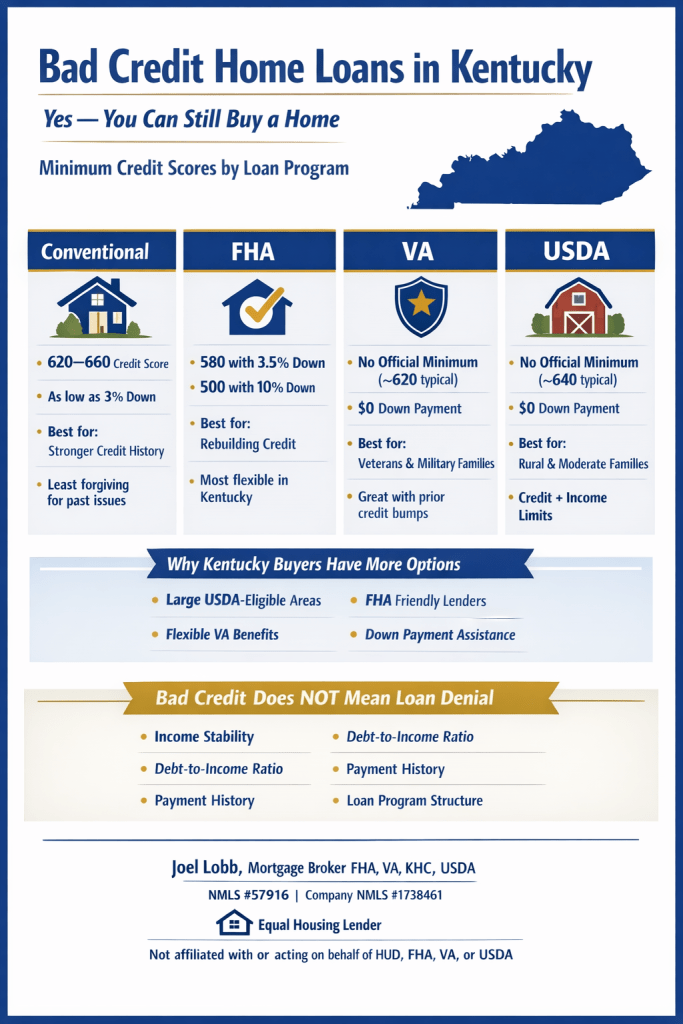

Many Kentucky homebuyers assume a low credit score automatically disqualifies them from buying a home.

That assumption is incorrect. Several mortgage programs are specifically designed to help buyers with past credit issues qualify for financing sooner than expected.

In Kentucky, the most common loan options for buyers with bad or fair credit include FHA, VA, USDA,

and select conventional loan programs. Each option has different credit score thresholds, down payment requirements,

and underwriting flexibility.

Minimum Credit Score Requirements by Loan Type

Conventional loans typically require a minimum credit score between 620 and 660, depending on the program and automated underwriting results.

While down payments can be as low as 3 percent, conventional loans are generally the least forgiving when it comes to recent late payments, collections, or limited credit history.

FHA loans in Kentucky are the most common solution for buyers rebuilding credit.

FHA financing allows approvals with credit scores as low as 580 with only 3.5 percent down.

In limited cases, buyers with scores down to 500 may qualify with a 10 percent down payment, provided the overall risk profile is strong.

Eligible service members and veterans may benefit from

VA loans in Kentucky, which do not have an official minimum credit score requirement set by the agency.

Most lenders look for scores around 620, but VA loans remain one of the most flexible options available, offering zero down payment and no monthly mortgage insurance.

For buyers purchasing outside major metro areas,

USDA loans in Kentucky can provide 100 percent financing with competitive interest rates.

While there is no official minimum credit score, most USDA lenders require a 640 score for automated approval, along with meeting income and household eligibility guidelines.

Why Kentucky Buyers Often Qualify With Lower Credit Scores

Large portions of Kentucky qualify for USDA rural housing loans

FHA loans are widely accepted by Kentucky lenders

VA loans provide exceptional flexibility for eligible veterans

Down payment assistance programs can be layered correctly with the right loan structure

What Mortgage Underwriters Actually Review

Mortgage approval is based on the full financial picture, not just the credit score. Underwriters evaluate income stability,

work history, debt-to-income ratio, recent payment behavior, available assets, and how the loan is structured.

In many cases, a borrower with a lower credit score but strong income stability and clean recent payment history

can be a stronger approval than someone with a higher score and excessive debt.

Bottom Line for Kentucky Homebuyers

Bad credit does not automatically mean loan denial. The right loan program, structured correctly from the start,

often matters more than the credit score alone. Many Kentucky buyers qualify months or even years sooner than they expect

once their options are reviewed properly.

NMLS #57916 | Company NMLS #1738461

Equal Housing Lender.

This is not a commitment to lend. All loans are subject to credit approval and program requirements.

Kentucky FHA Loans: New Guidelines for Collections & Disputes 2026

Kentucky FHA Loans: New 2026 Guidelines

Collections, Disputes & Judgements Explained

If you’re a Kentucky first-time homebuyer with collections, disputes, or judgements on your credit report, you’re not alone—and you’re not disqualified from homeownership. The Federal Housing Administration (FHA) recently updated its lending guidelines to provide more flexibility and clarity around credit challenges.

Whether you’ve faced financial hardship, billing disputes, or collection accounts, understanding these new FHA rules could be the key to securing your Kentucky mortgage.

📋 Effective Date: All loans with case numbers assigned on or after September 9th, 2026

Understanding FHA Loans with Bad Credit, Disputes & Collections

What Are Disputed Accounts on Your Credit Report?

A disputed account appears on your credit report when you’ve officially challenged information you believe is inaccurate or incorrect. Many Kentucky borrowers don’t realize that disputed accounts can affect their ability to qualify for an FHA loan. The good news? FHA has clarified how these accounts will be evaluated going forward.

Collection Accounts & FHA Loan Qualification

Collection accounts are one of the biggest obstacles for Kentucky first-time homebuyers trying to get approved. Under the new 2026 FHA guidelines, the agency has provided specific underwriting rules that actually offer more opportunity than you might think.

Judgements on Credit Reports

If you have judgements on your credit report, FHA underwriters will evaluate them carefully, but they don’t automatically disqualify you. The new guidelines provide specific direction on how these accounts are assessed during the mortgage approval process.

New FHA Guidelines for Collections, Judgements & Disputes

Collection Account Rules: The $2,000 Threshold

Here’s how FHA Fannie Mae’s DU (Desktop Underwriter) system now handles collection accounts:

If your collection accounts total $2,000 or more cumulatively:

Pay in Full — The collection debt(s) must be paid in full prior to or at closing, OR

Payment Plan — You can establish a payment arrangement with the creditor, and the monthly payment is included in your debt-to-income ratio, OR

5% Payment Calculation — Include a monthly payment of 5% of the outstanding balances of each collection account in your debt-to-income ratio

If your collection accounts total less than $2,000: These may be treated more favorably during underwriting, though FHA DU will still require verification.

💡 Important for Kentucky Borrowers: If you’re married and in a community property state, collection accounts from your spouse are also counted toward this threshold—even if they’re a non-borrowing spouse.

Manual Underwriting Triggers

Certain credit situations require manual underwriting instead of automated approval. Your Kentucky FHA application will likely be manually reviewed if:

$1,000 or more in disputed derogatory credit accounts appears on your credit report

20% or greater decline in self-employed income

Mortgage lates within the last 12 months

While manual underwriting takes longer, it doesn’t mean you’ll be denied. Many Kentucky borrowers with credit challenges are successfully approved through manual underwriting because a trained loan officer can explain your circumstances and compensating factors.

Payment History Requirements for FHA Approval

FHA has strict (but achievable) payment history standards:

All mortgage and installment loan payments must be on time within the last 12 months

No more than two 30-day late payments within the last 24 months

No derogatory credit on revolving accounts (credit cards, lines of credit) in the last 12 months

Collection accounts must be addressed per the guidelines above

Additional 2026 FHA Updates

New Well Water Testing Requirements

If you’re purchasing a Kentucky home with a private well, be aware of updated FHA requirements for well water testing:

Well water tests must now be:

Performed by a disinterested third party (not you, the seller, or anyone with a financial interest in the transaction)

Conducted using a method acceptable to your local health authority

Documented before approval

Well water testing is now required for:

Newly constructed properties and/or new wells

Properties with deficiencies in the well or water quality identified by an appraiser

Areas where water safety issues have been reported or are known

Properties near dumps, landfills, industrial sites, farms, or hazardous waste areas

Properties where the well and septic system are less than 100 feet apart

Overtime, Bonus & Tip Income: Simplified Calculations

Good news for Kentucky borrowers with variable income: FHA has clarified how overtime, bonuses, and tips are calculated for loan qualification.

Your overtime, bonus, or tip income will be calculated as the LESSER of:

Average income earned over the previous 2 years (or the total time if earned less than 2 years), OR

Average income earned over the previous year

Commission & Business Expense Requirements Removed

FHA has completely eliminated previous requirements regarding unreimbursed business expenses and commission income or automobile allowances. This aligns FHA guidelines with current IRS tax law, making it easier for self-employed borrowers and those with commission-based income to qualify.

Interested Party Contribution (IPC) Limits

Under the 2026 guidelines, mortgagees and third-party originators are now explicitly included in IPC limits. This means:

Lenders cannot contribute toward your down payment to artificially lower your upfront costs

Exception: Premium pricing credits don’t count against IPC limits—unless the lender is also acting as the seller, agent, builder, or developer

DTI Requirements & Qualification

31% Front-End / 43% Back-End FHA

31% of your gross monthly income can go toward housing costs. 43% of your gross monthly income can go toward all monthly debts.

No compensating factors required to meet these ratios, making FHA one of the most accessible loan programs for Kentucky borrowers.

Documentation You’ll Need for Underwriting

If your Kentucky FHA application requires manual underwriting due to credit challenges, be prepared to provide:

Employment & Income Documentation

Verbal Verification of Employment (VOE)

Paystubs covering the most recent 30-day period

W2s for the past 2 years

2-year employment history

Housing & Credit History

Verification of Rent (VOR) or 12 months of cancelled checks if credit report doesn’t show last 12 months of housing payment history

Letter of Explanation (LOX) for any derogatory credit or late payments within the last 24 months

Cash Reserves

At least 1 month in reserves from your own funds (cannot be a gift)

3 months required if purchasing a 3-4 unit property

Ready to Get Approved for a Kentucky FHA Loan?

With over 20 years of experience helping Kentucky families overcome credit challenges to achieve homeownership, I specialize in FHA loans for borrowers with collections, disputes, judgements, late payments, and more.

I offer free FHA mortgage applications with same-day approvals. Let’s discuss your options today.

About Joel Lobb – Kentucky Mortgage Loan Officer

With over 20 years of mortgage industry experience, I’ve helped more than 1,300 Kentucky families secure homeownership through FHA, VA, USDA, KHC, and Fannie Mae programs.

Your Guide to Disputed Accounts & Collections 2026

💰

Collection Accounts: The $2,000 Threshold

Step 1: Check Total

Add up all collection accounts on your credit report

Step 2: Compare

$2,000?

Is your total more or less?

Step 3: Choose Path

Select your payment strategy

1

Pay in Full

Pay before or at closing

2

Payment Plan

Monthly payment included in DTI

3

5% Calculation

5% of balance added to DTI

❓

Disputed Accounts

What Triggers Manual Underwriting?

If you have $1,000 or more in disputed derogatory accounts, your application will be reviewed by a human underwriter instead of automated approval. This isn’t bad news—it means your circumstances can be explained!

The Best Kentucky Mortgage Loan Options When Looking for your first house in Kentucky Kentucky First-time Home Buyer Programs👀💯👇‼

Kentucky Mortgage Requirements for FHA, VA, USDA and Fannie Mae

FHA loan in Kentucky you will be confronted with minimum credit score requirements set forth by FHA and the lender. Even though FHA will insure the mortgage loan at a certain credit score, you will see that lenders will create “credit-overlays” to protect their risk and ask for a higher credit score.

So keep in mind when you are getting an FHA lenders will have higher credit score minimums in addition to the FHA Mortgage Insurance program.

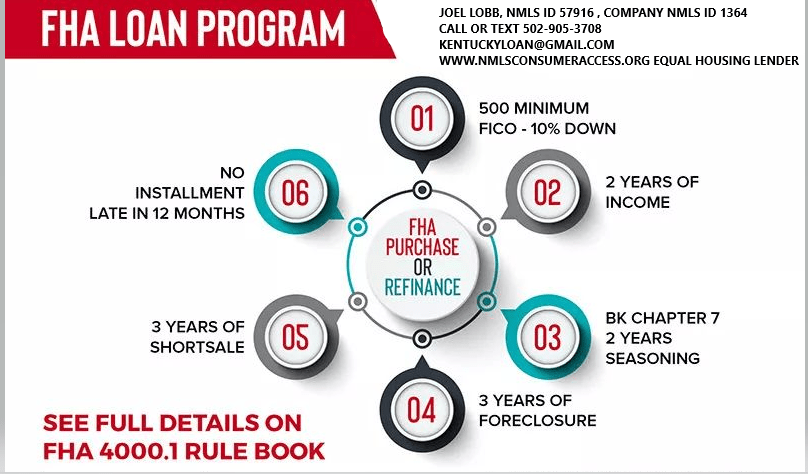

For a Kentucky Homebuyer wanting to purchase a home or refinance their existing FHA loan, FHA requires a 3.5% down payment and the borrower must have a 580 FICO Credit Score. If the score is below 580, then you would need 10% down and still qualify on a manual underwrite.

You must have a FICO score of at least 500 to be eligible for a Kentucky FHA loan. If your FICO score is from 500 to 579, your down payment on the loan is 10 percent of the loan.

If your FICO score is 580 or higher, your down payment is only 3.5 percent. If your credit score is less than 580, it may be more cost-effective to take the necessary steps to improve your score before taking out the loan, rather than putting the money into a larger down payment.

How do they get the credit score: There are three main credit bureaus in the US. Equifax, Experian, and Transunion. The three scores vary but should be relatively close as long as the same creditors are reporting to the same bureaus.

You will get a variation in the scores due to all creditors or collection companies don’t report to all three bureaus. This is why they take the mid score. So if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying credit score would be 620

Based on my experience with lenders that I deal with in Kentucky on FHA loans, most lenders require 620 middle credit score for consideration for loan approval.

How do they get the score: They take the mid score, so if you have a 590 Experian, 680 Equifax, and 620 TransUnion, your qualifying score would be 620.

If your score is below 620, a manual underwrite is where the AUS (Automated Underwriting System) refers your loan to a human being, and they look at the entire file to see if they can overturn and approve the mortgage loan because the Desktop Underwriting Automated Software could not approve you.

With scores below 620, they typically will want to verify your rent history, have no bankruptcies in the last two years, and no foreclosures in the last 3 years.

If you have had any lates since the bankruptcy this will probably result in a denial on a refer manual underwrite file.

Your max house payment will be set at 31% of your gross monthly income, and your new house payment plus the bills you are paying on the credit report cannot be more than 43%.

Typically, on scores below 620 for FHA loans, they will also look at reserves or money you have saved up after the loan is made to try and qualify you. For example, if you have a 401k or savings account that has at least 4 months reserves (take your mortgage payment x 4) and this would equal your reserves. They look at this as a rainy day fund and could help you keep up on your bills if you were unemployed or could not work.

The first thing to keep in mind is that qualifying for a mortgage involves a lot more than just a credit score. While your FICO score is a very important ingredient, it is just one factor. Lenders also look at your income and level of debt, among other things.

A FICO score between 600 and 640 is considered fair to good credit. But keep in mind, this range of credit scores does not guarantee you will qualify for a mortgage, and if you do qualify, it won’t get you the lowest interest rate possible. Still, to buy a home aim for a score of at least 620, recognizing that other factors weigh in the decision and that some banks may require a higher score.

What credit score do you need to get a low rate mortgage?

It uses to be that a score of about 720 would yield the lowest mortgage rates available. Today, the best rates kick in with a FICO score of 760. And interest rates go up significantly as your credit score drops. To give you an idea, the following table shows current rates by credit score and calculates a monthly principal and interest payment based on a $300,000 loan:

lenders will pull what they call a “tri-merge” credit report which will show three different fico scores from Transunion, Equifax, and Experian. The lenders will throw out the high and low scores and take the “middle score.” For example, if you had a 614, 610, and 629 score from the three main credit bureaus, your qualifying score would be 614.

So if you only have one score, you may not qualify. Lenders will have to pull their own credit report and scores so if you had it ran somewhere else or saw it on a website or credit card you may own, it will not matter to the lender, because they have to use their own credit report and scores.

Lastly, lenders will pull your credit report for free nowadays so this should not be a big deal as long as your scores are high enough.

offered by FHA, VA, USDA, Fannie Mae, and KHC all have their minimum fico score requirements and lenders will create overlays in addition to what the Government agencies will accept, so even if on paper FHA says they will go down to 580 or 500 in some cases on fico scores,

If you have low fico scores it may make sense to check around with different lenders to see what their minimum fico scores are for loans.

The lenders I currently deal with have the following fico cutoffs for credit scores:

As you can see, different government-backed loan programs have different minimum score requirements with most lenders for an FHA, VA, or Fannie Mae loan, and 620 is required for the no down payment programs offered by USDA and KHC in Kentucky for First Time Home Buyers wanting to go no money down.

By paying down your credit card balances (credit utilization) and having a good pay history (payment history) ,this is the best way to raise your score.

The credit bureaus don’t update immediately, so I would not add to the balance or open any new bills or have any other lender do an inquiry on your credit report while we wait for the scores to hopefully go up in the next 30 days. Try to keep everything status quo and make your payments on time and keep your balances low or lower than what is now reporting on the credit report.

How to improve your credit score!

Pay Every Single Bill on Time, or Early, Every Month

Please understand one thing; paying your bills on time each month is the single most important thing you can do to increase your credit scores.

Depending on the credit bureau, there are 4 or 5 main items that determine everyone’s credit score. Of those items, your history of paying bills makes up about 35% of the score. THIS IS HUGE!

Paying your bills on time shows lenders that you are responsible. It will also spare you from paying late fees whether it is a charge from a credit card or an added fee from your landlord.

Use a calendar, or a phone app, or some other organized system to make sure that you pay your bills on time every single month.

Another big factor in calculating a credit score is the amount of credit card debt. Credit bureaus look at two things when analyzing your credit cards.

First, they look at your available credit limit. Second, they look at the existing balance on each card. From these two figures an available ratio is developed. As the ratio goes higher, so too will your credit score increase.

Here is one simple example. Suppose a person has the following credit cards, corresponding balances, and credit limits

Credit Card

Current Balance

Credit Limit

Chase Visa

$105

$1,000

MarterCard from local bank

$236

$1,500

BP MasterCard

$87

$500

Totals

$428

$3,000

From these numbers, we get the following calculation

$428/$3,000 = 14%

In other words, the person is using 14% of their available credit and they have 86% available credit. The closer that ratio is to 100%, the better the credit score will be.

MAIN TIP: Keep all credit card balances as low as possible.In this particular example, if they had a problem with their car, or needed medical attention or some other emergency, the person would have the money necessary to handle the situation without incurring new debt. This is wise on the consumer’s part and lenders like to see this kind of money management.

Credit Cards Part 2: 1 or 2 is Better Than a Wallet Full

The previous example showed a person that utilized just three credit cards. This is much better than someone who has 5+ credit cards, all with available balances. Why? Lenders do not like to see someone that has the potential to get too far in debt in a short amount of time.

Some people have 5, 10 or more credit cards and they use many of them. This shows a lack of restraint and control. It is much better, and neater, to have only 2 or 3 cards with low rates that handle all of your transactions. A lower number of cards are easier to manage and it does not give a person the temptation to go on a huge shopping spree that could take years to payoff.

MAIN TIP: Try to limit yourself to no more than 2-3 credit cards.

Keep the Good Stuff Right Where it is

Too many people make the mistake of paying off old debts, such as old credit cards, and then closing the account. This is actually a bad idea.

A small part of the credit score is based on the length of time a person has had credit. If you have a couple of credit cards with a long track history of making payments on time and keeping the balance at a manageable level, it is a bad idea to close out the card.

Similarly, if you have been paying on a car or motorcycle for a long time, do not be in a hurry to pay off the balance. Continue to make the payments like clockwork each month.

An account that has a good record will help your scores. An account that has a good record and multiple years of use will have an even better impact on your score.

MAIN TIP: Keep old accounts open if you have a good payment history with them.

Stop Filling Out Credit Applications

Multiple credit inquiries in a short amount of time can really hurt your credit scores. Lenders view the various inquiries as someone that is desperate and possibly on the verge of making a bad financial choice.Too many people make the mistake of getting more credit after they are approved for a loan. For example, if someone is approved for a new credit card, they feel good about their finances and decide to apply for credit with a local furniture store. If they get approved for the new furniture, they may decide to upgrade their car. This requires yet another loan. They are surprised to learn that their credit score has dropped and the interest rate on the new car loan will be much higher. What happened?

If you currently have 2 or 3 credit cards along with either a car loan or a student loan, don’t apply for any more debt. Make sure the payments on your current debt are all up to date and focus on paying them all down.

In a few months of making timely payments your scores should noticeably go up.

MAIN TIP: Limit your new loans as much as possible

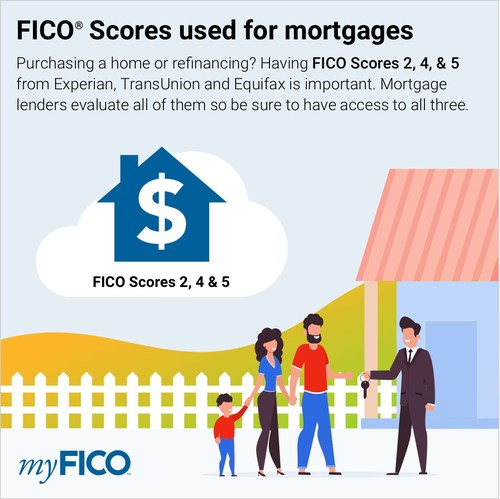

Which credit scores do mortgage lenders use to qualify people for a mortgage?

While it’s common knowledge that mortgage lenders use FICO scores, most people with a credit history have three FICO scores, one from each of the three national credit bureaus (Experian, Equifax, and TransUnion).

Which FICO Score is Used for Mortgages

Most lenders determine a borrower’s creditworthiness based on FICO® scores, a Credit Score developed by Fair Isaac Corporation (FICO™). This score tells the lender what type of credit risk you are and what your interest rate should be to reflect that risk. FICO scores have different names at each of the three major United States credit reporting companies. And there are different versions of the FICO formula. Here are the specific versions of the FICO formula used by mortgage lenders:

Equifax Beacon 5.0

Experian/Fair Isaac Risk Model v2

TransUnion FICO Risk Score 04

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

Which Score Gets Used?

Since most people have three FICO scores, one from each credit bureau, how do lenders choose which one to use?

For a FICO score to be considered “usable”, it must be based on adequate, concrete information. If there is too little information, or if the information is inaccurate, the FICO score may be deemed unusable for the mortgage underwriting process. Once the underwriter has determined if a score is usable or not, here’s how they decide which score(s) to use for an individual borrower:

If all three scores are different, they use the middle score

If two of the scores are the same, they use that score, regardless of whether the two repeated scores are higher or lower than the third score

Lenders have identified a strong correlation between Mortgage performance and FICO Bureau scores (FICO score). FICO scores range from 300 to 850. The lower the FICO score, the greater the risk of default.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation

FHA loans are a popular choice for many first-time homebuyers in Kentucky. This is due to their flexible qualifying criteria. If you’re considering an FHA loan in the Bluegrass State, understanding the key qualifying factors is crucial. Here’s a comprehensive guide to the criteria you need to know:

Credit Score Requirements:

FHA loans are known for accommodating borrowers with lower credit scores. The minimum required credit score can vary. Typically, a credit score of 580 or higher is needed to qualify for the minimum down payment of 3.5%. Borrowers with credit scores between 500 and 579 might still qualify. They will need a higher down payment, usually around 10%.

Down Payment:

The minimum down payment for an FHA loan in Kentucky is 3.5% of the home’s purchase price. This is advantageous for buyers who may not have substantial savings for a larger down payment, making homeownership more accessible.

Work History:

Lenders typically look for a steady 2 year employment history when considering FHA loan applications. A consistent work history is beneficial. It is preferable to have worked with the same employer or within the same field. This helps demonstrate financial stability and the ability to repay the loan.

Debt-to-Income Ratio (DTI):

The debt-to-income ratio is a crucial factor in mortgage approval. For FHA loans, the maximum allowable DTI ratio is typically around 40% to 45% of your gross monthly income. It can go higher up to 56% with good credit scores, a large down payment, or a shorter-term loan. Lenders may also consider higher ratios in certain cases if compensating factors are present.

Bankruptcy and Foreclosure:

FHA loans have lenient guidelines regarding bankruptcy and foreclosure. Generally, borrowers with a past bankruptcy may qualify for an FHA loan after two years. This is possible if they have re-established good credit and demonstrated responsible financial behavior. For foreclosures, the waiting period is usually three years.

Mortgage Term:

FHA loans offer various mortgage term options, including 15-year, 20 year, 25 year and 30-year fixed-rate loans. The choice of term depends on your financial goals and ability to manage monthly payments.

Occupancy: Primary residences with 1-4 units. Not for investment properties or second homes.

Mortgage Insurance on the loan for life of loan. Larger down payments and shorter terms will reduce the upfront mi and monthly mi premiums

can be used for refinances, not only for purchases.

No income limits nor property restrictions on where home is located

Can close within 30 days typically with good appraisal and title work

FHA Loan Requirements in Kentucky for Credit scores, Down payment, Debt Ratio and work history below

Requirement

Details

Credit Score

– 580+: Eligible for a 3.5% down payment. – 500-579: Requires a 10% down payment.

Down Payment

Minimum of 3.5% for qualified buyers; 10% for lower credit scores below 580 to 500 score range

Debt-to-Income Ratio (DTI)

– Ideal: 45% or lower on front end ratio or housing ratio. – Acceptable: Up to 57% with compensating factors. There are two ratios. Front end and back end with front end being maxed at 45% and the backed end ratio being 56.99% with an AUS approval. If manually underwritten, see guidelines here

Employment History

Must provide at least **2 years of consistent employment—College transcripts can supplement with a less than 2 year work history

Key Benefits of FHA Loans in Kentucky

Low Credit Score Requirements

FHA loans accept borrowers with credit scores as low as 500. However, a score of 580+ qualifies you for the lowest down payment option.

Low Down Payment Options

You can purchase a home with as little as 3.5% down if you meet credit requirements, making FHA loans more accessible than conventional loans.

Competitive Interest Rates

FHA loans typically offer rates comparable to conventional mortgages. They may even offer lower rates. This could save you money over the life of the loan.

Flexible Loan Uses

With an FHA 203(k) loan, you can bundle home purchase and renovation costs into a single mortgage.

Assumable Loans

FHA loans can be transferred to a new buyer. This feature is especially valuable if you sell your home when interest rates are higher.

Understanding these qualifying criteria can help you navigate the FHA loan application process in Kentucky more effectively. Working with an experienced mortgage professional can provide valuable guidance. They offer assistance tailored to your specific financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

Any questions, please don’t hesitate to reach out via, text, email, or call. Advice is always free.

One of Kentucky’s highest rated mortgage loan officers for FHA, VA, USDA, Kentucky Housing KHC and conventional mortgage loans.

Evo Mortgage Company NMLS# 1738461 Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

NMLS 57916 | Company NMLS #173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. (www.nmlsconsumeraccess.org).

Kentucky First Time Homebuyers FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans

Kentucky FHA Loans: Kentucky FHA loans are known for their lenient credit score requirements, making them accessible to borrowers with lower credit scores. However, a minimum score of 500 to 580 is typically required, depending on the down payment.

Kentucky VA Loans: VA loans offer flexible credit score requirements, while on paper VA states they don’t require a minimum score to insure the mortgage loan, most lenders preferring a FICO score of 620 or higher. Veterans, active-duty service members, and eligible spouses can benefit from VA loan options.

Kentucky USDA Loans: USDA loans are designed for rural homebuyers and require no minimum FICO score , but most lenders will want a credit score of 640 or higher. These loans offer zero down payment options for eligible properties.

KHC Mortgage Loans: Kentucky Housing Corporation (KHC) mortgage loans may vary in credit score requirements depending on the lender. It’s essential to work with a knowledgeable mortgage broker like Joel Lobb to understand specific lender guidelines. KHC requires a minimum 620 credit score for FHA, VA, USDA and 660 for Conventional loan programs

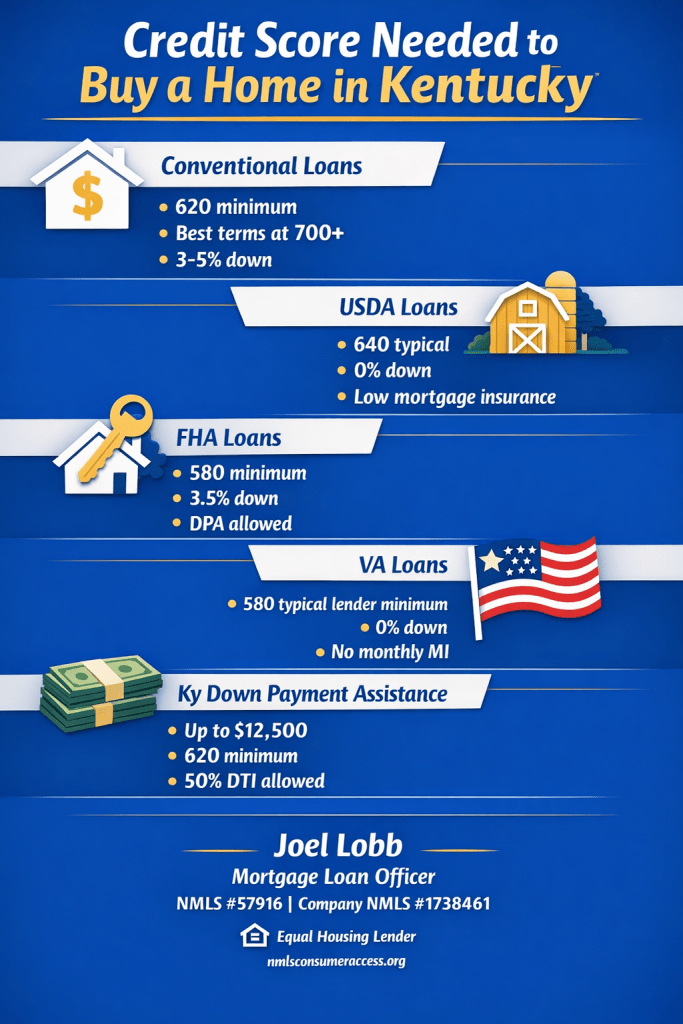

What Credit Score Do You Need to Buy a House in Kentucky?

There is no single “magic number.” The credit score needed depends on the loan program (Conventional, USDA, FHA, VA, or Kentucky Housing Corporation down payment assistance). Here’s how it works in the real world for Kentucky buyers.

Quick guide: typical credit score ranges and key highlights by Kentucky mortgage program.

Conventional Loans in Kentucky

Minimum credit score generally starts at 620.

Most lenders prefer higher scores for 3%–5% down options.

Best pricing and easier approvals are typically with strong credit (often 700+).

Mortgage insurance (PMI) usually improves as scores increase.

USDA Rural Housing Loans in Kentucky

Many lenders target around 640 for automated approval through GUS (Guaranteed Underwriting System).

Manual underwriting may be possible when automated approval is not available.

0% down payment required (eligible rural/suburban areas).

Typical fees include a 1% upfront guarantee fee and 0.35% annual fee (paid monthly).

USDA can be one of the best value options for Kentucky buyers with limited cash, provided the property is in an eligible area and the file meets income and underwriting requirements.

Kentucky FHA Loans

As low as 580 credit score with 3.5% down (typical baseline).

Gift funds, grants, and down payment assistance may be allowed.

Mortgage insurance is generally higher than USDA or VA, but rates can still be competitive.

Common waiting periods: 2 years after bankruptcy and 3 years after foreclosure (standard guideline).

Kentucky VA Loans

VA does not set a minimum credit score in its guidelines, but most lenders do.

Many VA lenders target around 580+ (lender overlay varies).

0% down and no monthly mortgage insurance.

Clear CAIVRS is required (for federal delinquency screening).

Kentucky Down Payment Assistance (KHC)

Kentucky Housing Corporation (KHC) often offers up to $12,500 down payment assistance (program terms and funding can change).

Typically structured as a second mortgage paid back over 15 years.

Minimum credit score is commonly 620 across many KHC options; KHC conventional often requires 660.

Maximum debt-to-income ratios are commonly around 50/50 (program and investor rules apply).

Next step: get a clear pre-approval target

If you share your approximate credit score range, income type, and whether you’re looking in Louisville, Lexington, or rural Kentucky, I can point you to the most realistic program and the exact score threshold that will matter for approval.

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “What credit score do I need to buy a house in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “It depends on the loan program. Conventional financing often starts around 620, USDA lenders commonly target about 640 for automated approval, FHA can allow down to 580 with 3.5% down, and many VA lenders look for around 580 even though VA does not publish a minimum score. Kentucky Housing Corporation down payment assistance commonly requires around 620 (and KHC conventional often around 660). Final approval also depends on income, debt-to-income ratio, and underwriting findings.”

}

},

{

“@type”: “Question”,

“name”: “Can I buy a home in Kentucky with a 580 credit score?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Often yes, depending on the full file. FHA commonly allows 580 with 3.5% down and can work well when you have limited savings or are using gift funds or down payment assistance. Lender overlays and underwriting results still apply.”

}

},

{

“@type”: “Question”,

“name”: “Is 640 a good credit score for a Kentucky mortgage?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “A 640 score can be workable for several programs. USDA lenders often target around 640 for automated approvals, and conventional approvals may be possible starting at 620, though terms improve as scores rise. Your debt-to-income ratio, income stability, and cash to close will strongly influence results.”

}

},

{

“@type”: “Question”,

“name”: “What credit score do I need for a USDA loan in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Many lenders prefer around 640 to obtain an automated approval through the USDA Guaranteed Underwriting System (GUS). Manual underwriting may be possible in some cases, but it is typically more restrictive on ratios and documentation.”

}

},

{

“@type”: “Question”,

“name”: “Does the VA require a minimum credit score in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “VA guidelines do not publish a minimum credit score, but lenders usually do. Many VA lenders commonly target around 580 or higher, depending on the overall file and lender overlays.”

}

},

{

“@type”: “Question”,

“name”: “What credit score is needed for Kentucky Housing Corporation (KHC) down payment assistance?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “KHC program requirements vary, but a common minimum is around 620 for many options. KHC conventional commonly requires around 660. Eligibility also depends on income limits, purchase price limits, and underwriting findings.”

}

}

]

}

What Credit Score Do You Need to Buy a House in Kentucky?

Are you considering buying a home in the beautiful state of Kentucky? Securing a mortgage loan is a crucial step in the homebuying process, and one of the key factors lenders evaluate is your credit score. Understanding the credit score requirements for mortgage loan approval in Kentucky can help you prepare and improve your chances of securing financing for your dream home.

Importance of Credit Scores

Your credit score is a numerical representation of your creditworthiness based on your credit history. Lenders use this score to assess the risk of lending to you. A higher credit score typically indicates lower risk to lenders, making you more likely to qualify for a mortgage loan and secure better terms and interest rates.

Credit Score Requirements in Kentucky

While specific credit score requirements can vary among lenders and mortgage programs, there are some general guidelines to consider when applying for a mortgage loan in Kentucky.

Conventional Loans: Conventional mortgage loans are not insured or guaranteed by the government. Many lenders prefer borrowers to have a credit score of at least 620 to qualify for a conventional loan. However, some lenders may require higher scores, especially for competitive interest rates.

FHA Loans: The Federal Housing Administration (FHA) offers loans with more lenient credit score requirements compared to conventional loans. In Kentucky, borrowers may be eligible for an FHA loan with a credit score as low as 500, provided they can make a 10% down payment. A credit score of 580 or higher may qualify for a lower down payment option of 3.5%.

VA Loans: If you’re a veteran, active-duty service member, or eligible spouse, you may qualify for a VA loan guaranteed by the Department of Veterans Affairs. VA loans typically have more flexible credit score requirements, and some lenders may consider borrowers with credit scores below 620.

USDA Loans: The U.S. Department of Agriculture (USDA) offers loans to eligible rural and suburban homebuyers with low to moderate incomes. Credit score requirements for USDA loans in Kentucky can vary, but many lenders prefer scores of 640 or higher.

Tips for Improving Your Credit Score

If your credit score is below the desired threshold for a mortgage loan, don’t despair. There are steps you can take to improve your creditworthiness over time:

Check Your Credit Report: Obtain a free copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—and review them for errors or discrepancies.

Pay Bills on Time: Your payment history is one of the most significant factors affecting your credit score. Make sure to pay all your bills, including credit cards, loans, and utilities, on time.

Reduce Credit Card Balances: Aim to keep your credit card balances low relative to your credit limits. High credit utilization can negatively impact your credit score.

Avoid Opening New Credit Accounts: While having a mix of credit accounts can be beneficial, opening multiple new accounts within a short period can lower your credit score.

Conclusion

In Kentucky, credit score requirements for mortgage loans can vary depending on the type of loan and lender you choose. While higher credit scores generally improve your chances of loan approval and favorable terms, there are loan programs available for borrowers with less-than-perfect credit.

Before applying for a mortgage loan, it’s essential to review your credit report, understand your credit score, and take steps to improve it if necessary. By demonstrating responsible financial behavior and maintaining a good credit history, you can increase your likelihood of securing a mortgage loan and achieving your homeownership goals in Kentucky.

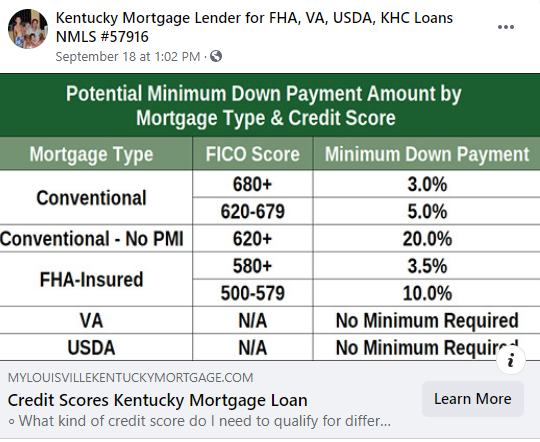

The type of mortgage you’re applying for determines the minimum requirements you’ll have to meet for your down payment, credit score, and debt-to-income ratio.

Find out what type of loan you might qualify for or what aspects of your finances you’ll need to improve to get a better shot at qualifying for a mortgage.

Loan Type

Min. Down Payment

Min. Credit Score

Max DTI

Property Type

Conventional

3%

620

45%

Primary, secondary, investment

VA

0%

none

none

Primary

FHA

3.5%

500

50%

Primary

USDA

0%

none

41%

Primary

Keep in mind: The minimum down payment, minimum credit score, and maximum DTI shown in the table apply to mortgages used to purchase a primary residence. While you can use a conventional loan or a jumbo loan to purchase a home for another purpose, you might need a larger down payment, a higher credit score, more cash reserves, or all three.

Credit score needed to buy a house

Mortgage lending is risky, and lenders want a way to quantify that risk. They use your three-digit credit score to gauge the risk of loaning you money since your credit score helps predict your likelihood of paying back a loan on time. Lenders also consider other data, such as your income, employment, debts and assets to decide whether to offer you a loan.

Different lenders and loan types have different borrower requirements, loan terms and minimum credit scores. Here are the requirements for some of the most common types of mortgages.

Conventional loan

Minimum credit score: 620

A conventional loan is a mortgage that isn’t backed by a federal agency. Most mortgage lenders offer conventional loans, and many lenders sell these loans to Fannie Mae or Freddie Mac — two government-sponsored enterprises. Conventional loans can have either fixed or adjustable rates, and terms ranging from 10 to 30 years.

You can get a conventional loan with a down payment as low as 3% of the home’s purchase price, so this type of loan makes sense if you don’t have enough for a traditional down payment. However, if your down payment is less than 20%, you’re required to pay for private mortgage insurance (PMI), which is an insurance policy designed to protect the lender if you stop making payments. You can ask your servicer to cancel PMI once the principal balance of your mortgage falls below 80% of the original value of your home.

FHA loan

Minimum credit score (10% down): 500

Minimum credit score (3.5% down): 580

FHA loans are backed by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). The FHA incentivizes lenders to make mortgage loans available to borrowers who might not otherwise qualify by guaranteeing the federal government will repay the mortgage if the borrower stops making payments. This makes an FHA loan a good option if you have a lower credit score.

FHA loans come in 15- or 30-year terms with fixed interest rates. Unlike conventional mortgages, which only require PMI for borrowers with less than 20% down, all FHA borrowers must pay an up-front mortgage insurance premium (MIP) and an annual MIP, as long as the loan is outstanding.

VA loan

Minimum credit score: N/A

VA loans are mortgages backed by the U.S. Department of Veterans Affairs (VA). The VA guarantees loans made by VA-approved lenders to qualifying veterans or service members of the U.S. armed forces, or their spouses. This type of loan is a great option for veterans and their spouses, especially if they don’t have the best credit and don’t have enough for a down payment.

VA loans are fixed-rate mortgages with 10-, 15-, 20- or 30-year terms.

Most VA loans don’t require a down payment or monthly mortgage insurance premiums. However, they do require a one-time VA funding fee, that ranges from 1.4% to 3.6% of the loan amount.

USDA loan

Minimum credit score: N/A

The U.S. Department of Agriculture guarantees loans for borrowers interested in buying homes in certain rural areas. USDA loans don’t require a minimum down payment, but you have to meet the USDA’s income eligibility limits, which vary by location.

All USDA mortgages have fixed interest rates and 30-year repayment terms.

USDA-approved lenders must pay an up-front guarantee fee of up to 3.5% of the purchase price to the USDA. That fee can be passed on to borrowers and financed into the home loan. If the home you want to buy is within an eligible rural area (defined by the USDA) and you meet the other requirements, this could be a great loan option for you.

What else do mortgage lenders consider?

Your credit score isn’t the only factor lenders consider when reviewing your loan application. Here are some of the other factors lenders use when deciding whether to give you a mortgage.

Debt-to-income ratio — Your debt-to-income (DTI) ratio is the amount of debt payments you make each month (including your mortgage payments) relative to your gross monthly income. For example, if your mortgage payments, car loan and credit card payments add up to $1,800 per month and you have a $6,000 monthly income, your debt-to-income ratio would be $1,800/$6,000, or 30%. Most conventional mortgages require a DTI ratio no greater than 36%. However, you may be approved with a DTI up to 45% if you meet other requirements.

Employment history — When you apply for a mortgage, lenders will ask for proof of employment — typically two years’ worth of W-2s and tax returns, as well as your two most recent pay stubs. Lenders prefer to work with people who have stable employment and consistent income.

Down payment — Putting money down to buy a home gives you immediate equity in the home and helps to ensure the lender recoups their loss if you stop making payments and they need to foreclose on the home. Most loans — other than VA and USDA loans — require a down payment of at least 3%, although a higher down payment could help you qualify for a lower interest rate or make up for other less-than-ideal aspects of your mortgage application.

The home’s value and condition — Lenders want to ensure the home collateralizing the loan is in good condition and worth what you’re paying for it. Typically, they’ll require an appraisal to determine the home’s value and may also require a home inspection to ensure there aren’t any unknown issues with the property.

FICO is used by 90% of lenders, according to myFICO, and has been around

since 1989. (VantageScore only hit the scene in 2006.)

If you’re not sure which scoring model a lender will use, just ask!

FICO Scores used for mortgages

USDA loan:

Most lenders prefer at least a 620

The U.S. Department of Agriculture insures for low- to moderate-income homebuyers. The USDA does not set a minimum credit score requirement and does not require a down payment.

Conventional loan:

620 is the minimum but in reality most will need a 720 or higher for a pre-approval if you are putting down less than 20%

Conventional loans aren’t insured by a government agency either, but they are covered by mortgage loan companies Fannie Mae and Freddie Mac. The down payment amount varies.

VA loan:

Most lenders prefer at least a 580

A Veterans Affairs loan is backed by the U.S. Department of Veterans Affairs and meant for military members and their spouses. These loans don’t require a minimum score or money down.

FHA loan:

500 (with 10% down payment) or 580 (with 3.5% down payment)

FHA loans, those guaranteed by the Federal Housing Administration, are for higher-risk borrowers who have poor credit and little money saved for a down payment. The credit requirements can fluctuate based on how much of a down payment you can afford.Most lenders have overlays now wanting a minimum 620 credit score even for FHA loans.

Are you interested in seeing how your current credit score might affect a new mortgage?

Let’s take a look together.

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

What Will My Lender Use? FICO is used by 90% of lenders, according to myFICO, and has been around since 1989. (VantageScore only hit the scene in 2006.) If you’re not sure which scoring model a lender will use, just ask! USDA loan: Most lenders prefer at least a 620 The U.S. Department of Agriculture … Continue reading Credit Score Information For Kentucky Home buyers

Email –

Email – Call/Text –

Call/Text –  Website:

Website:  Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome