Kentucky FHA Loan Guide — Updated for 2026

2026 Kentucky FHA Loan Limits & Complete Requirements Guide

Kentucky FHA loans remain one of the most accessible paths to homeownership for first-time buyers in Louisville, Lexington, Bowling Green, and all 120 counties statewide. Backed by the Federal Housing Administration (HUD), FHA loans offer low down payments, flexible credit requirements, and competitive interest rates — making them ideal for buyers who may not qualify for a conventional mortgage.

Effective January 1, 2026, FHA loan limits increased by 3.26% across all Kentucky counties. The new single-family limit is $541,288 — up $17,063 from 2025. This guide covers everything you need to know: updated loan limits, credit requirements, down payment assistance, mortgage insurance, and answers to the most common questions Kentucky homebuyers ask.

|

2026 Loan Limit

$541,288

Single-Family · All 120 KY Counties

|

Min Down Payment

3.5%

With 580+ Credit Score

|

Minimum Credit Score

500

580+ for 3.5% Down

|

Max Debt-to-Income

57%

With Compensating Factors

|

2026 FHA Loan Limits — All 120 Kentucky Counties

Kentucky is a standard-cost state. All 120 counties use the same national floor limits as published in HUD Mortgagee Letter 2025-23. Verify your county limit with the official HUD loan limit lookup tool.

| Property Type | 2025 Limit | 2026 Limit | Increase |

|---|---|---|---|

| 1-Unit — Single-Family Home | $524,225 | $541,288 | +$17,063 |

| 2-Unit — Duplex | $671,200 | $693,050 | +$21,850 |

| 3-Unit — Triplex | $811,275 | $837,700 | +$26,425 |

| 4-Unit — Fourplex | $1,008,300 | $1,041,125 | +$32,825 |

* Limits apply to the base loan amount only. Loan approval depends on credit, income, and property eligibility. The 3.26% increase reflects continued home price appreciation per the FHFA House Price Index.

Advantages

Why Kentucky Buyers Choose FHA

|

Requirements

Basic Eligibility Requirements

|

FHA Mortgage Insurance (MIP) — What to Expect

|

Upfront MIP

1.75% of the loan amount — typically rolled into the loan balance at closing

|

Annual MIP (paid monthly)

0.55% per year for 30-year loans with less than 10% down

|

|

MIP Duration — Less Than 10% Down

MIP remains for the life of the loan

|

MIP Duration — 10%+ Down

MIP cancels automatically after 11 years

|

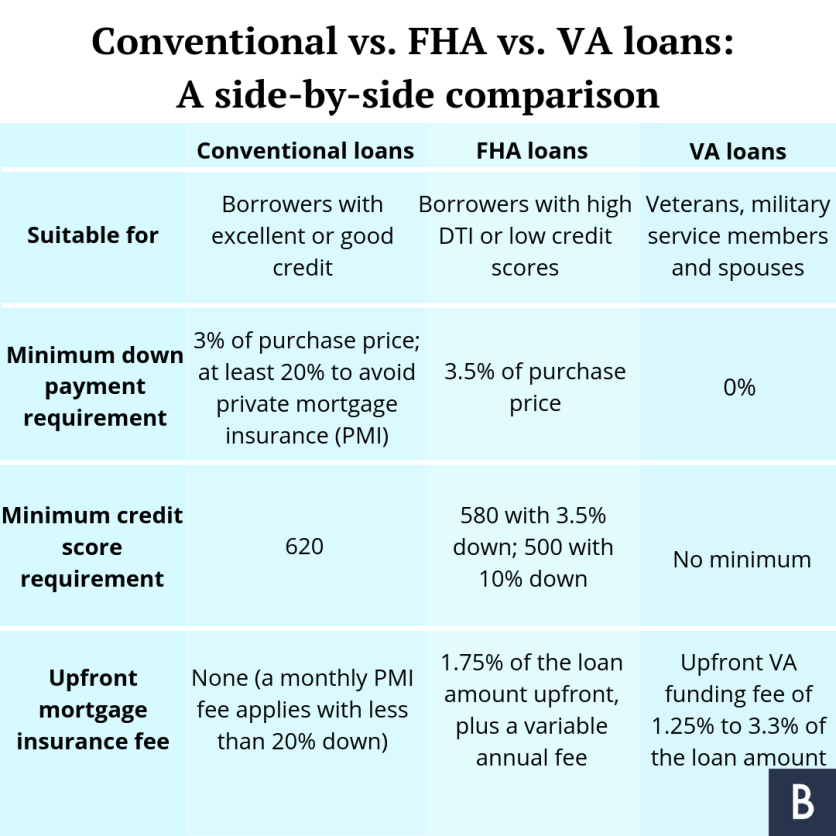

Other Kentucky Mortgage Programs to Compare

FHA is not the only option. Depending on your credit, income, and location, one of these programs may save you even more money:

|

Up to $10,000–$12,500 available. Stacks on top of FHA to eliminate your down payment. Income and purchase price limits apply. Available through Kentucky Housing Corporation.

|

Zero down payment for eligible rural and suburban Kentucky areas. No monthly MIP like FHA — just a small guarantee fee. Income limits apply. Great alternative for buyers outside Louisville and Lexington.

|

|

Zero down payment, no MIP for eligible veterans and active duty military. The best mortgage program available if you qualify. No loan limits for veterans with full entitlement.

|

Better option for buyers with 620+ credit and 3-5% down. PMI cancels at 20% equity (unlike FHA MIP). 2026 conforming limit: $806,500 for most Kentucky counties.

|

Not sure which program is right for you? I’ll compare all your options at no cost. See the full Kentucky mortgage program comparison guide on my blog.

Frequently Asked Questions — FHA Loans in Kentucky (2026)

What is the FHA loan limit in Kentucky for 2026?

The 2026 FHA loan limit for all 120 Kentucky counties is $541,288 for a single-family home — up from $524,225 in 2025, a 3.26% increase. Multi-unit limits are $693,050 (duplex), $837,700 (triplex), and $1,041,125 (fourplex). Kentucky is a standard-cost state, meaning all counties use the same national floor limit with no high-cost county adjustments. Source: HUD Mortgagee Letter 2025-23.

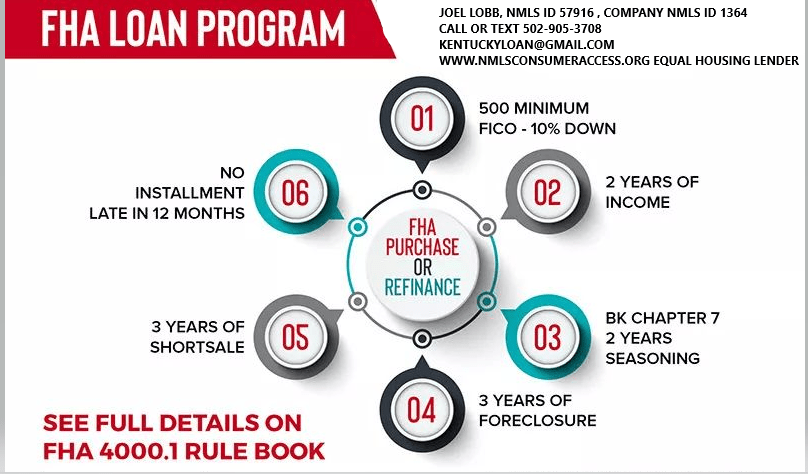

What credit score do I need for an FHA loan in Kentucky?

The FHA minimum is 500. With a score of 500–579, you’ll need a 10% down payment. With 580 or higher, you qualify for the 3.5% down payment option. Most lenders — including our programs — work with scores in the 580–620 range where conventional loans are typically unavailable. If your score needs work, I can help with a credit improvement plan at no cost before you apply. Call or text 502-905-3708.

Can I get an FHA loan after a bankruptcy or foreclosure in Kentucky?

Yes. FHA waiting periods are: Chapter 7 bankruptcy — 2 years from discharge date. Chapter 13 bankruptcy — 12 months of on-time trustee payments with court approval. Foreclosure — 3 years from the completed foreclosure date. You must have re-established good credit since the event. This flexibility is one of the biggest reasons Kentucky first-time homebuyers choose FHA over conventional loans.

Can I combine a 2026 FHA loan with KHC down payment assistance?

Absolutely — this is one of the most powerful combinations available to Kentucky homebuyers. Kentucky Housing Corporation (KHC) offers up to $10,000–$12,500 in down payment assistance that can be layered on top of an FHA loan, potentially covering your entire 3.5% down payment. The KHC purchase price limit for 2026 is $544,232. Income limits vary by county. Learn more about KHC programs or call me to check your eligibility.

What is the difference between FHA and a conventional loan in 2026?

FHA loans are government-backed and more forgiving on credit scores, down payments, and debt-to-income ratios. Conventional loans typically require 620+ credit and stronger finances, but private mortgage insurance (PMI) can be canceled once you reach 20% equity — unlike FHA MIP, which stays for the life of the loan if you put less than 10% down. The 2026 conventional conforming limit is $806,500 (higher than FHA’s $541,288 floor). FHA is better for buyers with credit challenges or limited savings. Conventional may be a better choice once you have 620+ credit. See my Kentucky mortgage program comparison for more detail.

How long does FHA loan approval take in Kentucky?

I offer free applications with same-day pre-approvals. Having your documents ready upfront (last 30 days of pay stubs, 2 years of W-2s and tax returns, 2–3 months of bank statements) speeds the process. Full loan closing from an accepted contract typically takes 30–45 days. Email me or call 502-905-3708 to start your free pre-approval today.

Can I buy a duplex or multi-unit property with a 2026 FHA loan?

Yes — FHA loans can finance 1 to 4 unit properties as long as you live in one unit as your primary residence. The 2026 limits are: Duplex $693,050 · Triplex $837,700 · Fourplex $1,041,125. Rental income from other units can often be used to help you qualify. This “house hacking” strategy is a popular way for Kentucky buyers to start building wealth while keeping monthly costs low. A standard 3.5% down payment applies.

Is there an income limit for FHA loans in Kentucky?

No — FHA loans have no maximum income limit. Anyone who meets the credit, down payment, and debt-to-income requirements can apply regardless of income. This differs from programs like USDA Rural Housing and some KHC programs, which do have household income caps.

Can my down payment be a gift from a family member?

Yes — FHA allows 100% of your down payment to come from a gift from a family member, employer, or approved nonprofit. The donor must provide a signed gift letter stating no repayment is expected. This is one of FHA’s biggest advantages over most conventional programs. When combined with KHC down payment assistance, many Kentucky buyers close with very little out of pocket.

What documents do I need to apply for a Kentucky FHA loan?

You’ll typically need: last 30 days of pay stubs, 2 years of W-2s and federal tax returns, 2–3 months of bank statements, a valid government-issued photo ID, and your Social Security number. Self-employed borrowers also need 2 years of business returns and a year-to-date profit & loss statement. I’ll walk you through exactly what’s needed during our free pre-approval call — no obligation. Call/text 502-905-3708 or email kentuckyloan@gmail.com.

Ready to Get Pre-Approved for a 2026 Kentucky FHA Loan?

Free application · Same-day pre-approval · No obligation · All 120 Kentucky counties · NMLS #57916

With over 20 years of experience and more than 1,300 Kentucky families helped, I specialize exclusively in Kentucky mortgage loans — FHA, VA, USDA, KHC, and Conventional. I know how to structure your loan to maximize your benefits and minimize your out-of-pocket costs at closing.

📞 Call/Text 502-905-3708 ✉ kentuckyloan@gmail.com

Joel Lobb · Mortgage Loan Officer · NMLS Personal ID #57916 · Company NMLS #1738461 · Equal Housing Lender ·

www.nmlsconsumeraccess.org

This website is not endorsed by or affiliated with the FHA, VA, USDA, or any government agency.

All loan programs are subject to credit approval, income verification, and property eligibility.

Loan limits and program availability subject to change without notice. Rates are not guaranteed and subject to change daily.

Information provided is for educational purposes only and does not constitute a commitment to lend.

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204

Email –

Email – Address:

Address:

First-Time Home Buyers Welcome

First-Time Home Buyers Welcome