Is an Kentucky FHA loan right for you?

Here are some benefits of Kentucky FHA loans 🤩

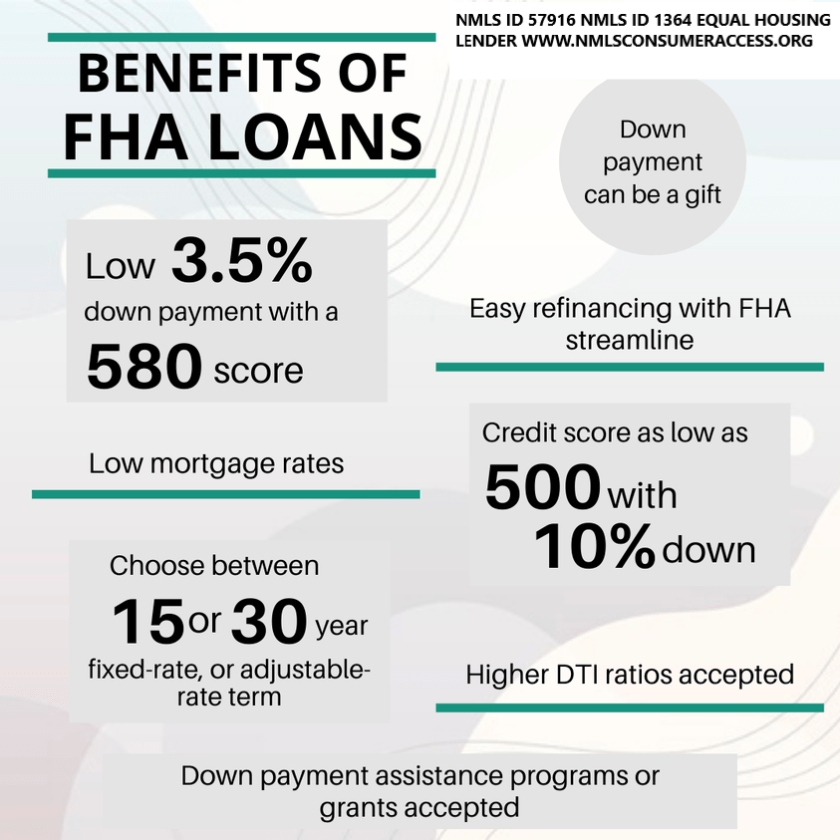

✅ Low down payment options

✅ Down payment assistance programs available

✅ Higher DTI ratios acceptedFHA requires you to establish that the income is in fact stable. I am covering Time on Job, Part Time Income, Seasonal Income and Job Gaps below.Time on JobThere is not a minimum length of time a borrower must have held a position for the income to be eligible. However, the application must identify the most recent 2 years of employment.If the borrower’s employment history indicates that they were in school or in the military, then the borrower must provide evidence supporting this such as college transcripts or discharge papers.The current type of employment has to be supported by the college transcripts or discharge papers showing that he borrower’s training enabled them to gain employment in their field of training.Part Time Income

Part-time and second job income can be used to qualify if documentation is obtained to prove that the borrower has worked the part-time job uninterrupted for the past two years, and plans to continue.For Qualifying purposed, “part-time” income refers to jobs taken to supplement the borrower’s main income from regular employment, such as a second job that is less than 40 hours per week.Income: Is averaged over the previous 2 years. If there was a pay rate increase and we can document the increase in pay, you can average the new pay rate over 12 months.Seasonal IncomeSeasonal income may be acceptable for qualifying. It is not unusual to have out-of-season income from unemployment income. If the borrower has a 2 year history and continuance is probable, this type of income may be allowed to qualify the borrower.The key here is history and continuance.Job GapsThe borrower must provide a signed explanation for gaps in employment as follows:Income can be considered effective if the following can be verified:1. Borrower has been employed in the current job for at least six months at the time of the case number assignment AND2. A two year work history prior to the absence from employment.What does FHA stand for?

FHA stands for Federal Housing Administration, and the FHA is a government agency that insures mortgages. It was created just after the Great Depression, at a time when homeownership was prohibitively expensive and difficult to achieve because so many Americans lacked the savings and credit history to qualify for a loan. The government stepped in and began backing mortgages with more accessible terms. Approved lenders began funding FHA loans, which offered more reasonable down payment and credit score standards.

Today, government-backed mortgages still offer a safety net to lenders—because a federal entity (in this case, the FHA) is guaranteeing the loans, there’s less financial risk if a borrower defaults on their payments. Lenders are then able to loosen their qualifying guidelines, making mortgages available to middle and low income borrowers who might not otherwise be approved under conventional standards.

What’s the difference between FHA and conventional loans?

Home loans fall into two broad categories: government and conventional. A conventional loan is any mortgage that is not insured by a federal entity. Because private lenders assume all the risk in funding conventional loans, the requirements to qualify for these loans are more strict. Generally speaking, FHA loans might be a good fit if you have less money set aside to fund your down payment and/or you have a below-average credit score. While low down payment minimums and competitive interest rates are still possible with a conventional loan, you’ll need to show a strong credit score to qualify for those advantages.

Each loan type has advantages and disadvantages—including different mortgage insurance requirements, loan limits, and property appraisal guidelines—so choosing the one that works best for you really depends on your financial profile and your homebuying priorities.

FHA loans pros and cons

FHA loans are meant to make homeownership more accessible to people with fewer savings set aside and lower credit scores. They can be a great fit for some borrowers, particularly first time homebuyers who often need lower down payment options, but you should weigh the costs and benefits of any mortgage before committing. Here’s a breakdown of the key pros and cons when it comes to FHA loans:

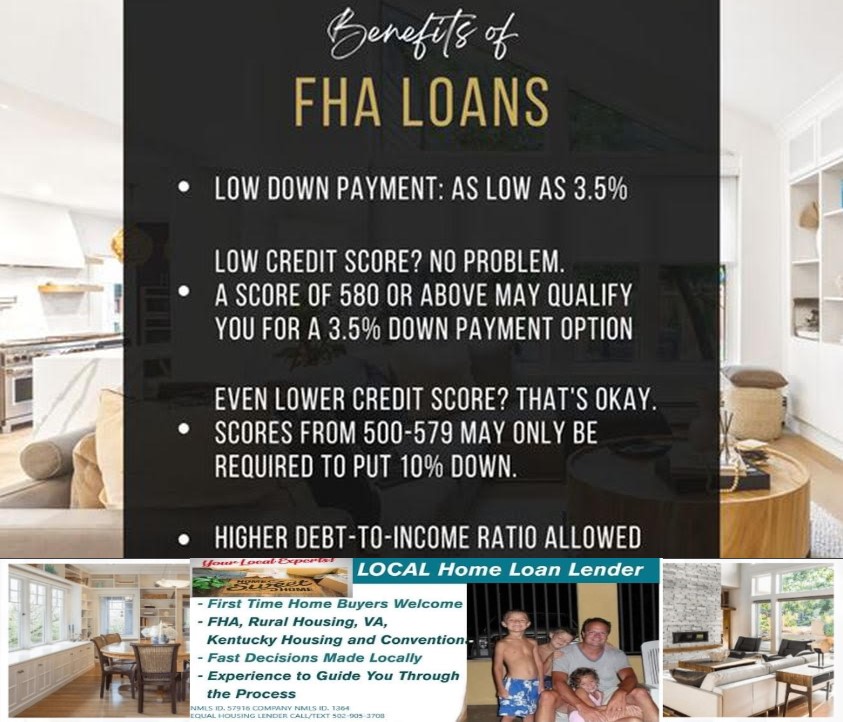

Pros Cons Low down payment. Down payments make up the majority of cash to close in any purchase loan, and saving up for one can be a significant barrier for some borrowers. FHA loans make it possible to put down as little as 3.5% upfront and still get competitive rates. Mandatory MIP payments. FHA loans are more lenient, but they also come with insurance costs to mitigate risk to the lender. You’ll have to pay Mortgage Insurance Premiums (MIP) no matter what—either for 11 years or for the life of your loan, depending on your down payment. Lower credit score. Credit scores can be a major hurdle when it comes to conventional loans, but borrowers with credit scores starting at 500 can qualify for FHA loans. Less competitive. Sometimes sellers can be more hesitant to accept FHA loans. In a competitive market, you might not win out against conventional loan bids. Higher DTI accepted. Your debt-to-income (DTI) ratio gives lenders an understanding of other major financial obligations in your life. This ratio is a key factor in any loan application because it indicates your ability to afford a mortgage based on current household income and existing debt. Again, FHA loans offer more leniency here and borrowers at or below 43% DTI can qualify. Stricter property standards. To offset risk and further protect lenders, FHA loans have strict criteria when it comes to assessing the condition of any property being purchased with an FHA loan. The downside? The house you want to buy might not qualify for an FHA loan. The upside? You’re less likely to be financially burdened by a home that requires expensive repairs or updates. No income limitations. It’s a common misconception that FHA loans are only available to first-time homebuyers or borrowers with limited income—but they’re not. There’s no maximum income limit that would disqualify you from this type of loan. Loan limits: FHA loan limits are typically lower than conventional loan limits, which means you might not be able to get funding for more expensive houses. This isn’t necessarily a bad thing, since it helps ensure that borrowers get loans they can afford to repay. How to qualify for an FHA loan

Qualifying for an FHA loan is generally easier than qualifying for a conventional loan, but you’ll still need to meet some basic minimum standards set by the FHA. While the government insures these loans, the funding itself comes through FHA-approved lenders each lending institution may have slightly different qualifying guidelines for its borrowers. Keep in mind that, while these FHA standards offer a basic framework, you’ll need to confirm the individual qualifying rules with your specific lender.

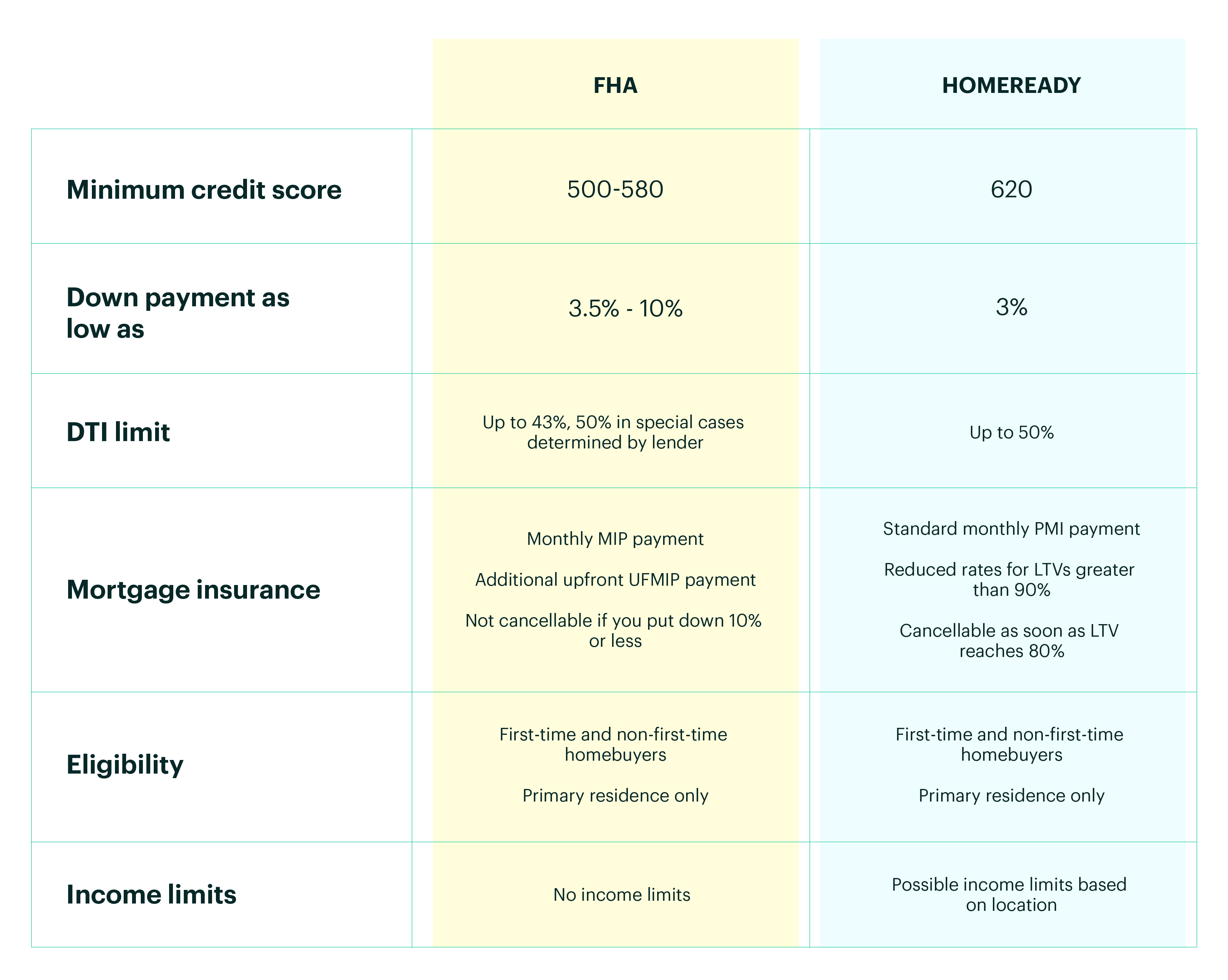

Credit score minimum 500. Your exact credit score will play a big role in determining your down payment minimum; typically, the higher your credit score, the lower your down payment and the more favorable your interest rate.

Debt-to-income ratio at or below 56.9%. DTI is a standard way of comparing the amount of money you earn to the amount you spend paying off other debts, and FHA loans are more lax on this number.

Steady income and proof of employment. Being able to provide at least 2 years of income and employment records is a standard requirement for all loans.

Down payment between 3.5%-10%. The down payment minimum for an FHA loan is typically lower than conventional loan, and can be as little as 3.5% depending on your credit score and lender.

Property standards apply. You won’t qualify for an FHA loan if the house you want to buy doesn’t pass the appraisal process, which is more strict with this type of loan than conventional mortgages.

Maximum FHA loan amount. The amount of money you borrow cannot exceed the FHA loan limits; this number changes based on your county and is determined by how expensive the local market is; the maximum FHA loan limit in 2021 is $420,000 (check HUD resources to confirm the latest limits.)

Joel Lobb

Senior Loan Officer

(NMLS#57916)American Mortgage Solutions, Inc.

10602 Timberwood Circle, Suite 3

Louisville, KY 40223text or call my phone: (502) 905-3708

email me at kentuckyloan@gmail.comThe view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency.

The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (http://www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.

KENTUCKY FHA MORTGAGE GUIDELINES FOR 2020

- FHA – 620+ Min Fico Approve Eligible / NO OVERLAYS-NONE!

- FHA – 620+ FICO for PURCH, RT, C/O including Flips & High Balance

- FHA – 640+ REFERS OK!—no overlays -u/w directly to 4000.1

- FHA – 640+ MANUALS up to 50% DTI (with 2 comp factors)

- FHA – 620+ No DTI CAP – Follow AUS Findings!!! (with approved eligible)

- FHA – 620+ NO Minimum Credit History or Trades with AUS Approval!

- FHA – 620+ – No VOR Unless Required by DU Findings!

- FHA – Transfer appraisals from ANY lender/AMC OK!

- FHA – ORDER YOUR APPRAISAL FROM 20+ AMCs YOU CHOOSE!

- FHA – Collections – HUD Guides Apply –

- FHA – Mortgage Lates OK if AUS Approved!!!

- FHA – ESCROW STATE – Non Purchasing Spouse derogs ignored – only affects DTI

- FHA – Borrower w/ Work Permits, Non-Resident Alien OK!

- FHA – 1 Day off Market for Cashout Refi! – Must be off market before date of loan application!

- FHA – Rental Income on 2-4 units ok FTHB

- FHA – STREAMLINE – 620 Minimum

- FHA – Streamline – 620 Score – No Appraisal, No Income, No AVM, No Credit Qualifying!!!

- FHA – Streamline -Investment and 2nd Homes OK!

- FHA – Streamline – Mtg only on subject property only!

Kentucky FHA Home loan programs for people with bad credit

Score Requirement on Kentucky FHA Loans for people with bad credit

Lowers Minimum Credit Score Requirement on Kentucky FHA Loans

Kentucky FHA Home loan programs for people with bad credit

FHA loans are designed to make housing more affordable with lower down payment requirements than conventional loans on purchases and less home equity requirements on refinances. Less stringent qualification guidelines and the security of a government-insured loan makes FHA a popular choice for consumers.

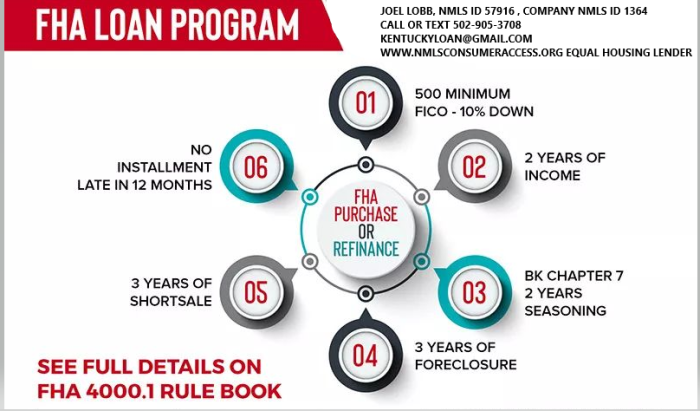

Kentucky FHA Loans with 580 Credit scores and – Low Down Payment – 3.5% which can be gifted from relatives or borrowed off one’s retirement account. If your scores is between 500-579, 10% down needed for home loan and subject to underwriting approval.

- Low down payment

- 500 minimum credit score from 10% down, to 580 above credit score with 3.5% down payment

- Can be used with Grants for Down payment through Eligible Sources

- FHA max loan – $336,750 in the State of Kentucky

- FHA approved condos eligible

- Entire Down payment can be a gift, a down payment assistance program or grant funds

- Seller can pay 6% of purchase price toward closing costs

Quick guide to checking your credit score for Kentucky FHA loans

If you’re just starting to shop for home mortgages, it pays to know if banks think you have bad credit or not. Here’s how FICO, the main credit score provider in the U.S., breaks down credit scores:

- 800-plus: Exceptional

- 740-799: Very good

- 670-739: Good

- 580-699: Fair

- 579 and lower: Poor

Kentucky FHA loans

|

Kentucky FHA Loan Details

|

|

|---|---|

|

Credit score required

|

500, but banks have minimum underwriting

standards |

|

Down payment required

|

Credit score between 500-579: 10 percent

Credit score above 580: 3.5 percent |

|

Upfront financing fee

|

1.75 percent, which can be financed

|

|

Mortgage insurance

|

0.45 to .85 percent

|

|

Mortgage limits

|

Generally, $336,766 for single-family units, but it

varies by location and you should check the limits in your area |

|

Fine print

|

Mortgage insurance premiums are paid for the life of the loan,

except when putting 10 percent or more down. If your down payment is less than 20 percent but 10 percent or more, you must have mortgage insurance for 11 years. |

Quick take

If you have bad credit, an Kentucky FHA loan offers a more accessible mortgage. While credit standards vary by lender, you may qualify for the Kentucky FHA loan with a credit score as low as 500. With a credit score above the 580 threshold, you may qualify for the 3.5 percent down payment.

Unfortunately, an Kentucky FHA loan can be expensive because of mortgage insurance fees. In addition to paying ongoing mortgage premiums for the life of the loan, you’ll have to pay a 1.75 per

Pros:

Cons:

|

Lending 101: FHA Loans In Kentucky

|

|

Kentucky FHA loans are great loan program that is not just for first-time buyers!

Kentucky FHA loans are great loan program that is not just for first-time buyers!

Kentucky FHA Down Payment Requirements, Credit Scores and Mortgage Insurance

How Credit Scores Impact Kentucky FHA Loan Down Payment Requirements

Kentucky Home Buyers credit scores are one of the largest factors in determining the amount of a down payment for an FHA loan. A credit score of 580 or higher, 3.5 percent is the minimum required for a down payment. Anyone with a credit score of 500 to 579 will have to save 10 percent for a down payment to obtain an FHA loan.

What Are Mortgage Insurance Requirements on Kentucky FHA Loans?

FHA loans are required to pay mortgage insurance premiums, often known as upfront mortgage insurance premiums and monthly annual premiums.

- Upfront mortgage insurance premium: 1.75 percent of the loan amount and is paid when the borrower gets the loan. The premium can be rolled into the mortgage.

- Annual mortgage insurance premium: 0.45 percent to 1.05 percent, depending on the term of the loan (15 years vs. 30 years), the loan amount and the initial loan-to-value ratio, or LTV. This premium amount is divided by 12 and paid monthly.

For a homeowner who borrows $150,000, this means the upfront mortgage insurance premium would be $2,625 and your annual premium would range from $675 ($56.25 per month) to $1,575 ($131.25 per month), depending on the length of the mortgage.

Unlike traditional mortgage insurance premiums, homeowners are required to pay FHA premiums for the entire term of the mortgage. The only time you can stop paying them is to refinance into a non-FHA loan or to sell the house.

Down Payment Gifts and Rules for Kentucky FHA Loans Kentucky borrowers choose an FHA loan can receive money as a gift to help towards the total amount of the down payment.

There are several rules that homeowners need to keep in mind. Gifts can come from friends, family members, labor unions and employers, according to data from the Department of Housing and Urban Development (HUD).

Even non-profit organizations can provide money for a contribution toward a down payment.

In addition, each state offers various assistance programs for down payments for both FHA buyers in Kentucky lacking the down payment.

People obtaining an Kentucky FHA loan are also eligible for these programs. I.e. Kentucky Housing Dap Funds, Welcome Grants In Kentucky

What are the requirements to qualify for a Kentucky FHA Mortgage?

What are the requirements to qualify for a Kentucky FHA Mortgage in 2020?

Kentucky FHA loan is a mortgage that is insured by the Government agency under Housing and Urban Development that is called FHA or short for Federal Housing Administration. The loan was established for Kentucky Home buyers will very little or no money down home loans with more lenient credit score and income requirements and tends to be more forgiving about credit history with regard to bankruptcy and foreclosures, higher debt to income ratios and job history with limited work history for home buyers will only 2 years work history or less.

Kentucky FHA Credit Score Requirements and Down Payment Requirements

The Kentucky FHA home loan program may accept credit scores as low as 580 and require at least a 3.5 percent down payment of the sales price on a purchase. If you have a credit score below 580, then a 10 percent down payment or more may be acceptable some FHA lenders in Kentucky , providing you meet all program guidelines in regards to debt to income ratios, assets, and income requirements . The loan cannot be used for rental properties and does allow for co-signers if they are related.

Remember, these guidelines are set forth by FHA and all lenders do not have to offer these guidelines, to whereas they may a higher credit score or more money down or income restrictions on how much you can qualify for.

Kentucky FHA Mortgage Loans and Bankruptcy or Foreclosure

In case you had a blemish on your credit report with a bankruptcy, short sale or foreclosure, follow these guidelines.

Kentucky FHA loans requires a passage of two years since the discharge date of a chapter 7 bankruptcy. A chapter 13 bankruptcy may be acceptable after at least 12 months of an on time pay-back period and the borrower has received permission from bankruptcy court to enter the mortgage transaction, and you qualify with the new house payment along with other debts on the credit report.

Three years must pass if you went through a short sale or foreclosure. The date starts when the home was sold, not when you entered the transaction toward foreclosure or short sale period. Sometimes the house will not sell to 1-2 years later after the foreclosure and this is when the passage date starts. Keep this in mind on your next FHA loan pre-approval if you have had a bankruptcy or foreclosure in the past.

Kentucky FHA Loans and Mortgage Insurance

FHA loans have two forms of mortgage insurance which protects the lender for any losses suffered if the borrower defaults on the payment. ne is called upfront mortgage insurance premium (UFMIP) which has a rate of 1.75% of the loan amount. The fee can be added to the loan amount or paid in full as part of your closing costs. In addition, FHA loans also have a 0.8-0.85% (of the loan amount) monthly mortgage insurance. In most cases, this mortgage insurance remains for the life of the loan. To eliminate the mortgage insurance, the borrower must refinance the loan into a non-FHA loan program and have 20% equity in the property.

In addition to the down payment requirements on a FHA loan, they’re closing costs and prepaids to pay at closing. The seller can contribute up to 6% of the sales price to help the buyer with closing costs and prepaid expenses. Closing costs vary from lender to lender and your prepaids would be the same no matter which lender you choose because this is a function of the property ‘s home insurance premium quote you obtain and the property tax bill on the home set by PVA.

Sometimes the lender can pay a credit toward these expenses at closing with a lender credit which lets the lender credit back to you with a higher rate to reduce the costs of the loan’s costs at closing for out of pocket expenses.

All Kentucky FHA loans are assumable, which means that when the homeowner sells a home, the buyer may be able to take on the existing loan and terms (e.g.: balance, rate and remaining loan amount). Of course, anyone interested in the assumable loan feature must go through the approval process (credit check, income verification) with the current lender on the property. This is a very rare occurrence because most sellers are going to sell the home for more than they owe on it.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

How to qualify for a Kentucky FHA Home Loan ?

It’s important to understand the different types of loan programs available to you and what benefits and drawbacks there are to each type.

For example, if you’re looking to find a fixer upper this may not be the right loan program for you. But an FHA loan may be a better fit for you if you have little cash saved up for a down payment or if you don’t have a high credit score.

Kentucky FHA loan requirements:

- At least 18 years old to apply

- No age limit. just must be 18 years of age to apply.

- Must occupy the home as a primary residence, no rental homes or investment property

- An appraisal must be done by an FHA-approved appraiser.Typically FHA appraisal in Kentucky costs anywhere from low-end $325 to $525 with most FHA lenders in KY.

- Home inspection is not required

- Termite inspection not required

- 2 years removed from Chapter 7 bankruptcy, and 1 year in Chapter 13 bankruptcy is possible to get a loan while in bankruptcy

- Foreclosure or short sale on previous home mortgage requires 3 years removal from those dates.

- Mortgage insurance (MIP) is required

- Upfront Mortgage Insurance Premium is 1.75% and monthly mortgage insurance is .85% or .80% depending on loan term and loan to value.

- Mortgage insurance is for life of loan.

- No matter your credit scores, everyone pays the same mortgage insurance premiums.

- Must have 2 years of employment history proving a reliable source of income

- 500 FICO score requirement with at least 10% down payment

- 580 FICO score requirement with at least 3.5% down payment

- Gifts and down payment assistance programs are allowed to meet your down payment requirements. Cannot come from seller, but seller can contribute up to 6% of the sales price toward buyer’s closing costs and prepaids.

- Student loan payments are factored into the debt-to-income ratio when applying. Typically if loans are deferred, or in an income=based repayment plan, the FHA underwriters will use 1% of the outstanding balance, which sometimes can make it difficult to qualify.

- Your debt-to-income ratio must not be higher than 31% or total debt obligation cannot be higher than 43% of your current income. This is for a manual underwriter, meaning that if the AUS underwriting system by mortgage lenders will approve you for a higher debt to income ratio, that is fine.

Joel Lobb (NMLS#57916)

Senior Loan Officer

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

|

How to get rid of Mortgage Insurance on a Kentucky Mortgage Loan.

Eliminate FHA Mortgage Insurance On Your Kentucky FHA Loan.

Mortgage insurance premium can add almost $200 to the payment on a $265,000 FHA mortgage. The decision to get an FHA loan may have been the lower down payment requirement or the lower credit score levels, but now that you have the loan, is it possible to eliminate it?

Mortgage Insurance Premium protects lenders in case of a borrower’s default and is required on FHA loans. The Up-Front MIP is currently 1.75% of the base loan amount and paid at the time of closing. Annual MIP for loans with greater than 95% loan-to-value is .85% per year.

For loans with FHA case numbers assigned before June 3, 2013, when the loan is paid down to 78% of the original loan amount, the MIP can be cancelled. The borrower may need to contact the current servicer.

However, for loans greater than 90% with FHA case numbers assigned on or after that date, the MIP is required for the term of the loan.

Most homeowners with FHA mortgages are not eligible to cancel the MIP because they either originated their loan after June 3, 2013, put less than 10% down payment and/or got a 30-year loan. If they have at least 20% equity in the home, they can refinance the home with an 80% conventional loan which in most cases, does not require mortgage insurance.

With normal amortization on a 30-year loan, it takes approximately 11-years to reduce the original loan to the 78-80% requirement based on normal amortization. There is another dynamic involved which is the appreciation on the home. As the home goes up in value and the unpaid balance goes down, the equity increases.

If the homeowners believe that they have enough equity that would eliminate the need for mortgage insurance, they can investigate refinancing with a conventional loan. Borrowers refinancing will incur expenses in starting a new mortgage and the interest rate may be higher than the existing rate. Analysis will determine how long it will take to recapture the cost of refinancing.

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

KENTUCKY HUD HOMES FOR SALE

FHA’s $100 Down Program is allowed for Kentucky Home Buyers buying a home that is owned by HUD or FHA. The $100 Down sales incentive permits a Borrower to purchase a HUD REO Property with FHA-insured financing with a minimum downpayment of $100.

This program can ONLY be used to purchase homes owned by HUD OR FHA.

Check the link below to see if any properties are offered in your area. If a property is eligible, the listing on the website will specify $100 Down Financing Incentivize.

You can find all current listings for sale by HUD here.

The main factors in qualifying for this Kentucky FHA program are that the property must be a HUD REO property and purchased using FHA Financing, aside from these, the requirements include:

- Occupancy: The property must be purchased for use as your Primary Residence.

- Property Type: Eligible properties include 1 or 2 unit homes, manufactured homes, condos, and PUDs.

- Full Price Offer: You must submit an offer for the full listing price. Typically, when you purchase a home, you make an offer to the seller…. we all want to get the best deal so you may offer less than the asking price… or you may offer more if the home you want is being bid on by many buyers…. With HUD REO properties this is not allowed. The sales price HUD has on the listing is what you must offer.

- Sales Contract: The $100 down payment incentive must be included on the executed sales contract.

- Cannot have purchased a HUD home within the preceding 24 months

- Credit Score: 580 is the minimum FICO score you must have to qualify for a FHA Kentucky Home Buyer using the HUD $100 Down loan program.

- Usually takes about 30-45 days to close

- Earnest Money Deposit usually needs to be at least $500 to $1000

- This is a manual underwriter meaning that your debt to income ratio has to be 31 and 43% respectively

- No Chapter 7 Bankruptcies in last two years

- No Foreclosures in last 3 years

- Clear Cavirs on borrowers.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

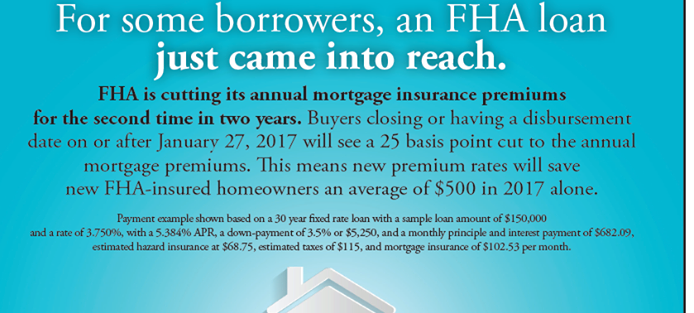

Kentucky FHA Loans Beginning January 27, 2017 will have lower mortgage insurance fees

For the first time in two years, the Federal Housing Administration (FHA) has announced that it will be lowering its annual mortgage insurance premiums for Kentucky FHA Homebuyers and homeowners looking to refinance a FHA mortgage loan

Kentucky Homeowners with an existing FHA loan that haven’t refinanced in the past two years may be able to reduce their payment and get a lower monthly payment.

U.S. Housing and Urban Development Secretary Julián Castro said on Monday the FHA will reduce the annual premiums most borrowers will pay by a quarter of a percent, or 25 basis points, for most new mortgages with a closing or disbursement date on or after January 27th of 2017. The new rates are projected to save new FHA-insured homeowners an average of $500 this year, Castro said.

When the FHA announced late last year that its flagship fund, the Mutual Mortgage Insurance Fund, grew for the fourth straight year, it led to many question whether we would see a cut to its mortgage insurance premiums again. Now we have an answer. Click the headline for the full details on the FHA reducing mortgage insurance premiums.

Source: FHA cuts mortgage insurance premiums again

2017 Kentucky FHA Annual Mortgage Insurance Premiums

According to the FHA, it will cut the annual mortgage insurance premiums most borrowers will pay by one-quarter of a percentage point, or 25 basis points

Joel Lobb

Senior Loan Officer

Senior Loan Officer

(NMLS#57916)

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice. Manufactured and mobile homes are not eligible as collateral.

Kentucky FHA loan mortgage insurance changes for 2017. Lower mortgage monthly insurance premium-savings of 25% for Louisville, Kentucky FHA homebuyers and homeowners

fha reduced mip program

Kentucky FHA Loan Limits for 2019

|

Kentucky FHA Loan Limits for 2019

FHA has announced new loan limits for 2019. For all FHA loans with Case Numbers assigned on or after January 1st, the following will be effective

these values are updated to coincide with the new FNMA loan limit floor values.

|

Kentucky Lending Limits for FHA Loans in KENTUCKY Counties

FHA mortgage lending limits in KENTUCKY vary based on a variety of housing types and the cost of local housing. FHA loans are designed for borrowers who are unable to make large down payments.

HUD Announces Higher FHA Loan Limits for 2019

December 20, 2018 – The HUD official site has announced higher FHA home loan limits for 2019. The higher loan limits are attributed to what the agency describes as “robust” increases in median housing prices over the last year. Nationwide, the limit for “average” housing markets-defined as those not in high-cost or low-cost areas-is set in 2019 at $314,827.

That is an increase from 2018 when the limit was set at $294,515.

1

Joel Lobb (NMLS#57916)

Senior Loan Officer

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916 http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.