This type of loan is administered by KHC in the state of Kentucky. They typically have $12,500 down payment assistance year around, that is in the form of a second mortgage that you pay back over 15 years at a interest rate of 4.75% depending on your income in the household.

Joel has worked with KHC for 12 of his 20 years in the mortgage lending business. Joel said, “A lot of my clients would not have been able to purchase a home of their own or possibly delayed their purchase due to lack of down payment but with the $6,000 DAP loan program, this gets them into a house sooner and starts their path to homeownership while building equity instead of throwing their money away.”

You are typically considered eligible to apply for first-time home buyer loans and benefits if you haven’t owned your principal residence within the past three years.

Some first-time home buyer assistance programs are even more lenient, offering financial aid in specific areas targeted for redevelopment, even to repeat buyers.

Kentucky First-time home buyer benefits

Benefits can include low- or no-down-payment loans, grants or forgivable loans for closing costs and down payment assistance, as well as federal tax credits with the Kentucky Housing Agency or KHC

Is there an income limit to qualify as a first-time home buyer?

Income limits come into play when you are applying for local, state or federal government assistance. Some national mortgage programs, such as loans issued or backed by the U.S. Department of Agriculture, also have household income limits.

Some low-down-payment conventional loans do, too.

In these cases, your income may be benchmarked to local county limits for low- and moderate-income households.

Lenders, even those working with loan programs authorized by a state housing agency, will likely consider your debt-to-income ratio when determining if you qualify.

How to qualify for a first-time home buyer grant

Grants or forgivable loans that typically don’t require repayment are available to low- and moderate-income borrowers through state first-time home buyer programs. Approval standards vary by program and location but often include household income and home sale price limits.

How to qualify for down payment assistance

Just as for grants, down payment and closing cost assistance is often offered by local and state housing authorities. Again, qualifications vary. Look for income and home sale price caps here, too.

Don’t be surprised if a first-time home buyer class is required to qualify for a grant or down payment assistance. These classes are designed to help you navigate the homebuying process, and can be a good idea to take whether they’re mandatory or not.

What are the requirements to qualify for a first-time home buyer loan?

Qualifications required for approval of a loan vary by the type of mortgage — and even by the lender — but here are some general guidelines:

Kentucky Conventional loans:

For a 3% down payment, you’ll need at least a 620 FICO and a debt-to-income ratio below 50%. The higher your credit score or the lower your debt, the better your chances are for approval.

Kentucky FHA loans:

If you want a down payment as low as 3.5%, you’ll need a FICO score of 580 or higher. With 10% down, your required credit score may go as low as 500.

Kentucky VA loans:

Down payments aren’t generally required for a loan backed by the Department of Veterans Affairs. And while VA-backed loans don’t have a minimum FICO score as a part of their official requirements, many lenders look for a score of 620 or better.

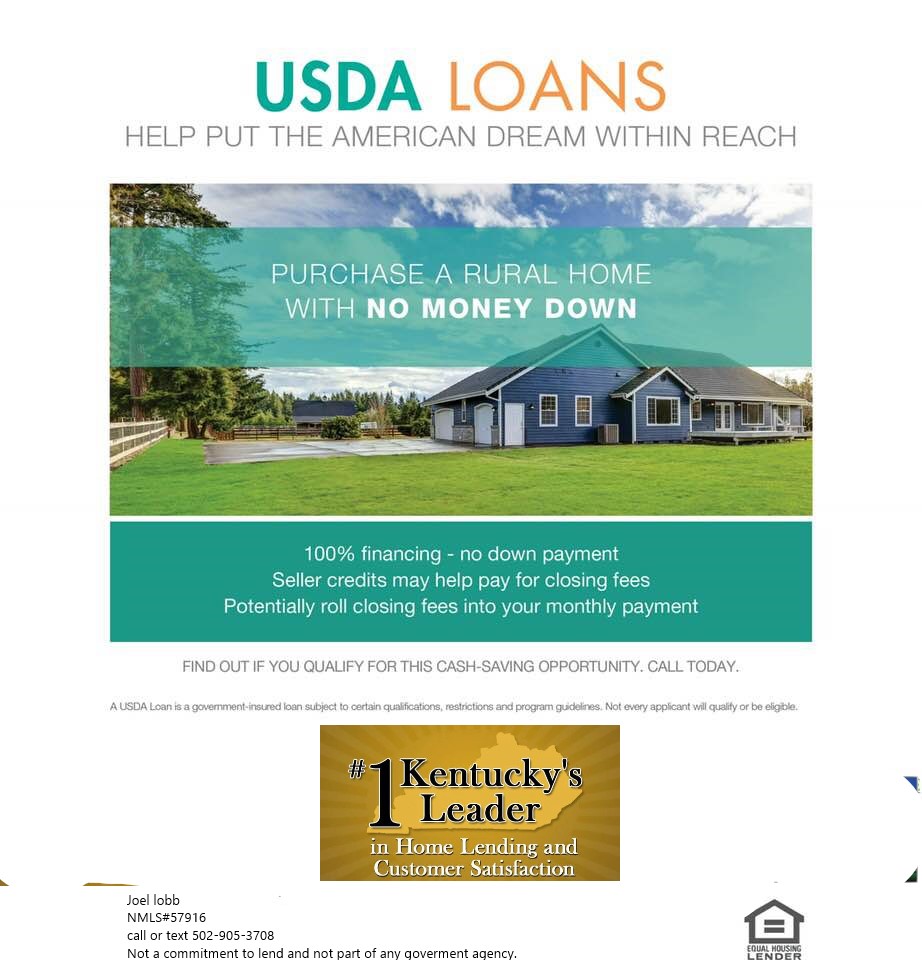

KentukcyUSDA loans:

Another no-down-payment option, USDA-backed loans are typically issued for rural or suburban properties. Income limits apply. A FICO score of 640 or better is generally required, though exceptions with documentation can allow a lower score.

Lenders can add additional conditions, called “overlays,” to loan approval. This is another good reason to shop for more than one lender.

The KY USDA home loans are perfect for first time buyers for many reasons. They have low interest rates, absolutely no down payment, no mortgage insurance, flexible credit guidelines, and most of the closing costs can be worked into the overall amount of the loan.

Advantages of a USDA vs. FHA & Other Loans

The USDA Home Loan program offers many advantages that traditional mortgage programs simply do not offer. First of all, all USDA home loans come with low interest rates, 100% financing, and require zero down payment. In fact, the USDA home loan program is the only home loan program in the country, besides the military, that requires absolutely no money for the purchase of a home. Instead, these funds can be used to pay to furnish the home, closing costs, make home renovations.

USDA home loans also have very flexible credit guidelines compared to most traditional lenders, with non-traditional credit histories being accepted. FHA home loans require a minimum of 3.5% down payment and have relatively high monthly mortgage insurance premiums.

Kentucky USDA Income Eligibility

Because USDA home loans are designed for moderate, to low income families, there are income limit restrictions. To be eligible for a USDA loan, your adjusted annual household income cannot exceed 115% of the median average income for that area.

This means if your total household income is above the average median income for that area, you may not be able to qualify. However, there are special deductions in place, such as childcare expenses, caring for elderly family members, or children in college, that can help to reduce your overall annual income. The borrower’s total housing and other consumer credit payments should account for no more than 4% of the total income. Income limits vary by county. Check your county Kentucky income limits here!

USDA Credit Eligibility

While it is true that USDA home loan program offers some the most credit flexible guidelines available, you still will need to have a minimum credit score of 620 to 640 to qualify.

However, some lenders may accept a credit score of as low as 580, if you can prove that some of your debts were circumstantial, temporary in nature, or beyond your control.

You must also have any bankruptcies or foreclosures discharged in the last 3 years, no outstanding tax liens and no accounts that have gone to collections within the past 12 months.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.