Medical Debt and Mortgage Approval for Kentucky Homebuyers

Medical debt has long been a challenge for many Americans. It particularly affects credit scores and the ability to secure a mortgage loan. Fortunately, the Consumer Financial Protection Bureau (CFPB) has finalized a new rule. This rule is set to remove medical debt from consumer credit reports. As a result, more opportunities may open up for homebuyers in Kentucky. Here’s how this change can affect your mortgage approval process. Also, understand what you need to know about medical debt and credit scores in Kentucky.

What’s Changing with Medical Debt and Credit Reports?

The CFPB has implemented a new rule to remove medical debt from credit reports. This change is significant for borrowers in Kentucky. Medical debt often lowers credit scores. It creates hurdles in the mortgage approval process.

Here’s what to expect from the new rule:

Implementation Timeline: The rule is expected to take effect in at least 60 days.

Debt Removed: Over $49 billion in medical debt will be erased from credit reporting systems.

Consumer Impact: An estimated 15+ million Americans will see their credit reports improved.

Credit Score Boost: Consumers affected by this change could see an average credit score increase of 20 points.

Mortgage Approvals: This change is anticipated to result in over 22,000 additional mortgage approvals annually across the U.S.

How Medical Debt Affects Credit Scores in Kentucky

Before this rule, unpaid medical bills often appeared on credit reports, negatively impacting credit scores. In Kentucky, this has been a common issue for homebuyers trying to secure mortgage loans.

Key Effects of Medical Debt on Credit Scores:

Lower Credit Scores: Medical debt can drag down your FICO score, making it harder to qualify for favorable loan terms.

Higher Interest Rates: A lower score often leads to higher interest rates on mortgages.

Mortgage Denials: In some cases, excessive medical debt could result in outright denials of loan applications.

Even with medical debt on your report, mortgage lenders may consider compensating factors. These factors include stable income, down payment assistance, or other positive financial attributes.

How Credit Scores Impact Mortgage Loan Approval in Kentucky

Mortgage lenders in Kentucky use credit scores as one of the primary factors to determine loan eligibility. Here’s how it works:

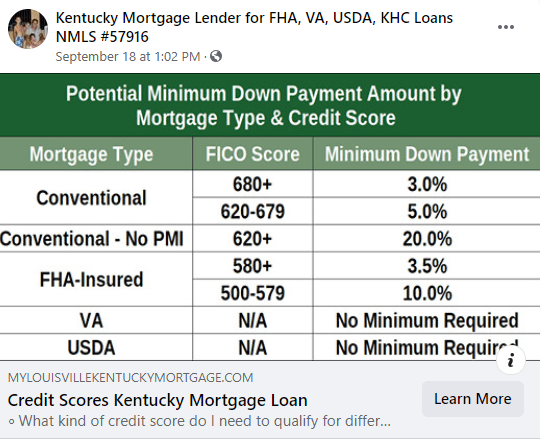

Credit Score Requirements by Loan Type:

FHA Loans: Minimum credit score of 580 with a 3.5% down payment. Scores as low as 500 may be considered with a 10% down payment.

Conventional Loans: Minimum credit score of 620 or higher.

VA Loans: No minimum credit score set by the VA, but most lenders prefer a score of 580-620.

USDA Loans: Minimum credit score of 640 for automatic approval, though manual underwriting is possible for lower scores.

Impact of Credit Score on Interest Rates: Higher credit scores lead to better mortgage rates. Lower scores can result in higher monthly payments.

Debt-to-Income Ratio (DTI): Lenders calculate your DTI to ensure you can manage your mortgage payments alongside other debts. Medical debt previously factored into this calculation, potentially increasing your DTI and reducing your borrowing power.

When you think credit score, you probably think FICO Since the Fair Isaac Corporation introduced its FICO scoring system in 1989, “What is my FICO score?” has become a common question. FICO scores have burrowed their way into all kinds of lending decisions, most notably mortgages, credit cards, and rentals.

But over the last decade or so, FICO’s market dominance has been challenged by a newcomer called VantageScore. As the result of a collaboration between the three major credit reporting agencies (CRAs) — Experian, Equifax, and TransUnion — VantageScore uses similar scoring methods to FICO but with slightly different results.

So what are the differences, and more importantly, do they really matter to you, the consumer? The short answer: usually no. But you might want to look at different scores for different needs or goals.In this article, we’ll cover the five main differences between FICO and VantageScore and tell you which one to watch.

What credit score is needed to buy a house?

1. Difference in scoring models

FICO and VantageScore aren’t the only scoring models on the market. Lenders use a multitude of scoring methods to determine your creditworthiness and make financial decisions. But despite the numerous options, FICO and VantageScore are likely the only scores you’ll ever personally see.How do FICO and VantageScore rate you? Both use the same basic criteria:

Payment history

Length of credit

Types of credit

Credit usage

Recent inquiries

Although both FICO and VantageScore consider much of the same information, they gather their data in different ways.

FICO bases its scoring model on credit reports from millions of consumers at once. They gather these reports from the three major credit bureaus and analyze the reports’ anonymous consumer data to generate an accurate scoring model.Alternatively, VantageScore uses a combined set of consumer credit files, also obtained from those same three credit bureaus, to come up with a single formula.

Both FICO and VantageScore issue scores ranging from 300 to 850. In the past, VantageScore has used a range of 501 to 990, but the range was adjusted when VantageScore 3.0 was issued in 2013. VantageScore’s numerical rankings now match FICO’s, which makes it easier for consumers and lenders to implement the VantageScore model — plus, it’s less confusing for consumers who check both their FICO score and VantageScore.

2. Variance in scoring requirements

If you don’t have a long history of credit, VantageScore is the score you want to monitor. Before it’s able to establish your credit score, FICO requires at least six months of credit history and at least one account reported to a CRA within the last six months. VantageScore only requires one month of history and one account reported within the past two years.

Because VantageScore allows a shorter credit history and a long period for reported accounts, it’s able to issue credit ratings to millions of consumers who wouldn’t qualify for FICO scores. Considering how everyone from employers to landlords wants to see your credit score these days, if you’re new to credit or haven’t been using it recently, VantageScore might be able to prove your trustworthiness before FICO has enough data to issue a rating.

3. Significance of late payments

A history of late payments will impact both your FICO score and your VantageScore. Both models consider these factors:

How recently the last late payment occurred

How many of your accounts have had late payments

How many payments you’ve missed on an account

However, while FICO treats all late payments the same, VantageScore judges them differently — it penalizes late mortgage payments more harshly than other types of credit.If you’ve had late payments on your credit cards, they will have about the same impact on both your FICO and your VantageScore. But if you’ve had late payments on your mortgage, you might find you have a higher FICO score than VantageScore.

4. Impact of credit inquiries

You’ve probably heard you shouldn’t open too many credit cards in a short period of time. One reason for this is every time you apply for a credit card, the lender does a “hard inquiry” to check your creditworthiness.

VantageScore and FICO both penalize consumers who have multiple hard inquiries in a short period of time, and they both do “deduplication.” Deduplication is important for things like auto loans, where your application may be sent to multiple lenders, thereby resulting in multiple inquiries. Both FICO and VantageScore don’t count each of these inquiries separately — they deduplicate them, or consider them one inquiry. However, the timespan they use for deduplication differs.

FICO uses a 45-day span to deduplicate your credit inquiries. VantageScore limits its focus to only a 14-day range. VantageScore also looks at multiple hard inquiries for all types of credit, including credit cards. FICO considers only mortgages, auto loans, and student loans.

Inquiries aren’t your biggest concern when it comes to your credit score, but they do have an impact. If you want to buy a house or a car, restrict hard inquiries as much as possible to avoid lowering your credit score.

5. Influence of low-balance collections

VantageScore and FICO both have penalties for accounts sent to collection agencies. However, FICO might give you a bit more of a break when it comes to low-amount collection accounts.

FICO ignores all collections where the original balance was under $100. It also doesn’t count collection accounts you’ve paid off. VantageScore, on the other hand, ignores only paid collection accounts, regardless of the original balance amount.

Keep your credit high

Regardless of the differences between FICO and VantageScore, the essential advice for keeping your credit score high remains the same:

Avoid late payments. Pay your bills, and pay them on time.

Keep your credit balances low. Don’t max out your credit cards, and try to keep your cumulative balance to less than 30% — the lower the better.

Apply for new credit only when you have to. Don’t open a bunch of new cards in a short period of time, and don’t close old accounts without good reason.

Which credit scores do mortgage lenders use to qualify people for a mortgage?

While it’s common knowledge that mortgage lenders use FICO scores, most people with a credit history have three FICO scores, one from each of the three national credit bureaus (Experian, Equifax, and TransUnion).

Which FICO Score is Used for Mortgages

Most lenders determine a borrower’s creditworthiness based on FICO® scores, a Credit Score developed by Fair Isaac Corporation (FICO™). This score tells the lender what type of credit risk you are and what your interest rate should be to reflect that risk. FICO scores have different names at each of the three major United States credit reporting companies. And there are different versions of the FICO formula. Here are the specific versions of the FICO formula used by mortgage lenders:

Equifax Beacon 5.0

Experian/Fair Isaac Risk Model v2

TransUnion FICO Risk Score 04

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

Which Score Gets Used?

Since most people have three FICO scores, one from each credit bureau, how do lenders choose which one to use?

For a FICO score to be considered “usable”, it must be based on adequate, concrete information. If there is too little information, or if the information is inaccurate, the FICO score may be deemed unusable for the mortgage underwriting process. Once the underwriter has determined if a score is usable or not, here’s how they decide which score(s) to use for an individual borrower:

If all three scores are different, they use the middle score

If two of the scores are the same, they use that score, regardless of whether the two repeated scores are higher or lower than the third score

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

If it helps to visualize this information:

Identifying the Underwriting Score

Example

Score 1

Score 2

Score 3

Underwriting Score

Borrower 1

680

700

720

700

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc. 10602 Timberwood Circle Suite 3 Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

Joel Lobb, American Mortgage Solutions (Statewide)

Joel has worked with KHC for 12 of his 20 years in the mortgage lending business. Joel said, “A lot of my clients would not have been able to purchase a home of their own or possibly delayed their purchase due to lack of down payment but with the $6,000 DAP loan program, this gets them into a house sooner and starts their path to homeownership while building equity instead of throwing their money away.”