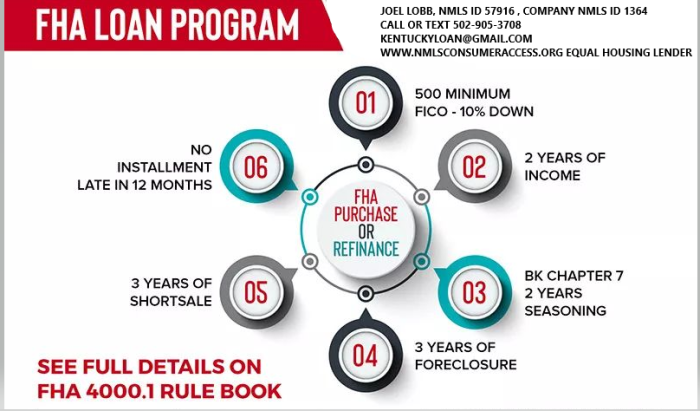

Kentucky FHA Refinance Guide (HUD-Compliant)

FHA UFMIP Refund: Official HUD Rules Kentucky Homeowners Need to Know

If you refinance an existing FHA loan into a new FHA loan, HUD may provide a partial refund of your upfront mortgage insurance premium.

What is an FHA UFMIP Refund?

FHA requires an upfront mortgage insurance premium (UFMIP), typically 1.75% of the base loan amount. According to HUD guidance, borrowers who refinance an FHA-insured loan into another FHA-insured loan may be eligible for a partial refund of the previously paid UFMIP.

The refund is not paid in cash. It is applied as a credit toward the new upfront mortgage insurance premium on the new FHA loan.

HUD Requirements for Eligibility

- Existing loan must be FHA-insured

- New loan must also be FHA-insured

- Loan must not be delinquent beyond HUD allowable limits

- Refinance must meet FHA net tangible benefit requirements

How the FHA UFMIP Refund is Calculated

HUD does not use a flat percentage schedule for public guidance. Instead, the refund is calculated using FHA’s official insurance amortization method based on:

- Time elapsed since loan endorsement

- Original upfront premium paid

- Remaining insurance exposure

The refund amount declines monthly and is administered through FHA Connection at the time of refinance.

Critical HUD Rule

Example (HUD-Based Explanation)

Example scenario based on FHA structure:

- Loan Amount: $200,000

- UFMIP Paid: $3,500

- Refinance within first 12–24 months

A portion of the $3,500 may be credited toward the new FHA upfront premium, depending on the exact month of refinance and HUD’s internal calculation.

What This Means Strategically

From a lending strategy standpoint, this creates a limited-time refinance window where:

- You may recover part of your upfront cost

- You may reduce your interest rate

- You may lower your monthly payment

However, the benefit declines every month and disappears after 36 months. Timing is critical.

Common Misconceptions

- There is no guaranteed refund percentage

- Refunds are not issued as cash payments

- This does not apply to conventional, VA, or USDA refinancing

When Should Kentucky Homeowners Review This?

If your FHA loan closed within the last 36 months, it is worth evaluating your refinance options immediately. Waiting reduces or eliminates your refund eligibility.

Free FHA Refinance Review

Find out if you qualify for a UFMIP refund and lower payment.

Call/Text: 502-905-3708

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

Joel Lobb | Mortgage Loan Officer | NMLS #57916 | Company NMLS #1738461 | Equal Housing Lender

This is not a commitment to lend. All loans are subject to credit approval and program requirements.

This website is not affiliated with or endorsed by FHA, VA, USDA, KHC, or any government agency.

Kentucky FHA Refinance Guide (HUD-Compliant)

FHA UFMIP Refund: Official HUD Rules Kentucky Homeowners Need to Know

If you refinance an existing FHA loan into a new FHA loan, HUD may provide a partial refund of your upfront mortgage insurance premium.

FHA borrowers in Kentucky often overlook one major refinance benefit: if you refinance from one FHA-insured loan into another FHA-insured loan, part of the upfront mortgage insurance premium you previously paid may be credited toward the new loan.

Timing matters. The longer you wait, the smaller the benefit becomes. After 36 months, the refund opportunity is generally gone.

Refinance timing directly impacts how much FHA UFMIP may be credited toward your new loan.

What is an FHA UFMIP Refund?

FHA requires an upfront mortgage insurance premium (UFMIP), typically 1.75% of the base loan amount. If you refinance your existing FHA loan into another FHA-insured loan, part of that previously paid premium may be credited toward the new upfront mortgage insurance premium.

HUD Requirements for Eligibility

- Existing loan must be FHA-insured

- New loan must also be FHA-insured

- Loan must meet FHA payment history guidelines

- Refinance must meet net tangible benefit requirements

Critical HUD Rule

Free FHA Refinance Review

Find out if you qualify for a UFMIP refund and lower your payment.

Call/Text: 502-905-3708

Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA

Joel Lobb | Mortgage Loan Officer | NMLS #57916 | Company NMLS #1738461 | Equal Housing Lender

This is not a commitment to lend. All loans are subject to credit approval and program requirements.

This website is not affiliated with or endorsed by FHA, VA, USDA, KHC, or any government agency.

1 – Email – kentuckyloan@gmail.com

2. Call/Text – 502-905-3708

Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com

Website: www.mylouisvillekentuckymortgage.com Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process