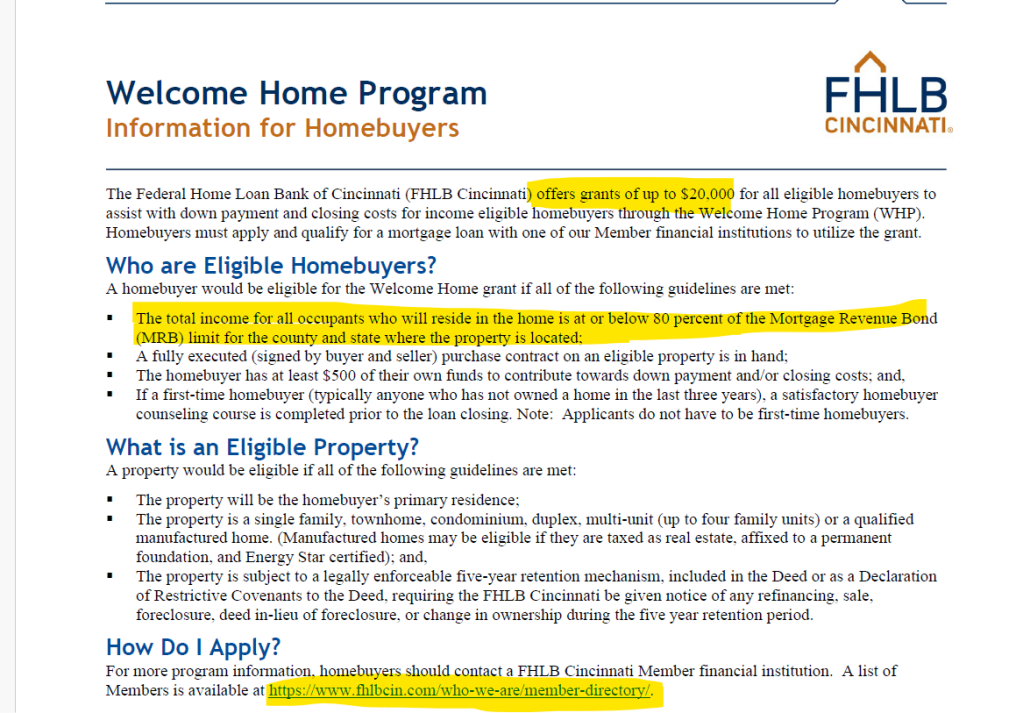

Comparing Kentucky VA loans to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky

Kentucky VA loans Compared to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky

When comparing Kentucky VA loans to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky, several factors come into play. These factors include credit score requirements, income considerations, work history, and debt ratios. They also involve how each loan type treats bankruptcy and foreclosure. Let’s delve into the benefits and differences of each loan type:

Kentucky Mortgage Credit Score Requirements:

- Kentucky VA Loan: VA loans typically have more flexible credit score requirements compared to conventional loans. While there’s no specific minimum score set by VA , most Kentucky VA lenders often look for a credit score of 620 or higher. I can do VA loans down to a 580 credit score.

- Kentucky USDA Loan: USDA loans also offer flexibility, with no minimum score required per USDA guidelines, but most Kentucky USDA lenders will want a 640 score or higher. I Can do Kentucky USDA loans down to a 580 credit score on a manual underwrite.

- Kentucky FHA Loan: FHA loans are known for accommodating borrowers with lower credit scores, often accepting scores as low as 500 with a 10% down payment or 580 with a 3.5% down payment.

- Kentucky Fannie Mae Loan: Fannie Mae loans usually require a minimum credit score of 620 or higher, although some lenders may have slightly different requirements.

Kentucky Mortgage Income and Work History:

- Kentucky VA Loan: VA loans consider your stable income and employment history but may be more lenient if you have a history of military service or steady employment. 2 years of employment needed for loan application-minimal job gaps

- Kentucky USDA Loan: USDA loans often have income limits based on the area’s median income, and you need a stable income source. 2 years of employment needed for loan application-minimal job gaps

- Kentucky FHA Loan: FHA loans consider your income stability and work history, with guidelines that vary by lender. 2 years of employment needed for loan application-minimal job gaps

- Kentucky Fannie Mae Loan: Fannie Mae loans typically require a stable income and employment history, similar to conventional loans. 2 years of employment needed for loan application-minimal job gaps

Kentucky Mortgage Debt Ratio Requirements:

- Kentucky VA Loan: VA loans generally have more lenient debt-to-income (DTI) ratio requirements, often allowing for a higher DTI compared to conventional loans. VA loans can get approved on much higher debt to income ratios vs FHA, USDA and Fannie Mae loans. 65% or higher in some situations but if manual underwrite, will want the ratios closer to 41% with good residual income for VA loan. VA loans are the only type of loans that require a residual income…FHA, Fannie Mae, USDA does not have residual income requirements

- Kentucky USDA Loan: USDA loans have very strict DTI ratio limits, typically around 41% to 45% max on the backend ratio and 33% or less on the front end. By far the most restrictive on debt ratios vs FHA, VA, and Fannie Mae loans

- Kentucky FHA Loan: FHA loans also have relatively flexible DTI ratio limits (56% back end ratio possible on a AUS approval), making them accessible to borrowers with moderate levels of debt. Front end ratio max 45%

- Fannie Mae Loan: Fannie Mae loans follow standard DTI ratio guidelines similar to conventional loans. TYpically the second most restrictive on debt ratios right behind USDA loans on tighter debt to income ratio requirements, with the max back-end ratio no more than 50% –Front end ratio max 45%

Kentucky Mortgage Bankruptcy and Foreclosure Requirements:

- Kentucky VA Loan: VA loans are more forgiving of past bankruptcy or foreclosure, often requiring a waiting period of 2 years for Chapter 7 bankruptcy and 1-2 years for foreclosure.

- Kentucky USDA Loan: USDA loans have specific waiting periods after bankruptcy (3 years for Chapter 7) and foreclosure (3 years).

- Kentucky FHA Loan: FHA loans have shorter waiting periods after bankruptcy (2 years for Chapter 7) and foreclosure (3 years).

- Kentucky Fannie Mae Loan: Fannie Mae loans typically require longer waiting periods after bankruptcy (4-7 years) and foreclosure (7 years).

Advantages and Disadvantages of Kentucky VA loans, USDA, Fannie Mae and FHA:

- Kentucky VA Loan Advantages: Zero down payment, competitive interest rates, no private mortgage insurance (PMI) requirement, lenient credit and DTI ratios, and flexible eligibility criteria for veterans and active-duty service members.

- Kentucky VA Loan Disadvantages: Funding fee (although it can be rolled into the loan), limited to eligible veterans, service members, and some spouses.

- Kentucky USDA Loan Advantages: Zero down payment, lower interest rates, flexible credit requirements, and available in eligible rural areas.

- Kentucky USDA Loan Disadvantages: Limited to rural properties, income limits, and property eligibility criteria.

- Kentucky FHA Loan Advantages: Low down payment (3.5%), flexible credit requirements, competitive interest rates, and accessible to first-time homebuyers.

- Kentucky FHA Loan Disadvantages: Mortgage insurance premiums (MIP), stricter property standards, and limits on loan amounts.

- Kentucky Fannie Mae Loan Advantages: Available for a wide range of properties, competitive interest rates, and options for low down payments.

- Kentucky Fannie Mae Loan Disadvantages: Stricter credit and DTI requirements, potential for private mortgage insurance (PMI), and limited flexibility for borrowers with past financial challenges.

In summary, choosing the right loan type depends on your specific financial situation, eligibility criteria, and property location. VA loans offer excellent benefits for eligible veterans and service members, while USDA, FHA, and Fannie Mae loans provide alternatives with their own advantages and considerations.

Joel Lobb Mortgage Loan Officer

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

Website:

Website:  Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204