This article is too good not to be shared so it’s copied from The Washington Post.

When it comes to qualifying for a loan to buy a home or to refinance your mortgage, there are plenty of numbers to consider, such as your credit score and the appraised home value. Perhaps one of the most important numbers is your debt-to-income (DTI) ratio, which compares the minimum payments on all debt you must make each month with your gross monthly income.

“The DTI ratio is one of the most important considerations lenders take into account when evaluating the risk associated with a borrower taking on another payment,” says Paul Buege, president and chief operating officer of Inlanta Mortgage in Pewaukee, Wis. “The lower the DTI ratio a borrower has, the more confident the lender is about getting paid on time in the future based on the loan terms.”

The Best Kentucky Mortgage Loan Options When Looking for your first house in Kentucky Kentucky First-time Home Buyer Programs👀💯👇‼

Kentucky Mortgage Requirements for FHA, VA, USDA and Fannie Mae

FHA loan in Kentucky you will be confronted with minimum credit score requirements set forth by FHA and the lender. Even though FHA will insure the mortgage loan at a certain credit score, you will see that lenders will create “credit-overlays” to protect their risk and ask for a higher credit score.

So keep in mind when you are getting an FHA lenders will have higher credit score minimums in addition to the FHA Mortgage Insurance program.

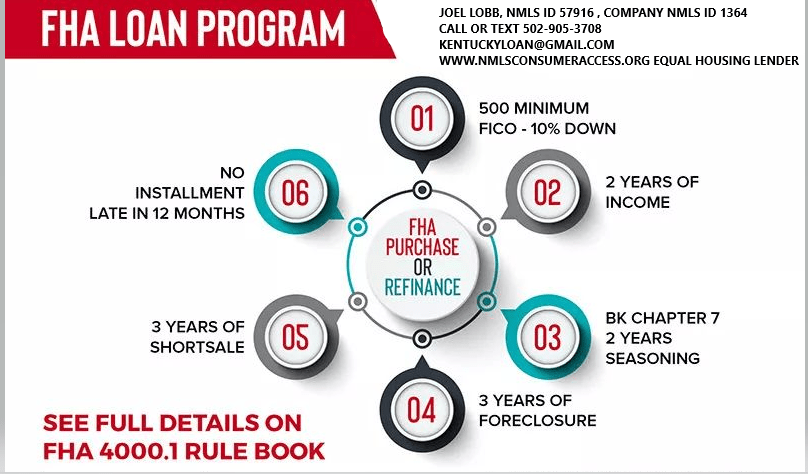

For a Kentucky Homebuyer wanting to purchase a home or refinance their existing FHA loan, FHA requires a 3.5% down payment and the borrower must have a 580 FICO Credit Score. If the score is below 580, then you would need 10% down and still qualify on a manual underwrite.

You must have a FICO score of at least 500 to be eligible for a Kentucky FHA loan. If your FICO score is from 500 to 579, your down payment on the loan is 10 percent of the loan.

If your FICO score is 580 or higher, your down payment is only 3.5 percent. If your credit score is less than 580, it may be more cost-effective to take the necessary steps to improve your score before taking out the loan, rather than putting the money into a larger down payment.

How do they get the credit score: There are three main credit bureaus in the US. Equifax, Experian, and Transunion. The three scores vary but should be relatively close as long as the same creditors are reporting to the same bureaus.

You will get a variation in the scores due to all creditors or collection companies don’t report to all three bureaus. This is why they take the mid score. So if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying credit score would be 620

Based on my experience with lenders that I deal with in Kentucky on FHA loans, most lenders require 620 middle credit score for consideration for loan approval.

How do they get the score: They take the mid score, so if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying score would be 620.

If your score is below 620, a manual underwrite is where the AUS (Automated Underwriting System) refers your loan to a human being, and they look at the entire file to see if they can overturn and approve the mortgage loan because the Desktop Underwriting Automated Software could not approve you.

With scores below 620, they typically will want to verify your rent history, have no bankruptcies in the last two years, and no foreclosures in the last 3 years.

If you have had any lates since the bankruptcy this will probably result in a denial on a refer manual underwrite file.

Your max house payment will be set at 31% of your gross monthly income, and your new house payment plus the bills you are paying on the credit report cannot be more than 43%.

Typically, on scores below 620 for FHA loans, they will also look at reserves or money you have saved up after the loan is made to try and qualify you. For example, if you have a 401k or savings account that has at least 4 months reserves (take your mortgage payment x 4) and this would equal your reserves. They look at this as a rainy day fund and could help you keep up on your bills if you were unemployed or could not work.

The first thing to keep in mind is that qualifying for a mortgage involves a lot more than just a credit score. While your FICO score is a very important ingredient, it is just one factor. Lenders also look at your income and level of debt, among other things.

A FICO score between 600 and 640 is considered fair to good credit. But keep in mind, this range of credit scores does not guarantee you will qualify for a mortgage, and if you do qualify, it won’t get you the lowest interest rate possible. Still, to buy a home aim for a score of at least 620, recognizing that other factors weigh in the decision and that some banks may require a higher score.

What credit score do you need to get a low rate mortgage?

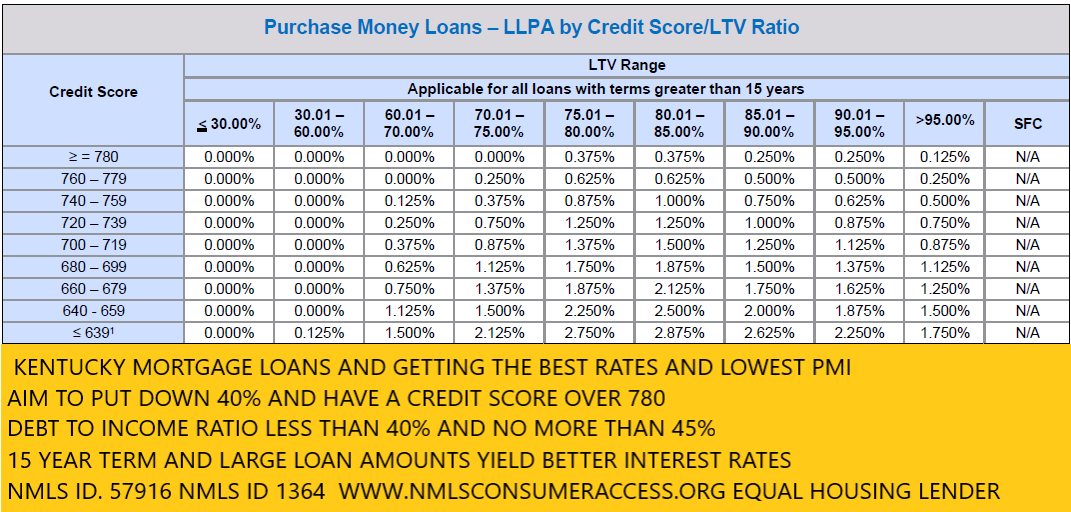

It uses to be that a score of about 720 would yield the lowest mortgage rates available. Today, the best rates kick in with a FICO score of 760. And interest rates go up significantly as your credit score drops. To give you an idea, the following table shows current rates by credit score and calculates a monthly principal and interest payment based on a $300,000 loan:

lenders will pull what they call a “tri-merge” credit report which will show three different fico scores from Transunion, Equifax, and Experian. The lenders will throw out the high and low scores and take the “middle score.” For example, if you had a 614, 610, and 629 score from the three main credit bureaus, your qualifying score would be 614.

So if you only have one score, you may not qualify. Lenders will have to pull their own credit report and scores so if you had it ran somewhere else or saw it on a website or credit card you may own, it will not matter to the lender, because they have to use their own credit report and scores.

Lastly, lenders will pull your credit report for free nowadays so this should not be a big deal as long as your scores are high enough.

offered by FHA, VA, USDA, Fannie Mae, and KHC all have their minimum fico score requirements and lenders will create overlays in addition to what the Government agencies will accept, so even if on paper FHA says they will go down to 580 or 500 in some cases on fico scores,

If you have low fico scores it may make sense to check around with different lenders to see what their minimum fico scores are for loans.

The lenders I currently deal with have the following fico cutoffs for credit scores:

As you can see, different government-backed loan programs have different minimum score requirements with most lenders for an FHA, VA, or Fannie Mae loan, and 620 is required for the no down payment programs offered by USDA and KHC in Kentucky for First Time Home Buyers wanting to go no money down.

By paying down your credit card balances (credit utilization) and having a good pay history (payment history) ,this is the best way to raise your score.

The credit bureaus don’t update immediately, so I would not add to the balance or open any new bills or have any other lender do an inquiry on your credit report while we wait for the scores to hopefully go up in the next 30 days. Try to keep everything status quo and make your payments on time and keep your balances low or lower than what is now reporting on the credit report.

How to improve your credit score!

Pay Every Single Bill on Time, or Early, Every Month

Please understand one thing; paying your bills on time each month is the single most important thing you can do to increase your credit scores.

Depending on the credit bureau, there are 4 or 5 main items that determine everyone’s credit score. Of those items, your history of paying bills makes up about 35% of the score. THIS IS HUGE!

Paying your bills on time shows lenders that you are responsible. It will also spare you from paying late fees whether it is a charge from a credit card or an added fee from your landlord.

Use a calendar, or a phone app, or some other organized system to make sure that you pay your bills on time every single month.

Another big factor in calculating a credit score is the amount of credit card debt. Credit bureaus look at two things when analyzing your credit cards.

First, they look at your available credit limit. Second, they look at the existing balance on each card. From these two figures an available ratio is developed. As the ratio goes higher, so too will your credit score increase.

Here is one simple example. Suppose a person has the following credit cards, corresponding balances, and credit limits

Credit Card

Current Balance

Credit Limit

Chase Visa

$105

$1,000

MarterCard from local bank

$236

$1,500

BP MasterCard

$87

$500

Totals

$428

$3,000

From these numbers, we get the following calculation

$428/$3,000 = 14%

In other words, the person is using 14% of their available credit and they have 86% available credit. The closer that ratio is to 100%, the better the credit score will be.

MAIN TIP: Keep all credit card balances as low as possible.In this particular example, if they had a problem with their car, or needed medical attention or some other emergency, the person would have the money necessary to handle the situation without incurring new debt. This is wise on the consumer’s part and lenders like to see this kind of money management.

Credit Cards Part 2: 1 or 2 is Better Than a Wallet Full

The previous example showed a person that utilized just three credit cards. This is much better than someone who has 5+ credit cards, all with available balances. Why? Lenders do not like to see someone that has the potential to get too far in debt in a short amount of time.

Some people have 5, 10 or more credit cards and they use many of them. This shows a lack of restraint and control. It is much better, and neater, to have only 2 or 3 cards with low rates that handle all of your transactions. A lower number of cards are easier to manage and it does not give a person the temptation to go on a huge shopping spree that could take years to payoff.

MAIN TIP: Try to limit yourself to no more than 2-3 credit cards.

Keep the Good Stuff Right Where it is

Too many people make the mistake of paying off old debts, such as old credit cards, and then closing the account. This is actually a bad idea.

A small part of the credit score is based on the length of time a person has had credit. If you have a couple of credit cards with a long track history of making payments on time and keeping the balance at a manageable level, it is a bad idea to close out the card.

Similarly, if you have been paying on a car or motorcycle for a long time, do not be in a hurry to pay off the balance. Continue to make the payments like clockwork each month.

An account that has a good record will help your scores. An account that has a good record and multiple years of use will have an even better impact on your score.

MAIN TIP: Keep old accounts open if you have a good payment history with them.

Stop Filling Out Credit Applications

Multiple credit inquiries in a short amount of time can really hurt your credit scores. Lenders view the various inquiries as someone that is desperate and possibly on the verge of making a bad financial choice.Too many people make the mistake of getting more credit after they are approved for a loan. For example, if someone is approved for a new credit card, they feel good about their finances and decide to apply for credit with a local furniture store. If they get approved for the new furniture, they may decide to upgrade their car. This requires yet another loan. They are surprised to learn that their credit score has dropped and the interest rate on the new car loan will be much higher. What happened?

If you currently have 2 or 3 credit cards along with either a car loan or a student loan, don’t apply for any more debt. Make sure the payments on your current debt are all up to date and focus on paying them all down.

In a few months of making timely payments your scores should noticeably go up.

MAIN TIP: Limit your new loans as much as possible

Which credit scores do mortgage lenders use to qualify people for a mortgage?

While it’s common knowledge that mortgage lenders use FICO scores, most people with a credit history have three FICO scores, one from each of the three national credit bureaus (Experian, Equifax, and TransUnion).

Which FICO Score is Used for Mortgages

Most lenders determine a borrower’s creditworthiness based on FICO® scores, a Credit Score developed by Fair Isaac Corporation (FICO™). This score tells the lender what type of credit risk you are and what your interest rate should be to reflect that risk. FICO scores have different names at each of the three major United States credit reporting companies. And there are different versions of the FICO formula. Here are the specific versions of the FICO formula used by mortgage lenders:

Equifax Beacon 5.0

Experian/Fair Isaac Risk Model v2

TransUnion FICO Risk Score 04

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

Which Score Gets Used?

Since most people have three FICO scores, one from each credit bureau, how do lenders choose which one to use?

For a FICO score to be considered “usable”, it must be based on adequate, concrete information. If there is too little information, or if the information is inaccurate, the FICO score may be deemed unusable for the mortgage underwriting process. Once the underwriter has determined if a score is usable or not, here’s how they decide which score(s) to use for an individual borrower:

If all three scores are different, they use the middle score

If two of the scores are the same, they use that score, regardless of whether the two repeated scores are higher or lower than the third score

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

Kentucky First-Time Home Buyer Programs 2026: Complete Guide to FHA, VA, USDA & KHC Loans

Kentucky First-Time Home Buyer Programs in 2026: Your Complete Guide to FHA, VA, USDA, Conventional, and KHC Loans

Buying your first home in Kentucky in 2026? You’re entering a market with more options than ever before. Updated loan limits, competitive interest rates, and powerful down payment assistance programs are making homeownership more accessible for Kentucky families across all 120 counties.

What are the best Kentucky homebuyer programs for 2026?

The main options for Kentucky homebuyers in 2026 include Conventional Loans, FHA Loans, VA Loans, USDA Loans, and Kentucky Housing Corporation (KHC) Down Payment Assistance programs. Each offers distinct advantages depending on your credit score, down payment savings, income level, and location.

This comprehensive guide breaks down every program, updated with 2026 loan limits, credit requirements, and qualification guidelines to help you make informed decisions about your home purchase.

Conventional Mortgage Loans in Kentucky (2026)

Conventional loans remain the most popular choice for Kentucky homebuyers with good credit and stable income. These loans are not government-backed, which means they follow stricter underwriting standards but offer significant benefits for qualified borrowers.

2026 Conventional Loan Requirements:

Credit Score: Minimum 620 (preferred 740+ for best rates)

Down Payment: As low as 3% for qualified first-time buyers; 5% for repeat buyers

Debt-to-Income Ratio (DTI): Maximum 43-50% (varies by lender and compensating factors)

2026 Loan Limits for Kentucky:

Single-Family Home: $832,750

Two-Unit Property: $1,066,000

Three-Unit Property: $1,288,750

Four-Unit Property: $1,601,750

Additional Requirements:

Work History: Two years of consistent employment in the same field or industry

Bankruptcy & Foreclosure Waiting Periods:

No foreclosure in the past 7 years

No Chapter 7 bankruptcy in the past 4 years

Chapter 13 bankruptcy allowed after 2 years of discharge with court approval

Loan-to-Value (LTV): Up to 97% for qualified first-time buyers

Private Mortgage Insurance (PMI): Required for down payments under 20%; can be canceled once you reach 20% equity

Required Documentation:

Last two years of W-2 forms

Last 30 days of pay stubs

Two years of federal tax returns (self-employed or commissioned income)

Last two months of bank statements

Tri-merge credit report from lender

Why Choose Conventional? Borrowers with credit scores of 740+ and 20% down payments often prefer conventional loans because they can avoid mortgage insurance entirely and typically secure the lowest interest rates available.

Kentucky FHA Loans (2026)

FHA loans are designed specifically for first-time homebuyers and those with lower credit scores or limited savings. Backed by the Federal Housing Administration, these loans offer the most flexible qualification guidelines of any mortgage program.

2026 FHA Loan Requirements:

Credit Score:

580+ for 3.5% down payment

500-579 for 10% down payment

Down Payment: As low as 3.5%

Debt-to-Income Ratio:

Front-End Ratio: Maximum 31% (housing costs only)

Back-End Ratio: Maximum 43-57% with compensating factors

2026 FHA Loan Limits for All Kentucky Counties:

Single-Family Home: $541,287

Two-Unit Property: $693,050

Three-Unit Property: $837,700

Four-Unit Property: $1,041,125

FHA Waiting Periods:

Foreclosure: 3 years minimum

Chapter 7 Bankruptcy: 2 years minimum

Chapter 13 Bankruptcy: 12 months of on-time payments with trustee approval

Work History Requirements:

Two years of steady employment in the same industry

Gaps exceeding 6 months in the past 2 years must be explained

Multiple job changes (3+ in 12 months) may require additional documentation

Recent college graduates can substitute education for work history

FHA Mortgage Insurance:

Upfront Premium: 1.75% of loan amount (can be financed into loan)

Annual Premium: 0.45% to 1.05% (paid monthly), based on loan amount and down payment

Required Documentation:

Same as conventional loans, plus:

12-24 months of rental payment history (if manually underwritten)

Verification of non-traditional credit (if applicable)

Why Choose FHA? Perfect for first-time buyers rebuilding credit, those with limited savings, or anyone who has experienced past financial challenges. FHA loans are more forgiving and accessible than conventional financing.

Kentucky VA Home Loans (2026)

VA loans provide unmatched benefits for eligible veterans, active-duty service members, National Guard members, Reservists, and qualifying surviving spouses. These loans eliminate major barriers to homeownership.

2026 VA Loan Benefits:

Down Payment: Zero down payment required

Mortgage Insurance: No monthly PMI required (major savings)

Credit Score: Minimum 580-620 (varies by lender)

Debt-to-Income Ratio: No maximum DTI with sufficient residual income

2026 VA Loan Limits for Kentucky:

Veterans with full entitlement have no loan limit

Partial entitlement follows conforming limits: $832,750 for single-family homes

VA Loan Requirements:

Certificate of Eligibility (COE): Required; obtain through VA website or your lender

Work History: Two years of consistent employment

Waiting Periods:

No foreclosure in the past 2 years

No Chapter 7 bankruptcy in the past 2 years

Chapter 13 bankruptcy allowed after 12 months with trustee approval

Loan-to-Value (LTV): Up to 100% for purchases; 100% for cash-out refinances

VA Funding Fee: 1.25% to 3.3% of loan amount (waived for disabled veterans)

Required Documentation:

Certificate of Eligibility (COE)

DD-214 (for veterans)

Statement of Service (for active duty)

Standard income/asset documentation

Why Choose VA? The combination of no down payment, no monthly mortgage insurance, and competitive interest rates makes VA loans the most powerful financing option available for eligible borrowers.

USDA Loans in Kentucky (2026)

USDA loans offer 100% financing for eligible rural and suburban properties throughout Kentucky. Despite the “rural” designation, many suburban areas qualify, including parts of major metro areas.

2026 USDA Loan Requirements:

Credit Score: Minimum 620 (preferred 640+ for automated approval)

Down Payment: Zero down payment required

Debt-to-Income Ratio:

Front-End: Maximum 29-32%

Back-End: Maximum 41-45% (higher with compensating factors through GUS system)

Income Limits: Must not exceed 115% of area median income (varies by county and household size)

Property Eligibility: Home must be in USDA-designated eligible area

USDA Waiting Periods:

Foreclosure: 3 years minimum

Chapter 7 Bankruptcy: 3 years minimum

Chapter 13 Bankruptcy: 12 months of on-time payments with trustee approval

USDA Guarantee Fee:

Upfront Fee: 1% of loan amount (can be financed)

Annual Fee: 0.35% (paid monthly)

Work History Requirements:

Two years of steady employment

Seasonal or temporary work may qualify with sufficient documentation

Why Choose USDA? Perfect for buyers purchasing in eligible rural or suburban areas who want 100% financing. Many Kentucky locations qualify, including areas near Louisville, Lexington, and other cities.

The Kentucky Housing Corporation offers the most comprehensive suite of programs for first-time homebuyers in the state, combining competitive interest rates with substantial down payment assistance.

KHC Down Payment Assistance Program (2026):

Assistance Amount: Up to $12,500

Structure: Second mortgage at 3.75% interest rate for 10 years

Usage: Can be used for down payment, closing costs, and prepaid expenses

Repayment: Monthly payments required; not forgivable

2026 KHC Program Options:

1. Conventional Preferred Program

Down payment as low as 3%

Available to low- to moderate-income borrowers

Private mortgage insurance required

Income limits apply (varies by county)

2. Conventional Preferred Plus 80 Program

Down payment as low as 3%

Available to higher-income borrowers (up to $181,300+ depending on county)

First-time and repeat buyers eligible

PMI required

3. Mortgage Revenue Bond (MRB) Program

Below-market interest rates

Available with FHA, VA, USDA, or Conventional loans

First-time buyer requirement (waived in targeted areas)

Maximum purchase price: $544,232

2026 KHC Income Limits (Examples):

Income limits vary by county and household size. Here are representative examples:

Jefferson County (Louisville): $95,000-$181,300 (depending on program and household size)

Fayette County (Lexington): $92,000-$176,000

Rural Counties: Generally lower limits; check with KHC-approved lender

KHC Purchase Price Limits (2026):

Maximum Purchase Price: $544,232 for most programs

Some programs have lower limits; verify with your lender

KHC Eligibility Requirements:

Must purchase primary residence in Kentucky

Property must meet KHC appraisal standards

Income and purchase price limits apply

First-time homebuyer requirement for most programs (waived in targeted areas)

Must complete homebuyer education course

Why Choose KHC? The combination of below-market interest rates and up to $12,500 in down payment assistance can save Kentucky homebuyers thousands of dollars over the life of their loan.

2026 Kentucky Welcome Home Grant

The Kentucky Welcome Home Grant is expected to return in March 2026, offering additional down payment assistance to eligible Kentucky homebuyers.

2026 Welcome Home Grant Details:

Grant Amount: To be announced (historically $7,500-$20,000)

Availability: First-come, first-served basis; funds typically depleted within weeks

Structure: Forgivable grant (not a loan)

Eligibility: Income limits and first-time buyer requirements apply

Launch Date: Expected March 2026

Important: The Welcome Home Grant consistently sells out within days of opening. Get pre-approved now and be ready to act immediately when the program launches.

Comparison: Kentucky Mortgage Loan Program Requirements (2026)

Program

Min. Credit Score

Down Payment

Max DTI

2026 Loan Limit (1-Unit)

Conventional

620

3-5%

43-50%

$832,750

FHA

580

3.5%

31/43-57%

$541,287

VA

580-620

0%

No max*

$832,750 (or unlimited)

USDA

620

0%

29/41-45%

Based on income limits

KHC Programs

Varies

3-3.5%

Varies by loan type

$544,232

*VA loans evaluate residual income rather than strict DTI limits

Step-by-Step: How to Apply for a Kentucky Home Loan in 2026

Step 1: Check Your Credit Score

Obtain free credit reports from all three bureaus

Review for errors and dispute inaccuracies

Work on improving your score if below 620

Step 2: Calculate Your Budget

Determine how much you can afford monthly

Factor in property taxes, insurance, HOA fees

Use online mortgage calculators for estimates

Step 3: Get Pre-Approved

Contact a Kentucky-licensed mortgage professional

Submit required documentation

Receive pre-approval letter (typically same-day)

Step 4: Choose Your Loan Program

Compare options based on your situation

Consider credit score, down payment, income, and location

Ask about combining KHC assistance with other programs

Step 5: Find Your Home

Work with a licensed Kentucky real estate agent

Stay within your pre-approved amount

Ensure property meets program requirements

Step 6: Submit Full Application

Complete formal loan application

Provide any additional documentation requested

Coordinate home inspection and appraisal

Step 7: Close on Your Home

Review closing disclosure carefully

Bring required funds to closing

Sign documents and receive keys

Frequently Asked Questions

Q: Can I combine KHC down payment assistance with FHA or VA loans?

A: Yes! KHC assistance can be layered with FHA, VA, USDA, or Conventional loans, making it possible to buy with minimal out-of-pocket costs.

Q: What’s the difference between the Welcome Home Grant and KHC down payment assistance?

A: The Welcome Home Grant is a forgivable grant (not repaid), while KHC down payment assistance is a second mortgage with monthly payments at 3.75% interest.

Q: Do all Kentucky counties have the same FHA loan limits?

A: Yes. For 2026, all 120 Kentucky counties use the same FHA floor limit of $541,287 for single-family homes.

Q: Can I buy a multi-unit property with these programs?

A: Yes! FHA, VA, and Conventional loans all allow 2-4 unit purchases, with the requirement that you occupy one unit as your primary residence.

Q: How long does the mortgage approval process take?

A: Pre-approval typically happens within 24 hours. Full approval to closing typically takes 30-45 days depending on the loan type and your responsiveness.

Q: What if I have student loan debt?

A: All programs allow student loan debt. Lenders will calculate either 0.5-1% of the balance or use your actual payment amount in DTI calculations.

Why Work With a Kentucky Mortgage Specialist?

Navigating multiple loan programs, down payment assistance options, and changing requirements requires expertise and local knowledge. Working with a Kentucky-licensed mortgage professional who specializes in first-time homebuyer programs ensures:

✓Accurate Pre-Approval: Same-day approvals with correct numbers

✓Program Expertise: Knowledge of all available KHC and state programs

✓Competitive Rates: Access to wholesale pricing and special programs

✓Local Market Knowledge: Understanding of Kentucky’s 120 counties

✓Personalized Service: One-on-one guidance throughout the entire process

Get Started Today

Ready to explore your Kentucky home buying options? The 2026 loan limits and programs provide more opportunities than ever for Kentucky families to achieve homeownership.

Joel Lobb

Mortgage Loan Officer – Kentucky Mortgage Loan Specialist

20+ Years Experience | 1,300+ Families Helped

NMLS Personal ID: 57916

Company NMLS ID: 1738461

Services Available:

✓ Free mortgage applications with same-day approval

✓ All 120 Kentucky counties served

✓ FHA, VA, USDA, Conventional, and KHC programs

✓ Down payment assistance guidance

✓ First-time homebuyer counseling

Equal Housing Lender | Licensed for Kentucky Mortgage Loans Only

Disclaimer: This website is not endorsed by or affiliated with the FHA, VA, USDA, or any government agency. Information provided is for educational purposes. Loan programs, rates, and requirements subject to change. All borrowers must meet program eligibility requirements.

2026 Kentucky Housing Market Outlook

Kentucky’s housing market continues to show strength in 2026, with steady home price appreciation and competitive interest rates creating favorable conditions for buyers. The increased loan limits provide greater purchasing power, while expanded down payment assistance programs make homeownership more accessible.

Whether you’re a first-time buyer, a veteran, or someone looking to purchase in a rural area, Kentucky’s diverse loan programs offer a pathway to homeownership that fits your unique financial situation.

Kentucky Mortgage Loan ExpertFHA | VA | USDA | KHC Down Payment Assistance | Fannie MaeEqual Housing Lender. This is not a commitment to lend. All loans are subject to credit approval and program requirements.

Are you a prospective homebuyer in Kentucky searching for the best mortgage lenders? Joel Lobb is a trusted mortgage broker. He has a proven track record of helping clients secure competitive mortgage rates. He also helps clients with financing options. With Joel Lobb by your side, you can access top-notch mortgage lenders in Kentucky. He will help you make your dream of homeownership a reality.

Joel Lobb has established strong relationships with a network of reputable mortgage lenders in Kentucky. These lenders offer a wide range of loan programs. These programs can suit your unique needs and financial goals. Whether you’re a first-time homebuyer, a seasoned investor, or looking to refinance your existing mortgage, Joel Lobb can connect you with the best mortgage lenders that offer:

Competitive Interest Rates: Access mortgage loans with competitive interest rates. These rates can save you money over the life of your loan.

Flexible Loan Programs: Choose from a variety of loan programs. These include FHA, VA, USDA, conventional, jumbo loans, and more. They are tailored to your specific requirements.

Personalized Guidance: Receive personalized guidance and support throughout the mortgage process. This includes steps from pre-qualification to closing. These efforts ensure a smooth and stress-free experience.

Quick and Efficient Approval: Benefit from efficient loan processing. Experience quick approval times, allowing you to close on your new home faster.

Transparent and Honest Service: Experience transparent and honest communication throughout your mortgage journey. We provide full transparency on loan terms, fees, and requirements.

When you are looking for the best mortgage lenders in Kentucky, Joel Lobb stands out. He is a trusted advisor and advocate for his clients’ best interests. With Joel Lobb’s expertise and industry knowledge, you can navigate the complex world of mortgage lending with confidence. You can achieve your homeownership goals.

Contact Joel Lobb today. Learn more about the best mortgage lenders in Kentucky. Start your journey towards owning the perfect home for you and your family.

Joel Lobb specializes in a wide array of mortgage loans, including: – **FHA Loans**: These loans are a great fit for buyers with lower credit scores or those who can afford only a minimal down payment. – **VA Loans**: Tailored for veterans and active military members, offering favorable terms with little to no down payment. – **USDA Loans**: Designed for rural home buyers, providing 100% financing options. – **KHC Loans**: In collaboration with the Kentucky Housing Corporation, these loans come with down payment assistance, making them ideal for first-time buyers.

FHA loans are a popular choice for many first-time homebuyers in Kentucky. This is due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

Credit Score Requirements:

FHA loans are known for accommodating borrowers with lower credit scores. The minimum required credit score can vary. Typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. Borrowers with credit scores between 500 and 579 might still qualify. They will need a higher down payment, usually around 10%.

Down Payment:

The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

Work History:

Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history is beneficial. It is preferable to have worked with the same employer or within the same field. This helps demonstrate financial stability and the ability to repay the loan.

Debt-to-Income Ratio (DTI):

The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income. It can go higher up to 56% with good credit scores, a large down payment, or a shorter-term loan. Lenders may also consider higher ratios in certain cases if compensating factors are present.

Bankruptcy and Foreclosure:

FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years. This is possible if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

Mortgage Term:

FHA loans offer various mortgage term options, including 15-year, 20 year, 25 year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

Occupancy: Primary residences with 1-4 units. Not for investment properties or second homes.

Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

can be used for refinances, not only for purchases.

No income limits nor property restrictions on where home is located

Can close within 30 days typically with good appraisal and title work

FHA Loan Requirements in Kentucky for Credit scores, Down payment, Debt Ratio and work history below

Requirement

Details

Credit Score

– 580+: Eligible for a 3.5% down payment. – 500-579: Requires a 10% down payment.

Down Payment

Minimum of 3.5% for qualified buyers; 10% for lower credit scores below 580 to 500 score range

Debt-to-Income Ratio (DTI)

– Ideal: 45% or lower on front end ratio or housing ratio. – Acceptable: Up to 57% with compensating factors. There are two ratios. Front end and back end with front end being maxed at 45% and the backed end ratio being 56.99% with an AUS approval. If manually underwritten, see guidelines here

Employment History

Must provide at least **2 years of consistent employment—College transcripts can supplement with a less than 2 year work history

Key Benefits of FHA Loans in Kentucky

Low Credit Score Requirements

FHA loans accept borrowers with credit scores as low as 500. However, a score of 580+ qualifies you for the lowest down payment option.

Low Down Payment Options

You can purchase a home with as little as 3.5% down if you meet credit requirements, making FHA loans more accessible than conventional loans.

Competitive Interest Rates

FHA loans typically offer rates comparable to conventional mortgages. They may even offer lower rates. This could save you money over the life of the loan.

Flexible Loan Uses

With an FHA 203(k) loan, you can bundle home purchase and renovation costs into a single mortgage.

Assumable Loans

FHA loans can be transferred to a new buyer. This feature is especially valuable if you sell your home when interest rates are higher.

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can provide valuable guidance. They offer assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

Any questions, please don’t hesitate to reach out via, text, email, or call. Advice is always free.

One of Kentucky’s highest rated mortgage loan officers for FHA, VA, USDA, Kentucky Housing KHC and conventional mortgage loans.

Evo Mortgage Company NMLS# 1738461 Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. (www.nmlsconsumeraccess.org).

Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans

Kentucky FHA Loans: Kentucky FHA loans are known for their lenient credit score requirements, making them accessible to borrowers with lower credit scores. However, a minimum score of 500 to 580 is typically required, depending on the down payment.

Kentucky VA Loans: VA loans offer flexible credit score requirements, while on paper VA states they don’t require a minimum score to insure the mortgage loan, most lenders preferring a FICO score of 620 or higher. Veterans, active-duty service members, and eligible spouses can benefit from VA loan options.

Kentucky USDA Loans: USDA loans are designed for rural homebuyers and require no minimum FICO score , but most lenders will want a credit score of 640 or higher. These loans offer zero down payment options for eligible properties.

KHC Mortgage Loans: Kentucky Housing Corporation (KHC) mortgage loans may vary in credit score requirements depending on the lender. It’s essential to work with a knowledgeable mortgage broker like Joel Lobb to understand specific lender guidelines. KHC requires a minimum 620 credit score for FHA, VA, USDA and 660 for Conventional loan programs

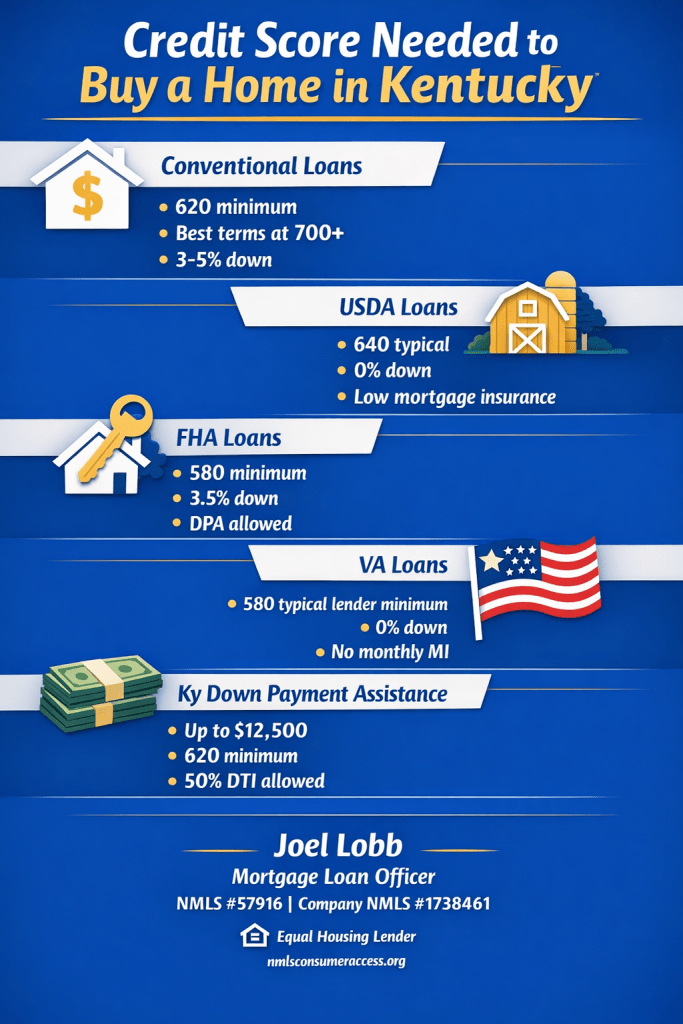

What Credit Score Do You Need to Buy a House in Kentucky?

There is no single “magic number.” The credit score needed depends on the loan program (Conventional, USDA, FHA, VA, or Kentucky Housing Corporation down payment assistance). Here’s how it works in the real world for Kentucky buyers.

Quick guide: typical credit score ranges and key highlights by Kentucky mortgage program.

Conventional Loans in Kentucky

Minimum credit score generally starts at 620.

Most lenders prefer higher scores for 3%–5% down options.

Best pricing and easier approvals are typically with strong credit (often 700+).

Mortgage insurance (PMI) usually improves as scores increase.

USDA Rural Housing Loans in Kentucky

Many lenders target around 640 for automated approval through GUS (Guaranteed Underwriting System).

Manual underwriting may be possible when automated approval is not available.

0% down payment required (eligible rural/suburban areas).

Typical fees include a 1% upfront guarantee fee and 0.35% annual fee (paid monthly).

USDA can be one of the best value options for Kentucky buyers with limited cash, provided the property is in an eligible area and the file meets income and underwriting requirements.

Kentucky FHA Loans

As low as 580 credit score with 3.5% down (typical baseline).

Gift funds, grants, and down payment assistance may be allowed.

Mortgage insurance is generally higher than USDA or VA, but rates can still be competitive.

Common waiting periods: 2 years after bankruptcy and 3 years after foreclosure (standard guideline).

Kentucky VA Loans

VA does not set a minimum credit score in its guidelines, but most lenders do.

Many VA lenders target around 580+ (lender overlay varies).

0% down and no monthly mortgage insurance.

Clear CAIVRS is required (for federal delinquency screening).

Kentucky Down Payment Assistance (KHC)

Kentucky Housing Corporation (KHC) often offers up to $12,500 down payment assistance (program terms and funding can change).

Typically structured as a second mortgage paid back over 15 years.

Minimum credit score is commonly 620 across many KHC options; KHC conventional often requires 660.

Maximum debt-to-income ratios are commonly around 50/50 (program and investor rules apply).

Next step: get a clear pre-approval target

If you share your approximate credit score range, income type, and whether you’re looking in Louisville, Lexington, or rural Kentucky, I can point you to the most realistic program and the exact score threshold that will matter for approval.

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “What credit score do I need to buy a house in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “It depends on the loan program. Conventional financing often starts around 620, USDA lenders commonly target about 640 for automated approval, FHA can allow down to 580 with 3.5% down, and many VA lenders look for around 580 even though VA does not publish a minimum score. Kentucky Housing Corporation down payment assistance commonly requires around 620 (and KHC conventional often around 660). Final approval also depends on income, debt-to-income ratio, and underwriting findings.”

}

},

{

“@type”: “Question”,

“name”: “Can I buy a home in Kentucky with a 580 credit score?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Often yes, depending on the full file. FHA commonly allows 580 with 3.5% down and can work well when you have limited savings or are using gift funds or down payment assistance. Lender overlays and underwriting results still apply.”

}

},

{

“@type”: “Question”,

“name”: “Is 640 a good credit score for a Kentucky mortgage?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “A 640 score can be workable for several programs. USDA lenders often target around 640 for automated approvals, and conventional approvals may be possible starting at 620, though terms improve as scores rise. Your debt-to-income ratio, income stability, and cash to close will strongly influence results.”

}

},

{

“@type”: “Question”,

“name”: “What credit score do I need for a USDA loan in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Many lenders prefer around 640 to obtain an automated approval through the USDA Guaranteed Underwriting System (GUS). Manual underwriting may be possible in some cases, but it is typically more restrictive on ratios and documentation.”

}

},

{

“@type”: “Question”,

“name”: “Does the VA require a minimum credit score in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “VA guidelines do not publish a minimum credit score, but lenders usually do. Many VA lenders commonly target around 580 or higher, depending on the overall file and lender overlays.”

}

},

{

“@type”: “Question”,

“name”: “What credit score is needed for Kentucky Housing Corporation (KHC) down payment assistance?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “KHC program requirements vary, but a common minimum is around 620 for many options. KHC conventional commonly requires around 660. Eligibility also depends on income limits, purchase price limits, and underwriting findings.”

}

}

]

}

What Credit Score Do You Need to Buy a House in Kentucky?

Comparing Kentucky VA loans to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky

Kentucky VA loans Compared to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky

When comparing Kentucky VA loans to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky, several factors come into play. These factors include credit score requirements, income considerations, work history, and debt ratios. They also involve how each loan type treats bankruptcy and foreclosure. Let’s delve into the benefits and differences of each loan type:

Kentucky Mortgage Credit Score Requirements:

Kentucky VA Loan: VA loans typically have more flexible credit score requirements compared to conventional loans. While there’s no specific minimum score set by VA , most Kentucky VA lenders often look for a credit score of 620 or higher. I can do VA loans down to a 580 credit score.

Kentucky USDA Loan: USDA loans also offer flexibility, with no minimum score required per USDA guidelines, but most Kentucky USDA lenders will want a 640 score or higher. I Can do Kentucky USDA loans down to a 580 credit score on a manual underwrite.

Kentucky FHA Loan: FHA loans are known for accommodating borrowers with lower credit scores, often accepting scores as low as 500 with a 10% down payment or 580 with a 3.5% down payment.

Kentucky Fannie Mae Loan: Fannie Mae loans usually require a minimum credit score of 620 or higher, although some lenders may have slightly different requirements.

Kentucky VA Loan: VA loans consider your stable income and employment history but may be more lenient if you have a history of military service or steady employment. 2 years of employment needed for loan application-minimal job gaps

Kentucky USDA Loan: USDA loans often have income limits based on the area’s median income, and you need a stable income source. 2 years of employment needed for loan application-minimal job gaps

Kentucky FHA Loan: FHA loans consider your income stability and work history, with guidelines that vary by lender. 2 years of employment needed for loan application-minimal job gaps

Kentucky Fannie Mae Loan: Fannie Mae loans typically require a stable income and employment history, similar to conventional loans. 2 years of employment needed for loan application-minimal job gaps

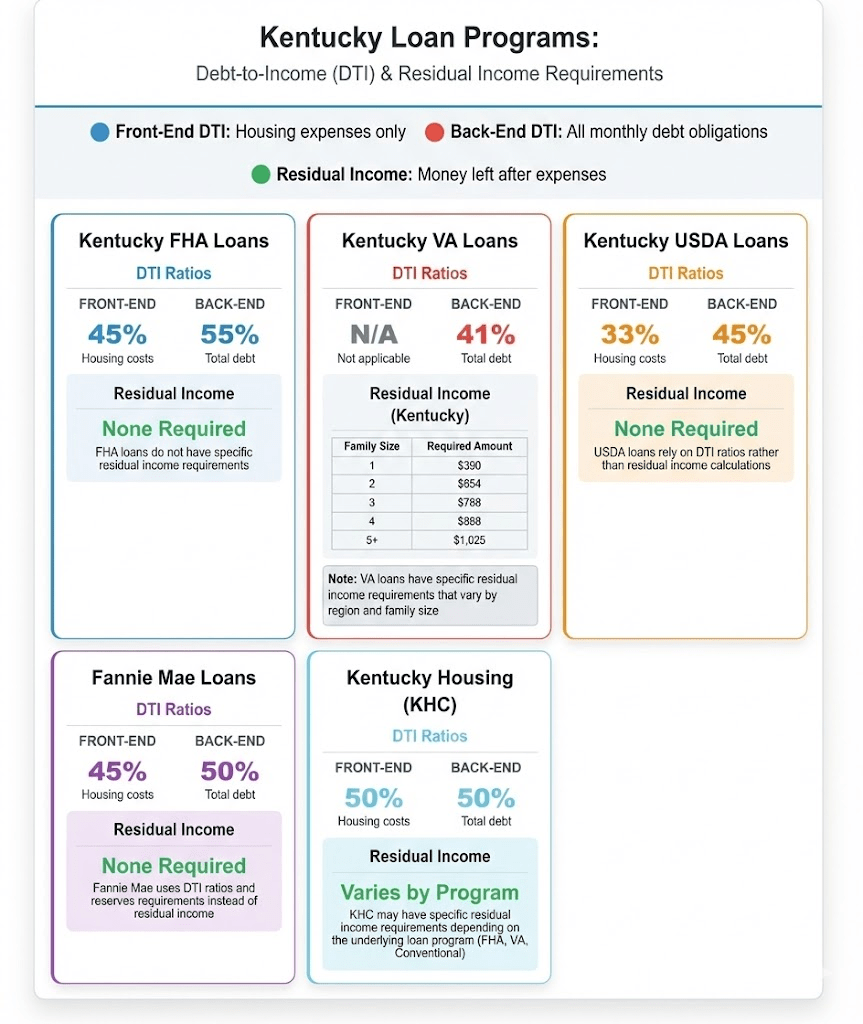

Kentucky VA Loan: VA loans generally have more lenient debt-to-income (DTI) ratio requirements, often allowing for a higher DTI compared to conventional loans. VA loans can get approved on much higher debt to income ratios vs FHA, USDA and Fannie Mae loans. 65% or higher in some situations but if manual underwrite, will want the ratios closer to 41% with good residual income for VA loan. VA loans are the only type of loans that require a residual income…FHA, Fannie Mae, USDA does not have residual income requirements

Kentucky USDA Loan: USDA loans have very strict DTI ratio limits, typically around 41% to 45% max on the backend ratio and 33% or less on the front end. By far the most restrictive on debt ratios vs FHA, VA, and Fannie Mae loans

Kentucky FHA Loan: FHA loans also have relatively flexible DTI ratio limits (56% back end ratio possible on a AUS approval), making them accessible to borrowers with moderate levels of debt. Front end ratio max 45%

Fannie Mae Loan: Fannie Mae loans follow standard DTI ratio guidelines similar to conventional loans. TYpically the second most restrictive on debt ratios right behind USDA loans on tighter debt to income ratio requirements, with the max back-end ratio no more than 50% –Front end ratio max 45%

Kentucky VA Loan: VA loans are more forgiving of past bankruptcy or foreclosure, often requiring a waiting period of 2 years for Chapter 7 bankruptcy and 1-2 years for foreclosure.

Kentucky USDA Loan: USDA loans have specific waiting periods after bankruptcy (3 years for Chapter 7) and foreclosure (3 years).

Kentucky FHA Loan: FHA loans have shorter waiting periods after bankruptcy (2 years for Chapter 7) and foreclosure (3 years).

Kentucky Fannie Mae Loan: Fannie Mae loans typically require longer waiting periods after bankruptcy (4-7 years) and foreclosure (7 years).

Advantages and Disadvantages of Kentucky VA loans, USDA, Fannie Mae and FHA:

Kentucky VA Loan Advantages: Zero down payment, competitive interest rates, no private mortgage insurance (PMI) requirement, lenient credit and DTI ratios, and flexible eligibility criteria for veterans and active-duty service members.

Kentucky VA Loan Disadvantages: Funding fee (although it can be rolled into the loan), limited to eligible veterans, service members, and some spouses.

Kentucky USDA Loan Advantages: Zero down payment, lower interest rates, flexible credit requirements, and available in eligible rural areas.

Kentucky USDA Loan Disadvantages: Limited to rural properties, income limits, and property eligibility criteria.

Kentucky FHA Loan Advantages: Low down payment (3.5%), flexible credit requirements, competitive interest rates, and accessible to first-time homebuyers.

Kentucky FHA Loan Disadvantages: Mortgage insurance premiums (MIP), stricter property standards, and limits on loan amounts.

Kentucky Fannie Mae Loan Advantages: Available for a wide range of properties, competitive interest rates, and options for low down payments.

Kentucky Fannie Mae Loan Disadvantages: Stricter credit and DTI requirements, potential for private mortgage insurance (PMI), and limited flexibility for borrowers with past financial challenges.

In summary, choosing the right loan type depends on your specific financial situation, eligibility criteria, and property location. VA loans offer excellent benefits for eligible veterans and service members, while USDA, FHA, and Fannie Mae loans provide alternatives with their own advantages and considerations.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Click here to apply for Free Info & Homebuyer Advice →

Click here to apply for Free Info & Homebuyer Advice →

Email –

Email – Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome