Joel Lobb specializes in a wide array of mortgage loans, including:

– **FHA Loans**: These loans are a great fit for buyers with lower credit scores or those who can afford only a minimal down payment.

– **VA Loans**: Tailored for veterans and active military members, offering favorable terms with little to no down payment.

– **USDA Loans**: Designed for rural home buyers, providing 100% financing options.

– **KHC Loans**: In collaboration with the Kentucky Housing Corporation, these loans come with down payment assistance, making them ideal for first-time buyers.

Complete Guide to FHA Loan Requirements in Kentucky

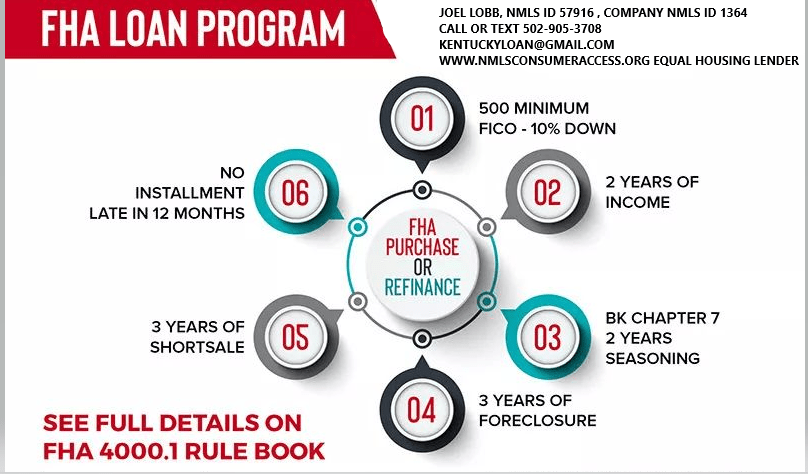

FHA loans are a popular choice for many first-time homebuyers in Kentucky. This is due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

- Credit Score Requirements:

- FHA loans are known for accommodating borrowers with lower credit scores. The minimum required credit score can vary. Typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. Borrowers with credit scores between 500 and 579 might still qualify. They will need a higher down payment, usually around 10%.

- Down Payment:

- The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

- Work History:

- Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history is beneficial. It is preferable to have worked with the same employer or within the same field. This helps demonstrate financial stability and the ability to repay the loan.

- Debt-to-Income Ratio (DTI):

- The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income. It can go higher up to 56% with good credit scores, a large down payment, or a shorter-term loan. Lenders may also consider higher ratios in certain cases if compensating factors are present.

- Bankruptcy and Foreclosure:

- FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years. This is possible if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

- Mortgage Term:

- FHA loans offer various mortgage term options, including 15-year, 20 year, 25 year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

- Occupancy: Primary residences with 1-4 units. Not for investment properties or second homes.

- Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

- can be used for refinances, not only for purchases.

- No income limits nor property restrictions on where home is located

- Can close within 30 days typically with good appraisal and title work

FHA Loan Requirements in Kentucky for Credit scores, Down payment, Debt Ratio and work history below

| Requirement | Details |

|---|---|

| Credit Score | – 580+: Eligible for a 3.5% down payment. – 500-579: Requires a 10% down payment. |

| Down Payment | Minimum of 3.5% for qualified buyers; 10% for lower credit scores below 580 to 500 score range |

| Debt-to-Income Ratio (DTI) | – Ideal: 45% or lower on front end ratio or housing ratio. – Acceptable: Up to 57% with compensating factors. There are two ratios. Front end and back end with front end being maxed at 45% and the backed end ratio being 56.99% with an AUS approval. If manually underwritten, see guidelines here |

| Employment History | Must provide at least **2 years of consistent employment—College transcripts can supplement with a less than 2 year work history |

Key Benefits of FHA Loans in Kentucky

- Low Credit Score Requirements

- FHA loans accept borrowers with credit scores as low as 500. However, a score of 580+ qualifies you for the lowest down payment option.

- Low Down Payment Options

- You can purchase a home with as little as 3.5% down if you meet credit requirements, making FHA loans more accessible than conventional loans.

- Competitive Interest Rates

- FHA loans typically offer rates comparable to conventional mortgages. They may even offer lower rates. This could save you money over the life of the loan.

- Flexible Loan Uses

- With an FHA 203(k) loan, you can bundle home purchase and renovation costs into a single mortgage.

- Assumable Loans

- FHA loans can be transferred to a new buyer. This feature is especially valuable if you sell your home when interest rates are higher.

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can provide valuable guidance. They offer assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

Any questions, please don’t hesitate to reach out via, text, email, or call. Advice is always free.

One of Kentucky’s highest rated mortgage loan officers for FHA, VA, USDA, Kentucky Housing KHC and conventional mortgage loans.

1 –  Email – kentuckyloan@gmail.com

Email – kentuckyloan@gmail.com

Email – kentuckyloan@gmail.com 2.  Call/Text – 502-905-3708

Call/Text – 502-905-3708

Call/Text – 502-905-3708Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com

Website: www.mylouisvillekentuckymortgage.com Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

(www.nmlsconsumeraccess.org).

(www.nmlsconsumeraccess.org).

Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans

MINIMUM CREDIT SCORES REQUIRED FOR KENTUCKY FHA, VA, USDA MORTGAGE LOANS

-

Kentucky FHA Loans: Kentucky FHA loans are known for their lenient credit score requirements, making them accessible to borrowers with lower credit scores. However, a minimum score of 500 to 580 is typically required, depending on the down payment.

-

Kentucky VA Loans: VA loans offer flexible credit score requirements, while on paper VA states they don’t require a minimum score to insure the mortgage loan, most lenders preferring a FICO score of 620 or higher. Veterans, active-duty service members, and eligible spouses can benefit from VA loan options.

-

Kentucky USDA Loans: USDA loans are designed for rural homebuyers and require no minimum FICO score , but most lenders will want a credit score of 640 or higher. These loans offer zero down payment options for eligible properties.

-

KHC Mortgage Loans: Kentucky Housing Corporation (KHC) mortgage loans may vary in credit score requirements depending on the lender. It’s essential to work with a knowledgeable mortgage broker like Joel Lobb to understand specific lender guidelines. KHC requires a minimum 620 credit score for FHA, VA, USDA and 660 for Conventional loan programs

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

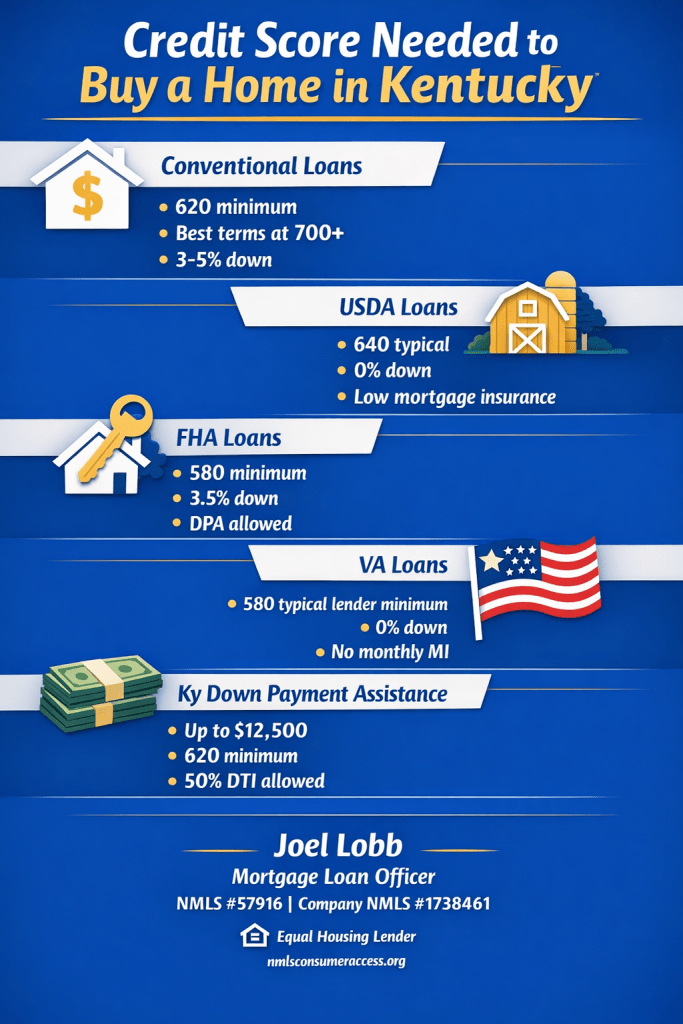

Credit Score Requirements for Kentucky Home Buyers

What Credit Score Do You Need to Buy a House in Kentucky?

There is no single “magic number.” The credit score needed depends on the loan program (Conventional, USDA, FHA, VA, or Kentucky Housing Corporation down payment assistance). Here’s how it works in the real world for Kentucky buyers.

Conventional Loans in Kentucky

- Minimum credit score generally starts at 620.

- Most lenders prefer higher scores for 3%–5% down options.

- Best pricing and easier approvals are typically with strong credit (often 700+).

- Mortgage insurance (PMI) usually improves as scores increase.

USDA Rural Housing Loans in Kentucky

- Many lenders target around 640 for automated approval through GUS (Guaranteed Underwriting System).

- Manual underwriting may be possible when automated approval is not available.

- 0% down payment required (eligible rural/suburban areas).

- Typical fees include a 1% upfront guarantee fee and 0.35% annual fee (paid monthly).

USDA can be one of the best value options for Kentucky buyers with limited cash, provided the property is in an eligible area and the file meets income and underwriting requirements.

Kentucky FHA Loans

- As low as 580 credit score with 3.5% down (typical baseline).

- Gift funds, grants, and down payment assistance may be allowed.

- Mortgage insurance is generally higher than USDA or VA, but rates can still be competitive.

- Common waiting periods: 2 years after bankruptcy and 3 years after foreclosure (standard guideline).

Kentucky VA Loans

- VA does not set a minimum credit score in its guidelines, but most lenders do.

- Many VA lenders target around 580+ (lender overlay varies).

- 0% down and no monthly mortgage insurance.

- Clear CAIVRS is required (for federal delinquency screening).

Kentucky Down Payment Assistance (KHC)

- Kentucky Housing Corporation (KHC) often offers up to $12,500 down payment assistance (program terms and funding can change).

- Typically structured as a second mortgage paid back over 15 years.

- Minimum credit score is commonly 620 across many KHC options; KHC conventional often requires 660.

- Maximum debt-to-income ratios are commonly around 50/50 (program and investor rules apply).

Next step: get a clear pre-approval target

If you share your approximate credit score range, income type, and whether you’re looking in Louisville, Lexington, or rural Kentucky, I can point you to the most realistic program and the exact score threshold that will matter for approval.

Bad Credit Kentucky Mortgage

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

2026 Kentucky FHA Loan Guide: Benefits & Updates

Kentucky FHA Loan Guide 2026: Limits, Gift Funds, KHC Down Payment Help, and Welcome Home Grant

Buying a home in Kentucky in 2026? This guide breaks down the FHA loan limit, gift fund rules, KHC down payment assistance, and the Welcome Home Grant in a clean, mobile-friendly format with no scripts.

2026 FHA limit: $541,287

3.5% down with 580+

KHC DAP up to $12,500

Welcome Home opens April 6, 2026

If you are a Kentucky first-time home buyer, or even a repeat buyer looking for a low down payment option, FHA financing remains one of the strongest mortgage programs available in 2026. FHA works well for many buyers because it allows a lower down payment, flexible credit guidelines, and in many cases the ability to combine with down payment assistance.

On top of that, Kentucky buyers may also be able to use Kentucky Housing Corporation down payment assistance or the Welcome Home Grant to reduce cash needed at closing. When the loan is structured correctly, that can make the difference between buying now and waiting another year.

2026 Kentucky FHA quick update

The 2026 FHA one-unit loan limit in Kentucky is $541,287. KHC continues offering up to $12,500 in Regular DAP. The Welcome Home Program opens April 6, 2026 at 8:00 a.m. ET. Gift fund documentation is cleaner than it used to be, but large deposits still need to be documented properly.

2026 Kentucky FHA Loan Highlights

$541,287

2026 FHA loan limit

Standard one-unit Kentucky FHA limit

3.5%

Minimum FHA down payment

For borrowers with a 580 or higher credit score

580

Typical minimum score for 3.5% down FHA

Lower scores may require more money down

$12,500

KHC Regular DAP

Repayable over 15 years at 4.75%

$10,000–$20,000

Welcome Home assistance

Grant funds available through participating lenders while funds last

FHA Gift Funds and Large Deposits in 2026

One of the biggest advantages for FHA borrowers today is that gift fund documentation is cleaner than it used to be. That matters because many Kentucky buyers rely on family help for down payment or closing costs.

Even with that improvement, large deposits still matter. If a deposit is unusually large compared to your monthly qualifying income, underwriting will usually require an explanation and documentation showing where the money came from.

The bottom line is simple: gift funds can absolutely help, but the file still needs to be documented the right way from the start.

KHC Down Payment Assistance 2026

The Kentucky Housing Corporation loan program remains one of the best tools available for Kentucky buyers who need help with down payment and closing costs.

How KHC helps FHA buyers

KHC Regular DAP can be paired with an eligible KHC first mortgage. For borrowers who qualify, that can help cover some or all of the FHA down payment and part of the closing costs.

This is especially useful for buyers who have the income to qualify but do not have a large amount of liquid cash saved. That is a common issue, and KHC helps address it directly.

Regular DAP is offered up to $12,500 and is repaid over 15 years at 4.75 percent.

Basic KHC eligibility points

- You must use an eligible KHC first mortgage program.

- You must meet KHC credit score requirements.

- You must stay within applicable income and purchase price limits.

- The home must be a primary residence.

- Program overlays and lender guidelines still apply.

Welcome Home Grant 2026

Separate from KHC

The Welcome Home Program is separate from KHC down payment assistance. A lot of buyers mix those up, but they are not the same program and they do not operate the same way.

The Welcome Home Program opens April 6, 2026 at 8:00 a.m. Eastern Time. Funds are first-come, first-served, so serious buyers need to be fully pre-approved and ready before the window opens.

- Program opens April 6, 2026

- Opening time is 8:00 a.m. ET

- Potential grant range is generally $10,000 to $20,000

- Available through participating lenders

- Income, occupancy, and program rules apply

- Funds can run out quickly

Official program information: FHLB Cincinnati Welcome Home Program

Internal Links to Related Kentucky Loan Programs

- Kentucky FHA Loans

- Kentucky USDA Rural Housing Loans

- Kentucky VA Mortgage Loans

- KHC Down Payment Assistance and KHC Loans

- Apply for a Kentucky Mortgage Pre-Approval

Official External Resources

- HUD FHA Mortgage Limits Lookup

- HUD 2026 FHA Loan Limit Announcement

- Kentucky Housing Corporation Down Payment Assistance

- FHLB Cincinnati Welcome Home Program

- AnnualCreditReport.com

How to Buy a House in Kentucky with an FHA Loan

1. Review your credit

Know where your mortgage scores stand before you start shopping.

2. Get pre-approved

Review your credit, income, assets, and employment up front so the right loan structure is clear from the beginning.

3. Review assistance options

Do not stop at FHA only. Check KHC and Welcome Home eligibility at the same time.

4. Gather documents early

Have pay stubs, W-2s, bank statements, ID, and documentation for any unusual deposits ready early.

5. Structure the offer correctly

Seller concessions, program fit, and property eligibility all matter before contract execution.

6. Move through underwriting and closing

Clean files close faster. Disorganized files do not.

Ready to Buy a Home in Kentucky?

Get a straight answer on your FHA, KHC, USDA, or VA options and find out which loan structure fits your situation best.

Frequently Asked Questions

What is the Kentucky FHA loan limit for 2026?

The standard one-unit FHA loan limit for Kentucky in 2026 is $541,287.

How much is KHC down payment assistance in 2026?

KHC Regular DAP is offered up to $12,500 and is repayable over 15 years at 4.75 percent for eligible borrowers.

When does the Welcome Home Program open in 2026?

The 2026 Welcome Home Program opens April 6, 2026 at 8:00 a.m. Eastern Time.

Can I use gift funds on an FHA loan?

Yes. FHA allows gift funds, but they still have to be documented properly for underwriting.

Which is better in Kentucky: FHA, USDA, VA, or KHC?

That depends on your credit, income, location, veteran status, and cash available. The right answer is the loan structure that gives you the best overall execution, not just the one with the most familiar name.

Disclaimer: This information is for educational purposes only and is not a commitment to lend. All loans are subject to credit approval, income verification, asset review, and property approval. Program guidelines, rates, limits, and eligibility can change. Equal Housing Lender.

Kentucky first time home buyer loan requirements

Buying your first house in Kentucky involves several steps, which can vary depending on the type of loan program you choose. Here’s a detailed guide on the steps and requirements for various Kentucky First Time Home Buyer loan programs:

1. Kentucky FHA Loans

Credit Score:

- Minimum credit score typically required is 580 for 3.5% down payment.

- Scores between 500-579 may qualify with a 10% down payment.

Income:

- Stable and sufficient income to cover the mortgage payments.

Work History:

- At least 2 years of consistent employment history.

Down Payment:

- 3.5% of the purchase price if the credit score is 580 or higher.

FICO Score:

- Minimum FICO score of 580 for maximum financing.

Bankruptcy and Foreclosure:

- Chapter 7 bankruptcy: 2 years from discharge with reestablished good credit.

- Chapter 13 bankruptcy: 1 year of the payout period with satisfactory payment history.

- Foreclosure: 3 years from completion date.

Debt Ratio:

- Typically, a maximum debt-to-income (DTI) ratio of 56.9% on backend and 45% on the front end debt ratio.

Collections:

- Must be addressed if they affect the borrower’s ability to repay the loan. Collections not required to be paid but must count in debt to income ratio sometimes if aggregate total on credit report is over $1000 total…Non-medical bills only, medical bills don’t count and usually not required to be paid or figure a payment unless you have a judgement of garnishment against your paystubs.

Mortgage Insurance:

- Required for all FHA loans. Includes an upfront mortgage insurance premium (UFMIP) and monthly mortgage insurance premiums (MIP).

Time to Close:

- Approximately 30-45 days.

Appraisal Requirements:

- Property must meet minimum property standards set by HUD.

Mortgage Documents Needed for Pre-Approval Letter in Kentucky to Buy a House using a Kentucky FHA loan:

- Proof of income (pay stubs, last two years W-2s, tax returns).

- Proof of employment. Last two years

- Proof of assets (last two bank statements). 401k or retirement account and stocks and bonds.

- Kentucky Mortgage Credit report for all three credit bureaus Experian, Equifax and Transunion

2. Kentucky USDA Rural Housing Loans

Credit Score:

- Minimum credit score of 640 is preferred for automated underwriting. No minimum score required.

- Scores below 640 may qualify with manual underwriting down to a 580 credit score

Income:

- Must meet USDA income eligibility guidelines (typically low to moderate income). 2 year history of income.

Work History:

- Stable employment history, usually for the past 2 years.

Down Payment:

- No down payment required (100% financing).

FICO Score:

- Minimum FICO score of 640 for automated underwriting. can go down to 580 possible

Bankruptcy and Foreclosure:

- Chapter 7 bankruptcy: 3 years from discharge.

- Chapter 13 bankruptcy: 1 year of the payout period with satisfactory payment history.

- Foreclosure: 3 years from completion date.

Debt Ratio:

- Typically, 33% for housing expenses and 45% for total DTI.

Collections:

- Must be resolved if they impact the ability to repay the loan. Collections typically don’t have to be paid but may have to count a payment in your debt to income ratio if aggregate is over 1k and non-medical

Mortgage Insurance:

- Annual fee and upfront guarantee fee. Currently 1% upfront and .35% month

Time to Close:

- Approximately 30-45 days, including USDA processing time.

Appraisal Requirements:

- Must meet HUD FHA standards.

Mortgage Documents Needed for Pre-Approval:

- Proof of income (pay stubs, last two years W-2s, tax returns).

- Proof of employment. Last two years

- Proof of assets (last two bank statements). 401k or retirement account and stocks and bonds.

- Kentucky Mortgage Credit report for all three credit bureaus Experian, Equifax and Transunion

3. Kentucky VA Home Loan

Credit Score:

- No minimum credit score requirement by the VA, but lenders typically require a score of 620.

Income:

- Sufficient income to cover mortgage payments and other obligations.

Work History:

- Stable employment, usually for the past 2 years.

Down Payment:

- No down payment required (100% financing).

FICO Score:

- Typically, a minimum FICO score of 620.

Bankruptcy and Foreclosure:

- Chapter 7 bankruptcy: 2 years from discharge.

- Chapter 13 bankruptcy: 1 year of the payout period with satisfactory payment history.

- Foreclosure: 2 years from completion date.

Debt Ratio:

- Typically, a maximum DTI ratio of 41%.

Collections:

- Must be resolved if they impact the ability to repay the loan.

Mortgage Insurance:

- No mortgage insurance, but a VA funding fee is required.

Time to Close:

- Approximately 30-45 days.

Appraisal Requirements:

- Property must meet VA Minimum Property Requirements (MPRs).

Mortgage Documents Needed for Pre-Approval:

Advertisement

- Certificate of Eligibility (COE).

- Credit report.

- Proof of income (pay stubs, last two years W-2s, tax returns).

- Proof of employment. Last two years

- Proof of assets (last two bank statements). 401k or retirement account and stocks and bonds.

- Kentucky Mortgage Credit report for all three credit bureaus Experian, Equifax and Transunion

4. Kentucky Down Payment Assistance Loans

Credit Score:

- Varies depending on the program; typically, a minimum of 580 for some programs and with KHC it requires a 620 score. .

Income:

- Must meet specific program income limits.

Work History:

- Stable employment history. Last two years

Down Payment:

- Assistance provided to cover down payment and closing costs. 25k welcome home grant, 10k down payment assistance loan from KHC and 5% grant used available toward closing costs and down payment

FICO Score:

- Minimum FICO score requirement varies by program.

Bankruptcy and Foreclosure:

- Varies by program.

Debt Ratio:

- Typically aligns with Kentucky FHA, VA, or USDA requirements.

Collections:

- Must be addressed if they impact the ability to repay the loan.

Mortgage Insurance:

- Depends on the primary loan program (FHA, VA, USDA).

Time to Close:

- Approximately 45-60 days.

Appraisal Requirements:

- Must meet the requirements of the primary loan program.

Mortgage Documents Needed for Pre-Approval:

- Proof of income (pay stubs, W-2s, tax returns).

- Proof of employment.

- Proof of assets (bank statements).

- Credit report.

5. 100% Financing Loans in Kentucky

Credit Score:

- Varies depending on the program; typically, a minimum of 620-640.

Income:

- Must meet specific program income limits.

Work History:

- Stable employment history.

Down Payment:

- No down payment required (100% financing).

FICO Score:

- Minimum FICO score requirement varies by program.

Bankruptcy and Foreclosure:

- Varies by program; typically 2-3 years from discharge or completion.

Debt Ratio:

- Varies by program, typically around 41-45%.

Collections:

- Must be addressed if they impact the ability to repay the loan.

Mortgage Insurance:

- Depends on the primary loan program (FHA, VA, USDA).

Time to Close:

- Approximately 30-45 days.

Appraisal Requirements:

- Must meet the requirements of the primary loan program.

Mortgage Documents Needed for Pre-Approval:

- Proof of income (pay stubs, W-2s, tax returns).

- Proof of employment.

- Proof of assets (bank statements).

- Credit report.

General Steps for Buying Your First Home in Kentucky

- Check Your Credit Score:

- Obtain a copy of your credit report and check your credit score.

- Determine Your Budget:

- Use a mortgage calculator to estimate your monthly payments and determine a comfortable budget.

- Get Pre-Approved:

- Contact a mortgage lender to get pre-approved for a loan. Provide necessary documents for income, employment, and assets.

- Choose a Real Estate Agent:

- Select a knowledgeable real estate agent to help you find a home that meets your needs and budget.

- Start House Hunting:

- Visit properties, attend open houses, and narrow down your choices.

- Make an Offer:

- Once you find a home, work with your real estate agent to make a competitive offer.

- Home Inspection:

- Hire a professional inspector to check the condition of the home.

- Finalize Your Loan:

- Work with your lender to finalize the loan application and submit all required documents.

- Appraisal:

- The lender will order an appraisal to determine the home’s value.

- Closing:

- Review and sign all closing documents. Pay any remaining closing costs and receive the keys to your new home.

Following these steps and meeting the specific requirements of your chosen loan program will help you successfully purchase your first home in Kentucky.

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574