Just like the gas prices at the pump, mortgage rates can change daily or throughout the day. Typically mortgage rates are published at 10-11 am daily by most lenders and you can lock up through the close of business which is usually around 6-7 PM. Mortgage rates can change up or down throughout the day based on various financial, economics, and geopolitical news in the US Financial markets and World markets. Generally speaking, good economic news is bad for rates and vice versa, bad economic news is good for mortgage rates.

The good news is this: Once you find a home and get it under contract, you can lock your mortgage loan rate. Typically it takes about 30-45 days to close a mortgage loan in Kentucky, so the typical lock is for 30-60 days. If rates get better you may be able to negotiate a better rate with your lender, but they usually have to improve by at least 25 basis points (.25) to do that. Not all lenders offer this option. The longer you lock the loan, the greater the costs. It is usually free to lock in a loan for up to 90 days without having to pay a fee.

What a lot of lenders are experiencing now is that some loans don’t close on time for various reasons. You can always extend the lock on the loan but it will costs you usually .125 basis points to do so. If you let the lock expire on the loan, then you have to take worse case pricing on that day when you go to relock. It is usually best to extend the lock on your loan.

2. What kind of Credit Score Do I need to qualify?

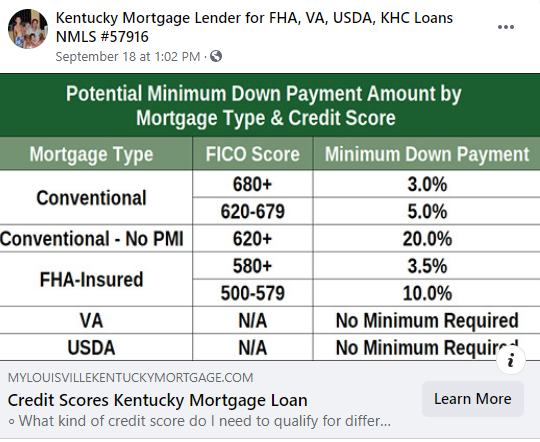

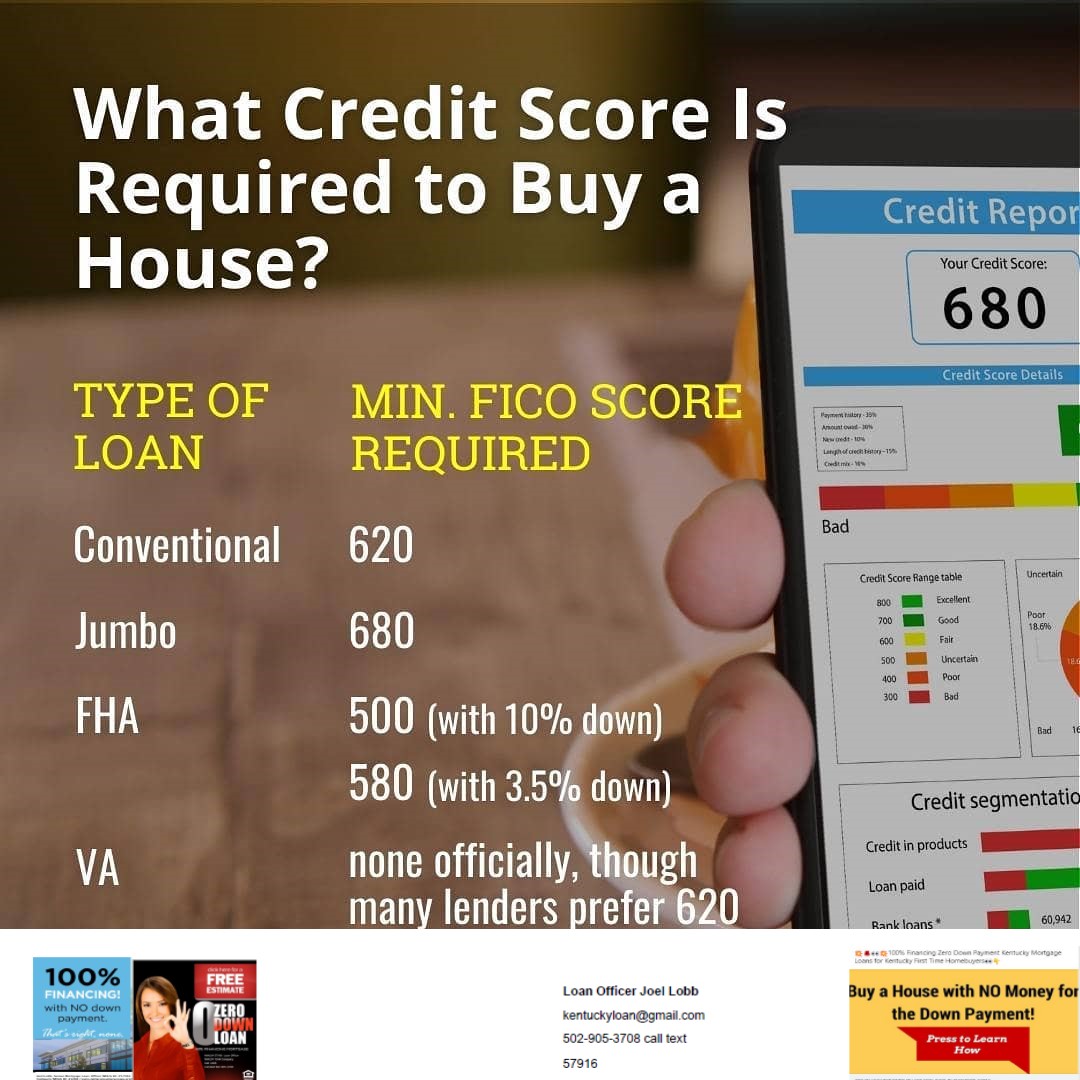

When applying for a mortgage loan, lenders will pull what they call a “tri-merge” credit report which will show three different fico scores from Trans union, Equifax, and Experian. The lenders will throw out the high and low score and take the “middle score” For example, if you had a 614, 610, and 629 score from the three main credit bureaus, your qualifying score would be 614. Most lenders will want at least two scores. So if you only have one score, you may not qualify. Lenders will have to pull their own credit report and scores so if you had it ran somewhere else or saw it on a website or credit card you may own, it will not matter to the lender, because they have to use their own credit report and scores. Most lenders will pull your credit report for free nowadays so this should not be a big deal as long as your scores are high enough. The Secondary Market of Mortgage loans offered by FHA, VA, USDA, Fannie Mae, and KHC all have their minimum fico score requirements and lenders will create overlays in addition to what the Government agencies will accept, so even if on paper FHA says they will go down to 580 or 500 in some cases on fico scores, very few lenders will go below the 620 threshold. If you have low fico scores it may make sense to check around with different lenders to see what their minimum fico scores are for loans. The lenders I currently deal with have the following fico cutoffs for credit scores: FHA–580 minimum score VA—-580 minimum score Fannie Mae–620 minimum score USDA–620 minimum score KHC with Down Payment Assistance –620 minimum score.

As you can see, 580-620 is the minimum score with most lenders for a FHA, VA, or Fannie Mae loan, is required for the no down payment programs offered by USDA for Kentucky for First Time Home Buyers wanting to go no money down.

3. What are the down payment requirements?

The most popular programs for Kentucky First Time Home Buyers usually involves one of the following housing programs outlined in bold below: FHA:

FHA will allow a home buyer to purchase a house with as little as 3.5% down. If your credit scores are low, say 680 and below, a lot of times it makes sense to go FHA because everyone pays the same mortgage insurance premiums no matter what your score is, and the down payment can be gifted to you. Meaning you really don’t have to have any skin into the game when it comes to down payment.

They even allow down payment assistance for down payment requirements of 3.5% through eligible parties like Kentucky Housing, Welcome Home Grants and Louisville KY and Covington Kentucky Down Payment Grants.

Lastly, FHA will allow for higher debt to income ratios with sometimes getting loan pre-approvals up to 55% of your total gross monthly income. So if you have a debt to income ratio of over 50%, Fannie Mae will not do the loan and USDA usually likes their debt to income ratios no more than 45%.

Think back to the last time you financed a purchase — be it a home, automobile, or what have you… You may remember having heard the term “debt-to-income ratio.” Today I want to spend some time going over exactly what this ratio is, and to also touch on how it can effect your personal finances.

4. What is your debt-to-income ratio?

Commonly referred to as your “DTI,” your debt-to-income ratio is a personal finance benchmark that relates your monthly debt payments to your monthly gross income. As an example… Let’s say that your gross monthly salary is $5,000 and you are spending $2,800 of it toward monthly debt payments. In that case, your DTI would be an unhealthy 56%. This version of your DTI is sometimes referred to as your “back-end” DTI. This is often broken down further to give a front-end debt-to-income ratio, which is a component of your back-end DTI.

How to calculate your front-end DTI for a Kentucky Mortgage Loan Approval

Your front-end DTI is calculated by dividing your monthly housing costs by your monthly gross income. Front-end DTI for renters is simply the amount paid in rent, whereas for homeowners it is the sum of mortgage principal, interest, property taxes, and home insurance (i.e., your PITI) divided by gross monthly income.

From above, if that $2,800 in debt payments is attributable to $1,500 in housing costs and $1,300 in non-housing costs, then your front-end DTI is $1,500/$5,000 = 30% (and your back-end ratio is still 56%, as calculated above). Fannie Mae: Fannie Mae requires just 3% down with their new Home Possible Program, but if you use their traditional mortgage loan, then 5% is the Fannie Mae Standard. Fannie Mae will go down 620 score, but if your scores are below 680, I would look seriously at the FHA loan program because Fannie Mae has steep increases to the interest rate and the mortgage insurance premiums if your scores are low. A couple of good things about Fannie Mae is that you can buy a larger priced home and have a large loan amount due to FHA only allowing most Kentucky Home Buyers a maximum mortgage loan amount of $356,000 for a max FHA loan and $545,000 for Fannie Mae Conventional loans in Kentucky for 2020. Lastly when it comes to mortgage insurance, FHA mortgage insurance premiums are for life of loan while Fannie Mae mortgage insurance premiums drop off when you develop 80% equity position in your house. But as a tell most people, nobody has a loan for 30 years, and the average mortgage is either refinanced or home sold within the first 5-7 years. VA Loans-

VA loans offer eligible Veterans and Active Duty Personnel to buy a home going no money down with no monthly mortgage insurance. This is probably the best no money down loan out there since the rates are traditionally very low on comparison to other government insured mortgages and no monthly mortgage insurance. The VA loan can be used anywhere in the state of Kentucky with the maximum VA loan limit being removed for 2021 USDA Loans-

USDA loans offer people buying a home in rural areas (typically towns of $20k or less) to buy a home going zero down. You cannot currently own another home and there is household income limits of $90,200 for a household family of four, and up to $119,300 for a household of five or more. You search USDA website for eligible areas and household income limits below at the yellow highlighted link :

KHC or Kentucky Housing- Kentucky First Time Home Buyers typically use KHC for their down payment assistance. KHC currently offers $10,000 for down payment assistance and sometimes throughout the year they will offer low mortgage rates on their mortgage revenue bond program.

The down payment assistance usually never runs out because you have to pay it back in the form of a second mortgage. It helps a lot of home buyers that want to buy in urban areas that cannot utilizer the USDA program in rural areas. Most of the time the first mortgage is a FHA loan tied with the 2nd mortgage fore down payment assistance. All KHC programs require a 620 score and rates are locked for 45 days.

5. What if I have had a bankruptcy or foreclosure in the past?

FHA and VA are the easiest on previous bankruptcies. FHA and VA both require 2 years removed from the discharge date on a Chapter 7. If you are in the middle of a Chapter 13, FHA will allow for financing with a 12 month clean history payment to the Chapter 13 courts, and with trustee permission.

VA requires 2 years removed from a foreclosure (sheriff sale date of home) and FHA requires 3 years.

USDA requires 3 years removed from both a foreclosure and bankruptcy, but on the foreclosure they do not go off the sale date. This may save you a little time if you had a previous foreclosure.

Fannie Mae (Conventional Loan)

Fannie Mae is by far the strictest. They require 4-7 years out of a foreclosure or bankruptcy

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people

CONFIDENTIALITY NOTICE: This message is covered by the Electronic Communications Privacy Act, Title 18, United States Code, §§ 2510-2521. This e-mail and any attached files are deemed privileged and confidential, and are intended solely for the use of the individual(s) or entity to whom this e-mail is addressed. If you are not one of the named recipient(s) or believe that you have received this message in error, please delete this e-mail and any attached files from all locations in your computer, server, network, etc., and notify the sender IMMEDIATELY at 502-327-9770. Any other use, re-creation, dissemination, forwarding, or copying of this e-mail and any attached files is strictly prohibited and may be unlawful. Receipt by anyone other than the named recipient(s) is not a waiver of any attorney-client, work product, or other applicable privilege. E-mail is an informal method of communication and is subject to possible data corruption, either accidentally or intentionally. Therefore, it is normally inappropriate to rely on legal advice contained in an e-mail without obtaining further confirmation of said advice.

The type of mortgage you’re applying for determines the minimum requirements you’ll have to meet for your down payment, credit score, and debt-to-income ratio.

Find out what type of loan you might qualify for or what aspects of your finances you’ll need to improve to get a better shot at qualifying for a mortgage.

Loan Type

Min. Down Payment

Min. Credit Score

Max DTI

Property Type

Conventional

3%

620

45%

Primary, secondary, investment

VA

0%

none

none

Primary

FHA

3.5%

500

50%

Primary

USDA

0%

none

41%

Primary

Keep in mind: The minimum down payment, minimum credit score, and maximum DTI shown in the table apply to mortgages used to purchase a primary residence. While you can use a conventional loan or a jumbo loan to purchase a home for another purpose, you might need a larger down payment, a higher credit score, more cash reserves, or all three.

Credit score needed to buy a house

Mortgage lending is risky, and lenders want a way to quantify that risk. They use your three-digit credit score to gauge the risk of loaning you money since your credit score helps predict your likelihood of paying back a loan on time. Lenders also consider other data, such as your income, employment, debts and assets to decide whether to offer you a loan.

Different lenders and loan types have different borrower requirements, loan terms and minimum credit scores. Here are the requirements for some of the most common types of mortgages.

Conventional loan

Minimum credit score: 620

A conventional loan is a mortgage that isn’t backed by a federal agency. Most mortgage lenders offer conventional loans, and many lenders sell these loans to Fannie Mae or Freddie Mac — two government-sponsored enterprises. Conventional loans can have either fixed or adjustable rates, and terms ranging from 10 to 30 years.

You can get a conventional loan with a down payment as low as 3% of the home’s purchase price, so this type of loan makes sense if you don’t have enough for a traditional down payment. However, if your down payment is less than 20%, you’re required to pay for private mortgage insurance (PMI), which is an insurance policy designed to protect the lender if you stop making payments. You can ask your servicer to cancel PMI once the principal balance of your mortgage falls below 80% of the original value of your home.

FHA loan

Minimum credit score (10% down): 500

Minimum credit score (3.5% down): 580

FHA loans are backed by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). The FHA incentivizes lenders to make mortgage loans available to borrowers who might not otherwise qualify by guaranteeing the federal government will repay the mortgage if the borrower stops making payments. This makes an FHA loan a good option if you have a lower credit score.

FHA loans come in 15- or 30-year terms with fixed interest rates. Unlike conventional mortgages, which only require PMI for borrowers with less than 20% down, all FHA borrowers must pay an up-front mortgage insurance premium (MIP) and an annual MIP, as long as the loan is outstanding.

VA loan

Minimum credit score: N/A

VA loans are mortgages backed by the U.S. Department of Veterans Affairs (VA). The VA guarantees loans made by VA-approved lenders to qualifying veterans or service members of the U.S. armed forces, or their spouses. This type of loan is a great option for veterans and their spouses, especially if they don’t have the best credit and don’t have enough for a down payment.

VA loans are fixed-rate mortgages with 10-, 15-, 20- or 30-year terms.

Most VA loans don’t require a down payment or monthly mortgage insurance premiums. However, they do require a one-time VA funding fee, that ranges from 1.4% to 3.6% of the loan amount.

USDA loan

Minimum credit score: N/A

The U.S. Department of Agriculture guarantees loans for borrowers interested in buying homes in certain rural areas. USDA loans don’t require a minimum down payment, but you have to meet the USDA’s income eligibility limits, which vary by location.

All USDA mortgages have fixed interest rates and 30-year repayment terms.

USDA-approved lenders must pay an up-front guarantee fee of up to 3.5% of the purchase price to the USDA. That fee can be passed on to borrowers and financed into the home loan. If the home you want to buy is within an eligible rural area (defined by the USDA) and you meet the other requirements, this could be a great loan option for you.

What else do mortgage lenders consider?

Your credit score isn’t the only factor lenders consider when reviewing your loan application. Here are some of the other factors lenders use when deciding whether to give you a mortgage.

Debt-to-income ratio — Your debt-to-income (DTI) ratio is the amount of debt payments you make each month (including your mortgage payments) relative to your gross monthly income. For example, if your mortgage payments, car loan and credit card payments add up to $1,800 per month and you have a $6,000 monthly income, your debt-to-income ratio would be $1,800/$6,000, or 30%. Most conventional mortgages require a DTI ratio no greater than 36%. However, you may be approved with a DTI up to 45% if you meet other requirements.

Employment history — When you apply for a mortgage, lenders will ask for proof of employment — typically two years’ worth of W-2s and tax returns, as well as your two most recent pay stubs. Lenders prefer to work with people who have stable employment and consistent income.

Down payment — Putting money down to buy a home gives you immediate equity in the home and helps to ensure the lender recoups their loss if you stop making payments and they need to foreclose on the home. Most loans — other than VA and USDA loans — require a down payment of at least 3%, although a higher down payment could help you qualify for a lower interest rate or make up for other less-than-ideal aspects of your mortgage application.

The home’s value and condition — Lenders want to ensure the home collateralizing the loan is in good condition and worth what you’re paying for it. Typically, they’ll require an appraisal to determine the home’s value and may also require a home inspection to ensure there aren’t any unknown issues with the property.

The Federal Housing Administration (FHA) has announced, effective for case numbers endorsed on and after 03/20/2023, a 30 basis point reduction in the annual premium charged to mortgage borrowers.

The cut, widely anticipated by the industry, will result in mortgage insurance premiums (MIP) of 55 bps for most borrowers, down from 85. The reduction also amends the Base Loan amount threshold used to establish MIP rates to the national conforming loan limit of $726,200, which increased from $625,500. Please refer to the following for the 03/20/2023 Annual Mortgage Insurance Premium MIP reduction:

FHA Loans with Terms > 15 Years

Base loan Amount and LTV:

Less than or equal to $726,200

≤ 90.00% (50 bps) 11 years

> 90.00% but ≤ 95.00% (50 bps) Mortgage term

> 95.00% (55 bps) Mortgage term

Greater than $726,200

≤ 90.00% (70 bps) 11 years

> 90.00% but ≤ 95.00% (70 bps) Mortgage term

> 95.00% (75 bps) Mortgage term

FHA Loans with Terms < 15 Years

Base loan Amount and LTV:

Less than or equal to $726,200

≤ 90.00% (15 bps) 11 years

> 90.00% (40 bps) Mortgage term

Greater than $726,200

≤ 78.00% (15 bps) 11 years

> 78.00% but ≤ 90.00% (40 bps) 11 years

> 90.00% (65 bps) Mortgage term

Please Note:

There is no change to the Upfront Mortgage Insurance Premium (UFMIP). This remains at 175 Basis Points (bps) (1.75%) of the Base Loan Amount

The MIP reduction applies to all Title II mortgages except Streamline Refinance and Simple Refinance Mortgages used to refinance a previously FHA endorsed Mortgage on or before May 31, 2009.

On February 22, 2023, HUD announced a 30 basis point MIP reduction on certain Kentucky FHA loans. According to the government agency, an estimated 850,000 borrowers could benefit this coming year, and the average Kentucky FHA homeowner will save $800 annually.

What you need to know:

The new rate is effective on loans endorsed for insurance by FHA on or after March 20, 2023.

Current clients could refinance to lower their monthly payments or shorten their term.

A lower MIP could open the door for more homebuyers who previously could not qualify.

FHA loans have many benefits, including flexible qualifications and low down payment requirements, and they allow for down payment assistance. Plus, there are no appraisal fees on a streamline refinance.

Contact your borrowers and prospects who are currently in an Kentucky FHA loan or could benefit from one to discuss how this change can work to their advantage.

FHA Reduces Annual Mortgage Insurance Premiums by 30 Basis Points to Support Affordable Homeownership

The Federal Housing Administration (FHA) announced today through Mortgagee Letter 2023-05 a 30 basis point reduction to the Annual Mortgage Insurance Premiums (annual MIP) it charges borrowers for FHA-insured Single Family Title II forward mortgages. This reduction supports the Biden-Harris Administration’s goals of making homeownership more accessible and affordable for the nation’s homebuyers. FHA mortgage insurance facilitates broader availability of mortgage financing to those not adequately served by the conventional mortgage market, particularly households of color for whom FHA-insured mortgages have been a cornerstone of access to affordable homeownership.

Today’s Mortgagee Letter provides additional information for mortgagees to implement the annual MIP reductions effective for mortgages endorsed for FHA insurance on or after March 20, 2023.

FHA estimates this reduction will benefit approximately 850,000 borrowers over the coming year, saving them $678 million in aggregate in the first year of their FHA-insured mortgage. For the average borrower purchasing a one-unit single family home with a down payment of 3.5 percent and a mortgage amount of $467,700 the national median home price as of December 2022 – FHA’s annual MIP reduction will save them more than $1,400 in the first year of their mortgage.

Wednesday, the Biden-Harris Administration announced reduced costs for FHA-backed mortgages.

In lowering annual mortgage insurance premiums 0.30 percentage points, the government makes homeownership more affordable and attainable for first-time buyers.

Here’s what you need to know about Kentucky FHA Loans and the changes that have been made for 2022.

What is a Kentucky FHA loan?

It stands for a Federal Housing Administration loan, meaning it is backed by the U.S. government. It is not made by a government agency. You deal directly with a mortgage lender or broker to get the loan, but the FHA will typically buy the loan from the lender after it is made or guarantee the lender against loss. FHA loans typically require lower down payments and credit scores than most conventional loans, making them a clear favorite among first-time buyers.

What Are the Terms?

These loans can have terms of either 30 years or 15 years. The interest rate is fixed for the entire loan length.

FHA borrowers are required to pay mortgage insurance premiums, but after a borrower’s equity in their home increases they may be able to refinance into a conventional loan and eliminate the monthly mortgage insurance premiums.

What Are the Qualifications?

To qualify for an FHA mortgage, home buyers need a FICO credit score of 580 or higher and a down payment of 3.5% (or a minimum down payment of 10% with a 500 FICO score).

These loans also require a two-year employment and income verification and the property as must be used as a primary residence.

If a borrower has had a bankruptcy, they must wait one to two years depending on if Chapter 13 or Chapter 7 before applying and three years after a foreclosure.

Increased Loan Limits for 2022

In 2022, for most parts of the U.S., Kentucky FHA borrowers can take out a loan for up to $420,680, an increase from 2021’s limit of $356,362.

Check your debt-to-income ratio (DTI). Mortgage lenders want to know how much debt you have compared to your income. It’s called your debt-to-income (DTI) ratio, and the better it is, the better mortgage terms you’ll get.

Find your DTI by plugging your financial numbers into Trulia’s affordability calculator. The percentage is found by dividing your debt by your income. For example, if your total debt is $3,000 a month (including your new mortgage payment), and your gross income is $6,000 a month, your DTI would be 50%.

Lenders typically prefer DTI to be no more than 36%—although some types of mortgages allow for a DTI of 50%. To lower yours, you can pay down debt or bring in more income.

One of the main pieces of an FHA loan approval is the borrower’s debt to income calculation. It is important that home buyers understand how this number is calculated and what they can do to improve their chances of getting approved.

Payments Included in Debt Ratios

Certain payments must be considered as part of a person’s overall debt when calculating the ratios. Items such as:

Payments for car loans

Payments on credit cards

Payments on unsecured loans

Child support payments

Alimony

Items Excluded from Debt Ratios

There are also some items not included in the debt to income ratio for FHA loans. Common examples would be:

Current rent payment

Money spent on entertainment

Expenses paid for child care

How to Overcome High Debt to Income Ratios

If a borrower has a compensating factor, it is possible for people with ratios higher than the proposed guidelines to get an approval for an FHA loan. Here are some examples of compensating factors:

Paying more than 10% of the purchase price as a down payment

Using income and expense records from the past two years to demonstrate that you have the ability and discipline to pay the housing expense

Having a large balance in a savings, investment or retirement account

For people that have a high debt to income ratio, it is possible to reduce the numbers. Paying off debt, such as credit cards or car loans can help. Sometimes it may be necessary to sell an expensive vehicle and get a cheaper payment in order to qualify for a loan.

$6000 Down for Your Dream Home with Down Payment Assistance

An exciting new program is making it easier for you to get your dream home faster and with more money in your pocket. Geared toward homebuyers who may need help coming up with down payment or closing costs, the Mortgage Down Payment Assistance Program (DPA) can turn you into a homebuyer today!

You do not need to be a first time homebuyer

Down payment assistance programs normally require you to be a first time homebuyer; however, this new program does not have this requirement. There are also various first mortgage options this program can be tied to, including FHA and USDA loans.

KHC recognizes that down payments, closing costs, and prepaids are stumbling blocks for many potential home buyers. Here are several loan programs to help. Your KHC-approved lender can help you apply for the program that meets your need.

Regular DAP

Purchase price up to $346,644 with Secondary Market.

Assistance in the form of a loan up to $6,000 in $100 increments.

Repayable over a ten-year term at 5.50 percent.

Available to all KHC first-mortgage loan recipients.

Affordable DAP

Purchase price up to $346,644 with Secondary Market.

FICO is used by 90% of lenders, according to myFICO, and has been around

since 1989. (VantageScore only hit the scene in 2006.)

If you’re not sure which scoring model a lender will use, just ask!

FICO Scores used for mortgages

USDA loan:

Most lenders prefer at least a 620

The U.S. Department of Agriculture insures for low- to moderate-income homebuyers. The USDA does not set a minimum credit score requirement and does not require a down payment.

Conventional loan:

620 is the minimum but in reality most will need a 720 or higher for a pre-approval if you are putting down less than 20%

Conventional loans aren’t insured by a government agency either, but they are covered by mortgage loan companies Fannie Mae and Freddie Mac. The down payment amount varies.

VA loan:

Most lenders prefer at least a 580

A Veterans Affairs loan is backed by the U.S. Department of Veterans Affairs and meant for military members and their spouses. These loans don’t require a minimum score or money down.

FHA loan:

500 (with 10% down payment) or 580 (with 3.5% down payment)

FHA loans, those guaranteed by the Federal Housing Administration, are for higher-risk borrowers who have poor credit and little money saved for a down payment. The credit requirements can fluctuate based on how much of a down payment you can afford.Most lenders have overlays now wanting a minimum 620 credit score even for FHA loans.

Are you interested in seeing how your current credit score might affect a new mortgage?

Let’s take a look together.

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

What Will My Lender Use? FICO is used by 90% of lenders, according to myFICO, and has been around since 1989. (VantageScore only hit the scene in 2006.) If you’re not sure which scoring model a lender will use, just ask! USDA loan: Most lenders prefer at least a 620 The U.S. Department of Agriculture … Continue reading Credit Score Information For Kentucky Home buyers

What credit score is needed to buy a house in Kentucky?

Ultimately, there is no singular credit score that can guarantee you a mortgage approval. Each lender is free to set their own credit score requirements.

But many loan types are insured by government organizations. And lenders cannot accept borrowers with credit scores below the minimum these organizations set. The four most popular home loan types are:

Conventional: Not backed by any government agency, but must meet the Fannie Mae and Freddie Mac underwriting guidelines

FHA: Loans backed by the Federal Housing Administration

VA: Loans backed by the US Department of Veterans Affairs (for military members)

USDA: Loans backed by the US Department of Agriculture (for low- to moderate-income families who buy homes in rural areas)

And here are the minimum credit score requirements for each of these loan types:

Conventional:

620 SCORE NEEDED. BUT TO GET APPROVED FOR A FANNIE MAE LOAN MOSTLY LIKE YOU WILL NEED A 720 SCORE OR HIGHER IF YOU HAVE LESS THAN 20% EQUITY POSITION OR LESS THAN 20% DOWN PAYMENT DUE TO PRIVATE MORTGAGE INSURANCE

FHA:

580 for a 3.5% down payment

500 for down payments of at least 10%

**MOST FHA LENDERS WILL WANT A 580 to 620 CREDIT SCORE NOWADAYS

VA:

No minimum BUT MOST VA LENDERS WILL WANT A 580 to 620 CREDIT SCORE

USDA:

No minimum, but with a credit score of at least 620 to 640 you could qualify for streamlined credit analysis and chances of approval goes way down if score is below 640…

You can often make a down payment as low as 3.5 percent down to a 580 credit score

You can finance a home with a 500 credit score with 10% down payment.

Kentucky FHA loans are assumable meaning that if you have a good rate on your current mortgage and the potential buyer of your home meets FHA guidelines, then he can assume your low rate mortgage

Kentucky FHA loans offer streamline refinancing without credit score minimums, verification of income, and no appraisals to refinance to a lower rate making it easier to qualify.

Kentucky FHA loans offer flexible terms when it comes to previous bankruptcy or foreclosures. 2 years removed from Chapter 7 with reestablished

credit, or if a Chapter 13, one year in the payment plan is eligible for FHA financing.

Foreclosures on a past home. FHA will finance a home 3 years removed from the sale date of your foreclosure property

30 year fixed rate mortgage with usually the best going rates on government insured loans like FHA, VA, USDA etc.

No prepayment penalty on Kentucky FHA loans.

Higher debt to income ratio requirements when compared to Conventional loans because most Fannie Mae Conventional loans cannot have a higher debt to income ratio than 45% on the back-end

You can make an FHA loan anywhere in the state of Kentucky with no geographical restrictions.

Will allow for down payment assistance and grants for borrowers minimum down payments in the State of Kentucky through the likes of KHC, Welcome Home Grant, and Kentucky Housing Down Payment Second Mortgage loans.

Kentucky FHA loans allow for unoccupied cosigner. For example, lets say you have a daughter that is getting ready to graduate college and does not have the income or credit history established yet to buy a home. FHA allows a family-member to co-sign for them to buy a home and you don’t have to occupy as primary residence. Note, FHA co-singers are not allowed to makeup for some that has bad credit, because they will take the lowest credit scores of both applicants. FHA usually allows for co-singers lack of income purposes only.

Can usually close within 30 days just like a regular conventional mortgage. No extra time to close an FHA loan in Kentucky versus other secondary market loans like VA, USDA, Fannie Mae.

You can use the FHA loan over and over. You can actually have two FHA loans open at the same time, but it gets tricky on this. Call or text me with more info if you have an FHA loan currently and would like to use FHA Financing again.

FHA loans aren’t just for first time home buyers in Kentucky.

Disadvantages of Kentucky FHA Mortgage Loans

There are loan limits in the State of Kentucky on FHA Mortgage loans. The maximum FHA loan in the state of Kentucky is $$420,680 for 2022. So if you were needing to finance a loan over this amount, you would need to look at doing a Conventional loan with the updated 2021 Kentucky State Loan Limits for a Fannie Mae loan being $647,250

Seller must have own the home for 90 days before you can make an offer on the home. This comes into play where the seller bought the home as an investor and rehabbed the property and wants to sell for a quick profit. FHA mandates seller must maintain for 90 days before you can write up an offer on it. Also called FHA Flipping Policy. Read more here

There is mortgage insurance. This is one of the biggest disadvantages for FHA loans. But as I tell most people, nobody rarely has a loan for 30 years, so if it meets your payment and your cash to close requirement, I tell people to go with it because it can be refinanced down the road and you are getting one of the lowers 30 year fixed rates out there. Both upfront and monthly mortgage insurance premiums you have to pay HUD/FHA. These premiums change whenever FHA/HUD replenish their insurance pool to pay claims from defaults, but currently the FHA upfront mortgage insurance premium is 1.75% and monthly is .85% and .80% of the loan amount. If you happen do a 15 year term or shorter, the mortgage insurance is cheaper monthly with .45 and .70 respectively each month. The upfront mortgage insurance is the same for a 30 year and 15 year at 1.75%

FHA Mortgage insurance can be on the loan for life of loan. This is a recent change made in 2016 when FHA lowered there premiums for upfront and monthly mi premiums, but made the mortgage insurance for life of loan for some FHA loans.

If you put down more than 10% on the loan, or have at least 10% equity in the home for a refinance, you only have to pay mortgage insurance for 11 years before it automatically falls off.

Obviously you can refinance out of an FHA loan at anytime, since it does not a prepayment penalty, and you can potentially get a refund of your upfront mortgage insurance if paid off within 3 years on sliding scale.

I have incorporated some charts below to illustrate the different Kentucky FHA Mortgage Insurance premiums to explain it better.

The upfront mortgage insurance is usually financed into the loan, so it will look like you are borrowing more than the standard 3.5% down payment because this is financed into the loan. Some borrowers elect to pay it out of pocket upfront, but I have never seen this done in my 20 years of doing FHA loans in the State of Kentucky

Kentucky FHA Loans Greater Than 15 Years MIP Chart

👇

Base Loan Amt.

LTV

Annual MIP

≤$625,500

≤95.00%

80 bps (0.80%)

≤$625,500

>95.00%

85 bps (0.85%)

>$625,500

≤95.00%

100 bps (1.00%)

>$625,500

>95.00%

105 bps (1.05%)

Kentucky FHA Loans Less Than or Equal to 15 Years MIP Chart👇

Base Loan Amt.

LTV

Annual MIP

≤$625,500

≤90.00%

45 bps (0.45%)

≤$625,500

>90.00%

70 bps (0.70%)

>$625,500

≤78.00%

45 bps (0.45%)

>$625,500

78.01% – 90.00%

70 bps (0.70%)

>$625,500

>90.00%

95 bps (0.95%)

When can I get the FHA mortgage insurance off my Mortgage Loan? See chart below 👇👇

Appraisals. On an FHA appraisal, the FHA appraiser has to turn on the utilities to make sure they are in worked order when he gets there. This is different that Conventional loan appraisals. A lot of realtors or buyers think that FHA loans are harder due to appraisals, but honestly, they’re really not. FHA puts these minimum HUD standards in place to make sure the home is in good working order and SAFE to live in. I.e.is there any lead based paint or chipping paint that could lead to poisoning It is all about Safety with FHA and HUD on these appraisals. The value is determined just like a regular Conventional, USDA, VA appraisals whereas they compare the house to 3 recent homes sold in the area to get a value.

Some lenders don’t offer FHA loans due to their complexity and sale on the secondary market, so if you call a local lender in Kentucky and they don’t offer FHA loans, the reason is usually they don’t have the team in place to do them or don’t want to do them due to lack of experience on the secondary government market.

Government Liens. FHA will not be an option for you usually if you have unpaid federal tax liens, delinquency on federal backed-government loans, or a claim with social security etc. FHA loans are ran through aCAVIRS alert system to check to see if you are delinquent on any federal oblation. If so, this swill stop you until you can clear the CAVIRS alert system. For example, I did a loan for a buyer that had a delinquent federal debt with his student loan that happened over 14 years old. It was off the credit report and title search, so I had to switch to a conventional loan to make the home loan work.

FHA loans are not good for second homes or investment properties. FHA loans are mainly for single family residence 1-4 unit, that are going to occupied primarily as main home.

In summary, FHA loans have few drawbacks other than the mortgage insurance in my opinion. It is a great first time home buyer program or borrowers with past credit problems to get into a house of their own with very little out of pocket, at a low 30 year fixed rate, and no prepayment penalty

Questions about qualifying for a FHA loan in Kentucky . Give me text, call or email below. Love to help you out on your next home or refinance in Kentucky

Read more below about specific FHA Loans in Kentucky.👇👇👇

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.