptcy two years from the discharge date to the application date, or four years from the dismissal date to the application date.

The shorter waiting period based on the discharge date recognizes that borrowers have already met a portion of the waiting period within the time needed for the successful completion of a Chapter 13 plan and subsequent discharge.

A borrower who was unable to complete the Chapter 13 plan and received a dismissal will be held to a four-year waiting period.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted after a Chapter 13 dismissal, if extenuating circumstances can be documented. There are no exceptions permitted to the two-year waiting period after a Chapter 13 discharge.

Foreclosure / Short Sale

A seven-year waiting period is required. In all instances, the “date of foreclosure” is considered the date of the foreclosure deed. The end date of the waiting period is the application date.

Foreclosure / Short Sale – Extenuating Circumstance A three-year waiting period is permitted if extenuating circumstances can be documented. Additional requirements apply between three and seven years, which include:

FHA Loan Guidelines for Bankruptcy and Foreclosure

Chapter 7

Chapter 7 bankruptcy discharged more than 24 months prior to the application date may be allowed.

Chapter 7 bankruptcy discharged between 12 and 24 months prior to the application date requires satisfactorily established credit and documentation showing the circumstances which caused the bankruptcy were beyond the borrower’s control (i.e. unemployment, medical bills not covered by insurance). In these instances, the file must be manually downgraded to a refer and manually underwritten. It falls upon the underwriter to make a final determination as to the overall quality of the file.

Chapter 7 bankruptcy discharged less than 12 months prior to the application date is not allowed.

Chapter 13

Loans where the borrower is currently in a Chapter 13 bankruptcy or had a Chapter 13 bankruptcy which was discharged within the previous 2 years require manual downgrade and must be underwritten manually. Note that manual underwrites require Underwriting Management approval.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for FHA financing provided all of the following conditions are met in addition to standard manual underwriting requirements:

Foreclosure / Short Sale

A foreclosure less than 3 years ago is not allowed.

In all instances, the “date of foreclosure” is considered the date of the foreclosure deed. The end date of the time frame is determined by the application date.

Kentucky VA Loan Guidelines for Bankruptcy and Foreclosure

Chapter 7

Chapter 7 bankruptcy discharged more than 24 months prior to application date may be disregarded.

Chapter 7 bankruptcy discharged between 12 and 24 months prior to application date requires satisfactorily established credit and documentation showing the circumstances which caused the bankruptcy were beyond the borrower’s control (i.e. unemployment, medical bills not covered by insurance). In these instances, the file must be manually downgraded to a refer and manually underwritten. It falls upon the underwriter to make a final determination as to the overall quality of the file.

Chapter 7 bankruptcy discharged less than 12 months prior to application date is not allowed.

Note that for High Balance Transactions a minimum of 7 years must have elapsed since the discharge date regardless of AUS findings.

Chapter 13

The borrower’s credit history since the bankruptcy, the circumstances behind the bankruptcy, and the discharge date all factor in to the final determination by the underwriter.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for VA financing

Foreclosure / Short Sale

Foreclosure more than 36 months prior to application date may be disregarded.

Foreclosure less than 36 months prior to application date is not allowed.

Note that for High Balance Transactions a minimum of 7 years must have elapsed since the foreclosure date regardless of AUS findings.

In all instances, the “date of foreclosure” is considered the date of the foreclosure deed.

USDA Guidelines for Bankruptcy and Foreclosure

Chapter 7

The Discharge date and GUS findings both play an important role in determining the viability and future repayment of the new loan. As such, Chapter 7 bankruptcy seasoning is evaluated by GUS.

Chapter 13

Loans where the borrower is currently in a Chapter 13 bankruptcy or had a Chapter 13 bankruptcy which was discharged within the previous 3 years require a manual downgrade and must be underwritten manually.

A borrower who is currently in a Chapter 13 bankruptcy may be eligible for RD financing provided all of the following conditions are met in addition to standard manual underwriting requirements:

• At least 12 months of payments have been made satisfactorily

• The Trustee or bankruptcy judge’s approval to enter into the mortgage transaction is documented

• Bankruptcy payments are included in the borrower’s debt ratio

Foreclosure / Short Sale

The foreclosure date and GUS findings both play an important role in determining the viability and future repayment of the new loan. As such, foreclosure seasoning is evaluated by GUS.

A foreclosure does not automatically disqualify a borrower from RD financing. In all instances, the “date of foreclosure” is considered the date of the foreclosure deed.

You can obtain a copy of your bankruptcy paperwork from the website below:

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

2018 KENTUCKY FHA MORTGAGE GUIDELINES FOR APPROVAL WITH STUDENT LOANS

Student Loan Payment Calculation

Must include all student loans in the borrower’s liabilities, regardless of the payment type or status of payments.

Calculation of monthly obligation, regardless of the payment status, must use either:

the greater of: • 1 percent of the outstanding balance on the loan; or • the monthly payment reported on the borrower’s credit report; or

the actual documented payment, provided the payment will fully amortize the loan over its term.

Additional documentation required if the payment used for the monthly obligation is: • less than 1 percent of the outstanding balance reported on the borrower’s credit report;and • less than the monthly payment reported on the borrower’s credit report. Provide written documentation of the actual monthly payment, the payment status, and evidence of the outstanding balance and terms from the creditor. Guide Reference – 4000.1 II.A.4.b.iv(H) (TOTAL) and II.A.5.a.iv.(G) (Manual)

I can answer your questions and usually get you pre-approved the same day.

Call or Text me at 502-905-3708 with your mortgage questions. Email Kentuckyloan@gmail.com

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

, NMLS ID# 57916, (www.nmlsconsumeraccess.org). I lend in the following states: Kentucky