Do I qualify as a Kentucky first-time home buyer?

You are typically considered eligible to apply for first-time home buyer loans and benefits if you haven’t owned your principal residence within the past three years.

Some first-time home buyer assistance programs are even more lenient, offering financial aid in specific areas targeted for redevelopment, even to repeat buyers.

Kentucky First-time home buyer benefits

Benefits can include low- or no-down-payment loans, grants or forgivable loans for closing costs and down payment assistance, as well as federal tax credits with the Kentucky Housing Agency or KHC

Is there an income limit to qualify as a first-time home buyer?

Income limits come into play when you are applying for local, state or federal government assistance. Some national mortgage programs, such as loans issued or backed by the U.S. Department of Agriculture, also have household income limits.

Some low-down-payment conventional loans do, too.

In these cases, your income may be benchmarked to local county limits for low- and moderate-income households.

Lenders, even those working with loan programs authorized by a state housing agency, will likely consider your debt-to-income ratio when determining if you qualify.

How to qualify for a first-time home buyer grant

Grants or forgivable loans that typically don’t require repayment are available to low- and moderate-income borrowers through state first-time home buyer programs. Approval standards vary by program and location but often include household income and home sale price limits.

How to qualify for down payment assistance

Just as for grants, down payment and closing cost assistance is often offered by local and state housing authorities. Again, qualifications vary. Look for income and home sale price caps here, too.

Don’t be surprised if a first-time home buyer class is required to qualify for a grant or down payment assistance. These classes are designed to help you navigate the homebuying process, and can be a good idea to take whether they’re mandatory or not.

What are the requirements to qualify for a first-time home buyer loan?

Qualifications required for approval of a loan vary by the type of mortgage — and even by the lender — but here are some general guidelines:

Kentucky Conventional loans:

For a 3% down payment, you’ll need at least a 620 FICO and a debt-to-income ratio below 50%. The higher your credit score or the lower your debt, the better your chances are for approval.

Kentucky FHA loans:

If you want a down payment as low as 3.5%, you’ll need a FICO score of 580 or higher. With 10% down, your required credit score may go as low as 500.

Kentucky VA loans:

Down payments aren’t generally required for a loan backed by the Department of Veterans Affairs. And while VA-backed loans don’t have a minimum FICO score as a part of their official requirements, many lenders look for a score of 620 or better.

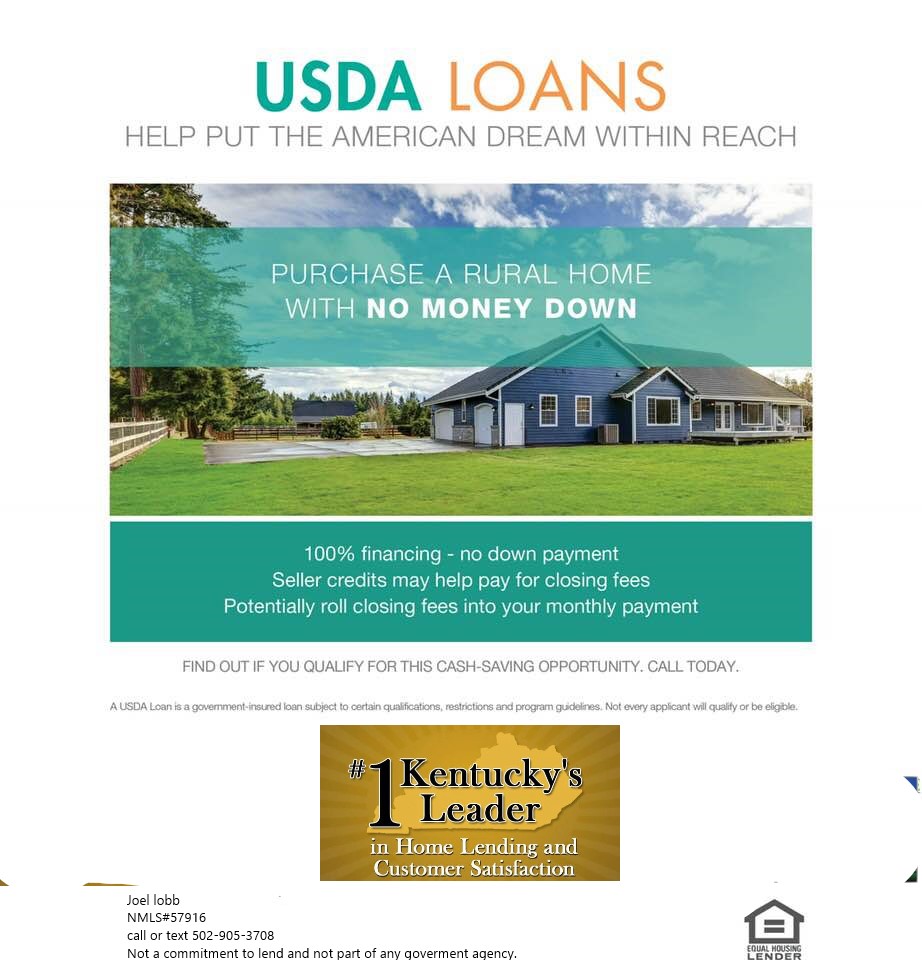

KentukcyUSDA loans:

Another no-down-payment option, USDA-backed loans are typically issued for rural or suburban properties. Income limits apply. A FICO score of 640 or better is generally required, though exceptions with documentation can allow a lower score.

Lenders can add additional conditions, called “overlays,” to loan approval. This is another good reason to shop for more than one lender.

Mortgage Loan Officer

Text/call: 502-905-3708

email: kentuckyloan@gmail.com