There are many ways to get the mortgage to buy your first home. The FHA is one option. If you are a first-time homebuyer in Kentucky, an FHA loan could be the perfect option for you. There are many flexible requirements, low down payments, and financial assistance options available. These are just a few of the many things that can help make homeownership more accessible.

What is an FHA Loan?

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration (FHA). It’s designed for low-to-moderate-income borrowers, offering relaxed qualification standards compared to conventional loans. Here are the main advantages:

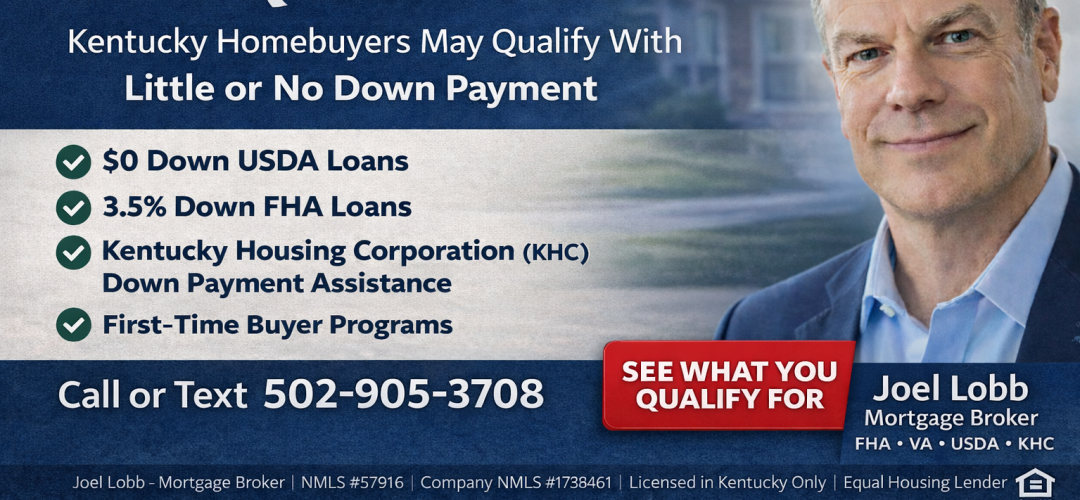

- Low down payment: As little as 3.5% of the purchase price.

- Lower credit score requirements: Minimum score of 500 with 10% down or 580 with 3.5% down.

- Seller-paid closing costs: Sellers can contribute up to 6% of the purchase price.

- Flexible qualifying criteria: Higher debt-to-income (DTI) ratios and options for non-occupant co-signers.

How to Qualify for a Kentucky FHA Loan

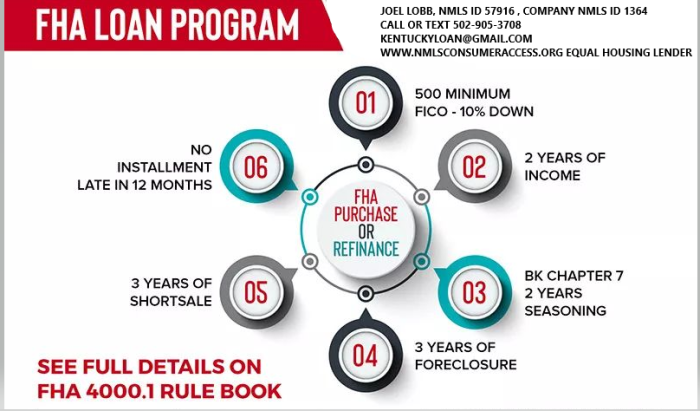

1. Credit Score Requirements

- 580 or higher: You’ll need a minimum credit score of 580 to qualify for the 3.5% down payment option.

- 500-579: You can still qualify with a 10% down payment, but many lenders prefer a score of 580 or higher.

- Bankruptcy or Foreclosure:

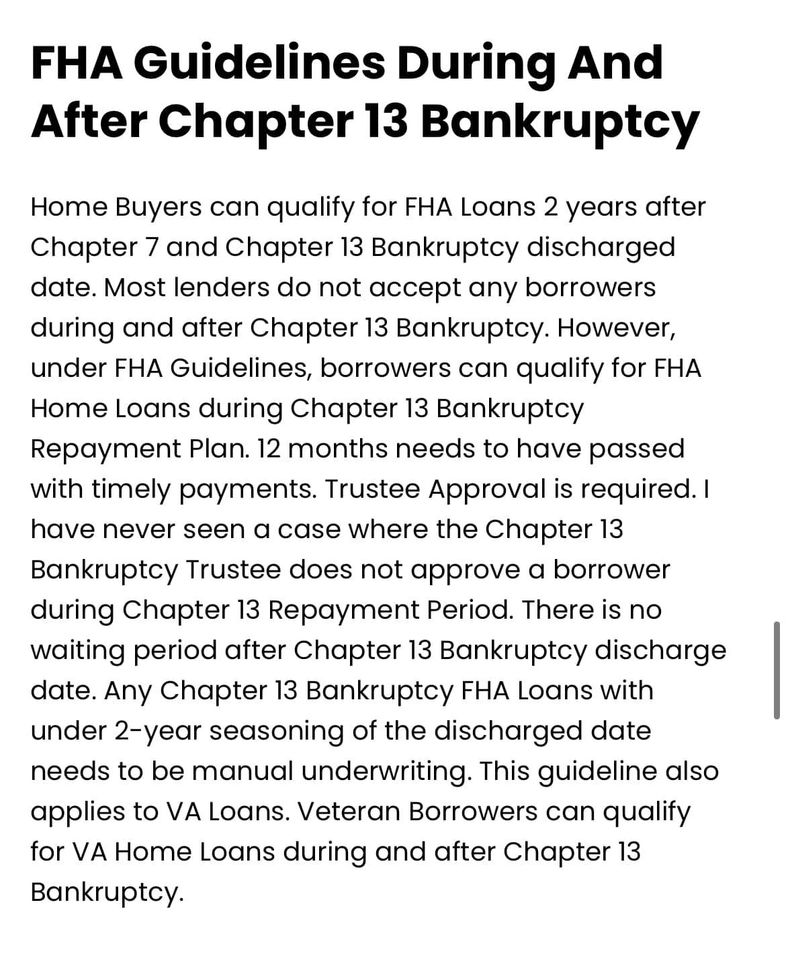

- Chapter 7 bankruptcy: Must be 2 years removed, with good credit since.

- Chapter 13 bankruptcy: Can qualify after 1 year of on-time payments with trustee approval.

- Foreclosure: Must be 3 years removed, unless there are extenuating circumstances.

2. Income and Debt-to-Income Ratio

- DTI ratio: Typically, up to 45%% of your income can go toward your mortgage payment, and up to 56.9% can go toward all debts, depending on your credit and financial history.

- Work history: You must have a stable employment history of at least 2 years in the same field. Recent graduates can use college transcripts as a substitute.

3. Down Payment and Gift Options

- 3.5% down payment: This can be gifted by a family member, employer, or nonprofit organization, drawn off a retirement account like a 401k or money saved up.

- Cash deposits: Cash cannot be used as proof of funds for your down payment—only traceable sources are allowed.

4. Property Requirements

- Must be your primary residence. FHA loans are not for investment properties or second homes.

- Eligible property types: Single-family homes, townhomes, condos (must be approved condo development on HUD approved list), duplexes, and some manufactured homes (if affixed to a permanent foundation).

- Appraisal: The property must be appraised by an FHA-approved appraiser to meet HUD standards.

5. Mortgage Insurance Premium (MIP)

- Upfront MIP: 1.75% of the loan amount, which can be rolled into the loan.

- Annual MIP: 0.45%-1.05% of the loan amount, depending on the down payment and loan term.

Kentucky FHA Loan Limits for 2025

In all Kentucky counties, the FHA loan limit is $524,225 for a single-family home up to $1,008,300 for a four-unit property

Why Choose an FHA Loan as a Kentucky First-Time Buyer?

Pros

- Lower credit thresholds: You can qualify with a credit score as low as 500.

- Smaller down payments: With as little as 3.5% down with a 580 credit score

- Seller-paid costs: The seller can pay a significant portion of your closing costs.

- Higher debt to income ratios

- Lenient on past bankruptcies and foreclosures.

Cons

- Mortgage insurance: You’ll pay MIP for the life of the loan if your down payment is less than 10%.

- Property requirements: Homes must meet specific standards, which may limit your options.

- a lot of sellers will not accept an FHA mortgage as a offer due to property may need work to meet FHA HUD minimum standards

- Purchase price limits and only can be used for primary residence

FHA Loans vs. Conventional Loans

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Credit Score | 500+ | 620+ |

| Down Payment | 3.5% (580+ credit score) | 3%-20% |

| Mortgage Insurance | Required for life of loan | Can be removed at 20% equity |

| Debt-to-Income Ratio | Up to 55% | Up to 45% |

| Property Standards | Strict requirements | More flexibility |

Other Kentucky First-Time Homebuyer Programs

1. Kentucky Housing Corporation (KHC)

- Down payment assistance up to $10,000.

- Tax credit programs for first-time buyers.

2. USDA Loans

- Zero-down-payment option for eligible rural areas.

- Minimum credit score of 620-640 preferred.

3. VA Loans

- No down payment or private mortgage insurance required for eligible veterans. No minimum credit score, higher debt to income ratios allowed and no monthly mortgage insurance and low 30 year fixed rates

Need Help Getting Approved for an FHA Loan in Kentucky?

As an experienced mortgage loan officer specializing in FHA loans for Kentucky first-time homebuyers, I’m here to guide you every step of the way.

Contact Me Today:

- 📧 Email: kentuckyloan@gmail.com

- 📞 Call/Text: 502-905-3708

- 🌐 Website: www.mylouisvillekentuckymortgage.com

Joel Lobb

Mortgage Loan Officer – Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com

Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

Equal Housing Lender

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.